The lingering banking problem

Add Axios as your preferred source to

see more of our stories on Google.

There's hope this morning that the banking crisis might be over — at least for the time being. But the cause of the crisis hasn't gone away, and the entire banking system is going to feel shaky for the foreseeable future.

Why it matters: Banks create money and drive the economy. If they're struggling — even if they're not failing — that's bad news for economic growth and vitality.

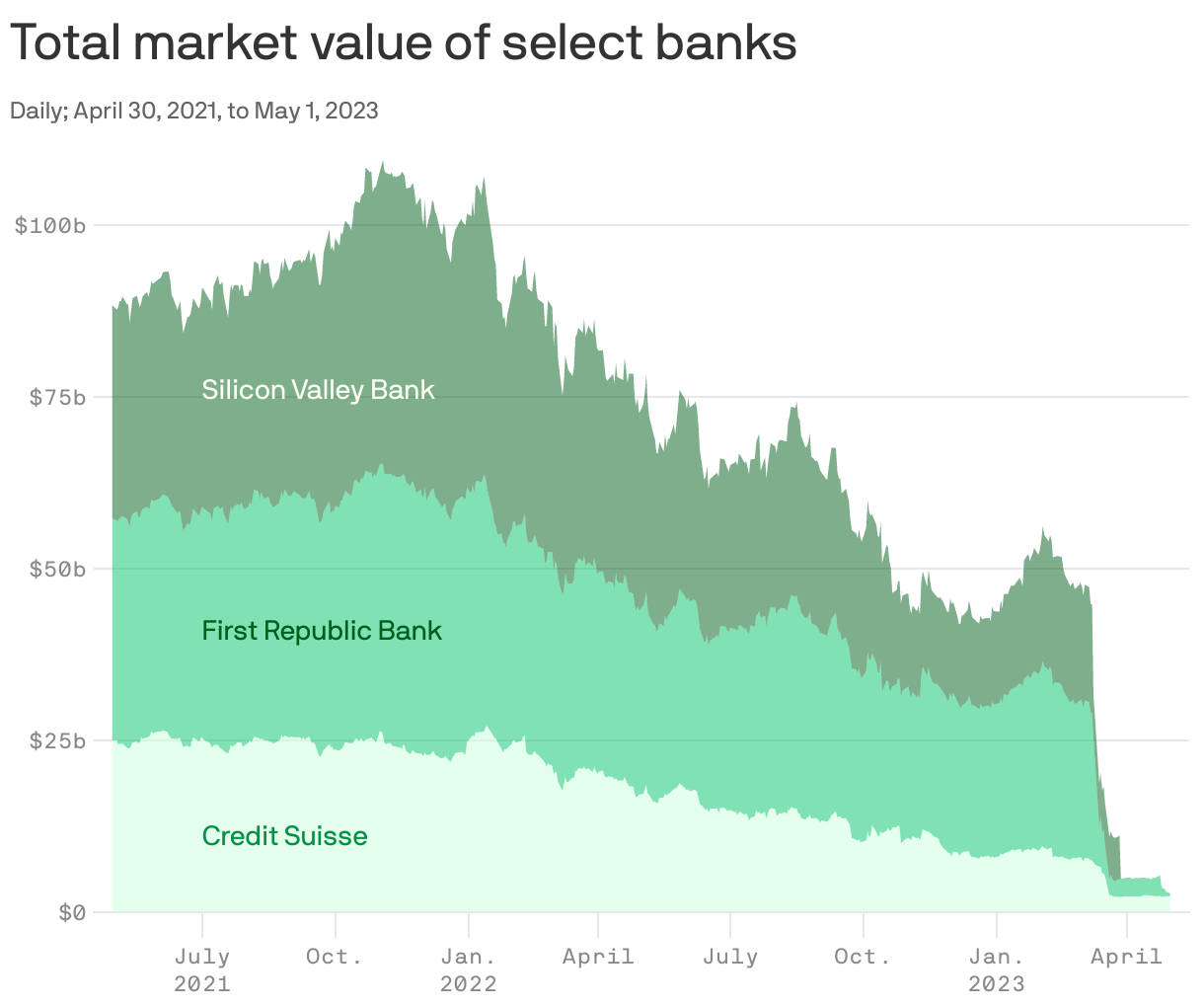

Driving the news: The count of multibillion-dollar banking corpses continues to grow. First Republic Bank has now joined Credit Suisse, Silicon Valley Bank, Signature Bank and Silvergate on the list of dead institutions.

By the numbers: At the beginning of last year, those four banks had an equity value of more than $100 billion. Today, their shareholders have been largely wiped out.

The cause of death was the same in all cases: rapidly rising interest rates. And if those rates proved fatal for such large and formerly valuable institutions, they will have caused serious damage to many other banks that remain alive.

What they're saying: "This part of the crisis is over," said JPMorgan Chase CEO Jamie Dimon on an analyst call this morning, after taking over First Republic. "This is how the system is meant to work. You're never going to have no bank failures."

Between the lines: So far, all of the failed banks were reliant on very large deposits from companies and wealthy individuals.

- That's not true of the banking system as a whole — but deposits are leaving the system, they're not coming back any time soon, and they're the cheapest funding that banks have.

- Without them, banks will make less money and have less lending capacity.

💭 Our thought bubble: When the banking crisis seemed like it was contained to SVB and Silvergate, there was a school of thought that tighter lending conditions would help the Fed cool down the economy.

- The failure of First Republic, however, raises the specter of a more systemic weakness in the financial system. There's no silver lining here.

The bottom line: In an ideal world, Fed rate hikes can reduce demand for loans without rendering banks insolvent. We're far from that ideal world.