Treasury Secretary Janet Yellen warned Monday that the U.S. could be unable to "continue to satisfy all of the government’s obligations" by June 1 if Congress does not raise or suspend the debt limit before that time.

Why it matters: The warning reduces the timeline in which the Biden administration and House Republicans must come to an agreement to stave off a catastrophic default.

Adidas is facing a lawsuit from investors who allege the sportswear giant "routinely ignored extreme behavior" of Ye years before it dropped its partnership with the artist formerly known as Kanye West.

Driving the news: Adidas told USA Today Sunday it would fight the lawsuit, which alleges a 2018 report "ignored serious issues" of partnering with Ye by "generally alluding" to risks "rather than stating that the company had actually considered ending the partnership as a result of West's personal behavior."

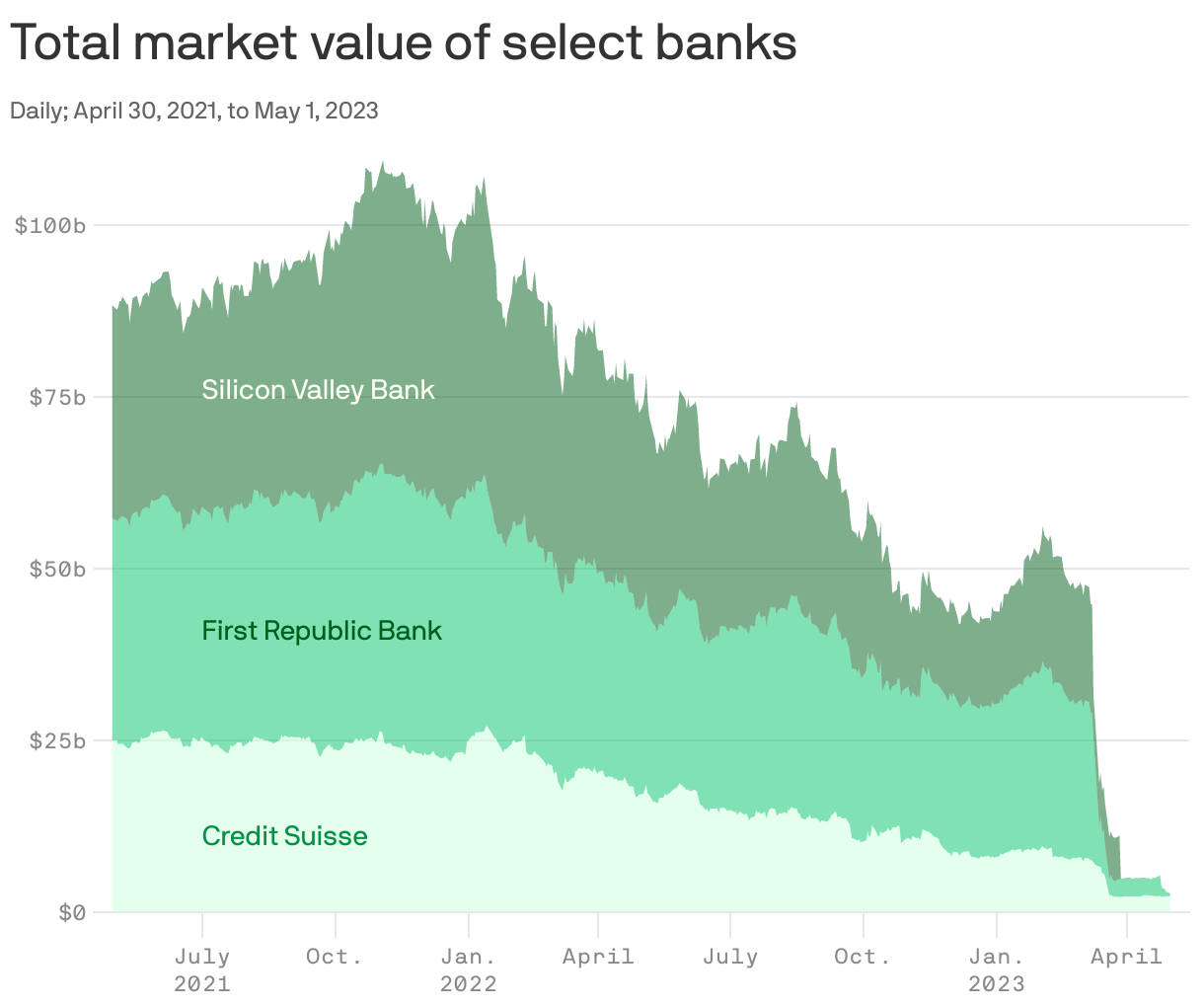

JPMorgan Chase has now played savior in two of the three largest bank failures in U.S. history — Washington Mutual and First Republic Bank.

Why it matters: The two institutions were in vastly different conditions before needing to be rescued 15 years apart, but both offered attractive businesses for JPMorgan to consider.

Celsius is facing new allegations brought by a group of its disgruntled customers who want all of their money back and then some.

Driving the news: A group of unsecured creditors filed a class claim against the bankrupt platform, seeking no less than the full amount they are owed in trapped funds, some $5.2 billion, as well as "damages" in an amount to be determined later at trial, a court filing submitted over the weekend shows.

Top executives at U.S. financial institutions flagged a broader concern around the nation's commercial real estate market, amid tumult in the banking sector.

Why it matters: The insights Monday morning come at a delicate time for the U.S. economy, which is digesting the government takeover of First Republic Bank, the FDIC's third bank intervention since March.

What they're saying: "There's already a lot of pressure in that area," said PGIM CEO David Hunt, referring to the commercial real estate market.

Hunt was speaking at an opening panel during the Milken Institute's Global Conference, an annual gathering of business and global leaders held in Los Angeles.

The panel pointed specifically to the strain on commercial real estate backed securities (CMBS) and the turmoil that the Fed's rapid rate hikes have caused across that segment.

"We're seeing CMBS as much as an opportunity as it is a challenge," added fellow panelist Rishi Kapoor, co-CEO of Investcorp.

Catch up quick: Remote work that took hold during the pandemic hollowed out cities, and sank office occupancy rates.

Rising interest rates added an additional layer of stress on commercial real estate market, as major loans come due for developers.

Yes, but: Certain parts of commercial real estate are under pressure, but not all of it, said Citigroup CEO Jane Fraser.

The bottom end of the CMBS stack will be under stress, she notes.

"But let's not make the sweeping statements and let's not tarnish all the regional and small banks" that provided loans to the sector, Fraser added.

Fraser's bottom line: The First Republic takeover addressed a critical uncertainty looming over the market, and the Citi leader's confidence in the U.S. financial system is unwavering.

"It's not perfect, but it's the envy of the world," Fraser says, adding that a "small handful" of banks were poorly managed and seizing headlines.

In the wake of three major bank failures, the FDIC released a report Monday afternoon with recommendations for reforming the way the nation's deposit insurance system works.

Why it matters: All the banks that folded or failed this year had a large share of deposits that weren't covered by FDIC insurance, which maxes out at $250,000.

There's hope this morning that the banking crisis might be over — at least for the time being. But the cause of the crisis hasn't gone away, and the entire banking system is going to feel shaky for the foreseeable future.

Why it matters: Banks create money and drive the economy. If they're struggling — even if they're not failing — that's bad news for economic growth and vitality.

The feud between Florida Gov. Ron DeSantis (R) and the Walt Disney Company has been going on for years, with at least two dueling lawsuits playing out in state court.

Driving the news: DeSantis and Disney are at odds over several issues, including a law dubbed "Dont Say Gay" by its critics and the control over the Reedy Creek District near the Disney World resort in Orlando.

Electric vehicle startup Lordstown Motors warned Monday that its survival is in jeopardy after its manufacturing partner, Foxconn, threatened to withdraw from their deal in northeast Ohio.

Driving the news: Lordstown, which makes an EV pickup called Endurance in small quantities, said in an SEC filing that "there is substantial doubt" about the company's future as a business.

NBA chief marketing officer Tammy Henault, Netflix chief content officer Bela Bajaria, AMD CEO Lisa Su and Twitch chief content officer Laura Lee are among top business leaders named to this year's A100 List.

Why it matters: The annual list, organized by Gold House, and selected by a group of about 50 journalists and nonprofits from the Asian American Pacific Islander community, calls out prominent figures of Asian heritage who have impacted the way Americans live and experience the world.

Banking regulators were well aware of the problems at both Silicon Valley Bank and Signature Bank ahead of their failures in March, but weren't able to prevent catastrophe.

Driving the news: Three separate autopsies on the bank failures were released last Friday by regulators, and they all highlighted the inadequacy of bank supervisors.

First Republic Bank was seized by regulators and sold to JPMorgan Chase, the Federal Deposit Insurance Corporation announced early Monday morning, making First Republic the third major bank failure in eight weeks.

Why it matters: First Republic is the latest victim of a U.S. banking system that's adjusting to a new normal of client deposits fleeing in search of greater safety and higher rates.

A TikTok trend dubbed "bare minimum Mondays" might help cure the "Sunday scaries" but taking it too far could derail your career, experts tell Axios.

The big picture: Like "quiet quitting" — a viral term defined as workers who don't do more than is necessary — bare minimum Mondays encourage easing into work by doing just enough to get by and practicing self-care at the start of the work week.

/2023/04/28/1682706558751.gif?w=3840)