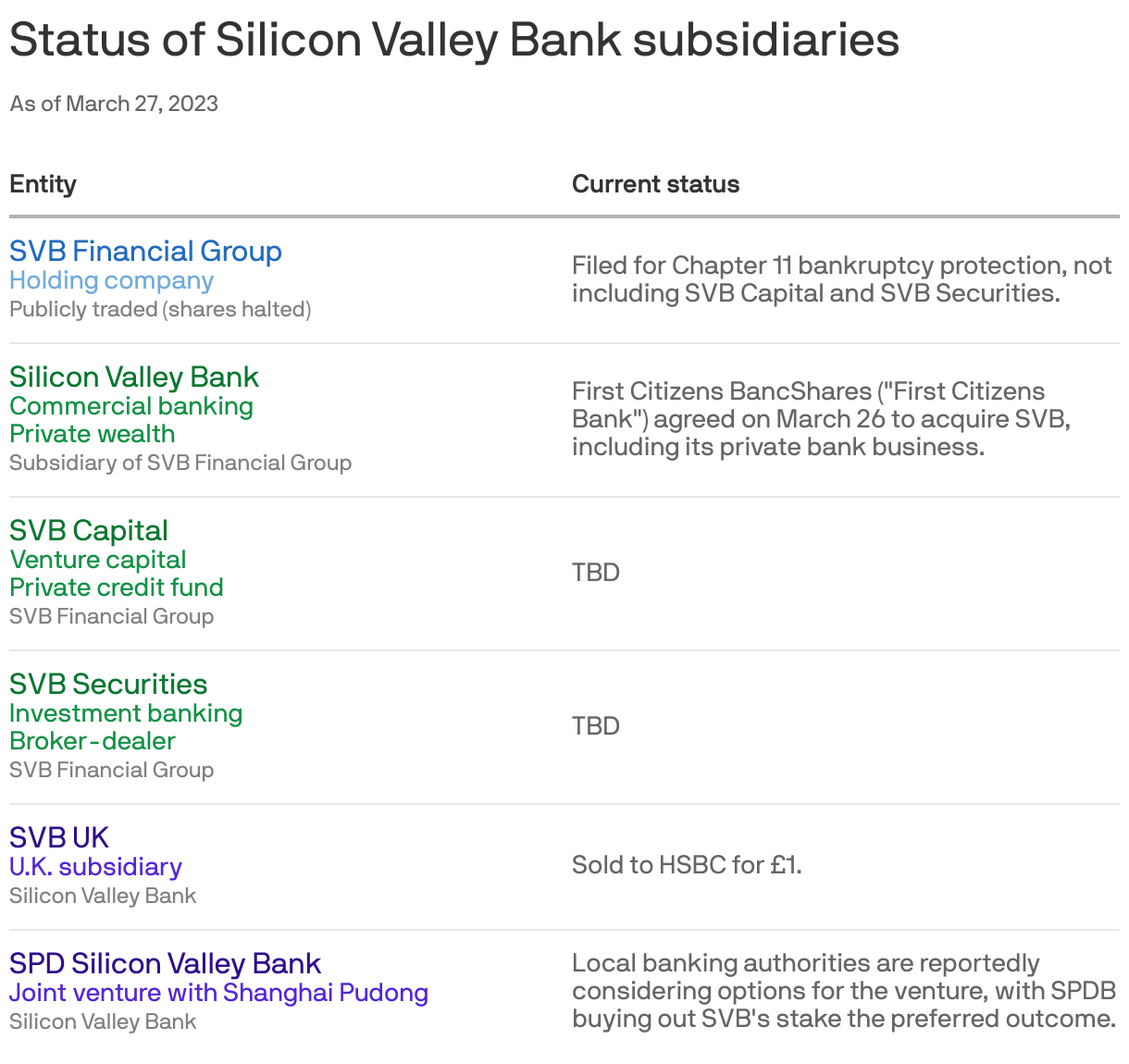

UBS has struck a deal to purchase troubled Credit Suisse for $3.2 billion, as bank solvency fears continue to batter global markets.

Why it matters: Aggressive central bank action to arrest stubborn inflation has shaken investor confidence, with financial institutions caught in the crosshairs.

The banking sector is poised to head into a third week of existential questions and whipsaw volatility, despite official efforts to stabilize markets and reassure depositors.

Meanwhile, the search for causes, lessons, and blame is already well underway.

The world's leading central banks jointly announced new action to try to keep U.S. dollars flowing easily through the global banking system, returning to a strategy used extensively in past crises.

Driving the news: The Federal Reserve, along with the European Central Bank, Bank of England, Bank of Canada, Bank of Japan, and Swiss National Bank, with their Sunday evening (U.S. time) aimed to make dollar swap lines more readily available.

Sen. Elizabeth Warren (D-Mass.) called for an independent investigation into the Federal Reserve and the banking regulatory system during an appearance on ABC's "This Week" on Sunday.

Why it matters: The banking sector is poised to head into a third week of existential questions and whipsaw volatility, despite official efforts to stabilize markets and reassure depositors, Axios' Pete Gannon writes.

A coalition of midsize U.S. banks is calling on the government to insure all deposits for the next two years, in the wake of Silicon Valley Bank's emergency rescue that insured all of the firm's deposits regardless of size.

Driving the news: The Mid-Size Bank Coalition of America sent a letter to regulators arguing that a temporary suspension of the FDIC's deposit insurance limit is necessary to ensure that smaller banks can navigate the current banking crisis, Bloomberg reported.

The past 10 days have felt like an eternity, so here's a handy timeline of what's happened:

March 8: SVB announced it has raised $500 million from General Atlantic and plans for a $1.25 billion common stock sale, plus another $500 million of depository shares.

Earlier in the day, Silvergate, a bank popular with the crypto industry, announced it's shutting down operations, a harbinger to what's to come.

SVB CEO Greg Becker attempted to appease VCs and startups in a conference video call, asking them to "stay calm." The bank also updated Goldman Sachs on deposit outflows, effectively killing the share offering.

By the end of the day, customers had initiated $42 billion in withdrawals, making it the largest bank run in history.

In the evening, the FDIC informed an unknown number of SVB employees that they’d keep their jobs as part of the newly formed bridge bank for the next 45 days.

March 12: Bids to acquire SVB were due on Sunday, but there was no sale (the FDIC reportedly declined the lone bid by an unnamed company).

March 12: The U.S. government announced it would backstop all SVB deposits.

March 15: Credit Suisse, who’s had its own woes for quite some time, announced it will borrow up to 50 billion Swiss francs ($53.68 billion) from the Swiss National Bank to strengthen its liquidity.

March 16: Treasury Secretary Janet Yellen reassured Congress that the U.S. banking system is “sound.”

11 banks inject $30 billion of deposits into First Republic Bank as a show of confidence as it’s spent the week trying to avoid SVB’s fate.

March 17: SVB Financial Group files for Ch. 11 bankruptcy protection in the Southern District of New York.

Bids in a second attempt to sell SVB are reportedly due.

Startups breathed a sigh of relief Sunday night when the Federal Reserve announced it would backstop Silicon Valley Bank deposits. Yet amid anxiety about the banking sector and the future of venture capital funding, this past week has been surprisingly busy.

The big picture: Among startup-land denizens and venture capitalists who were SVB clients, there hasn't been a uniform approach about what to do since the government takeover.

Why it matters: SVB’s temporary successor, Silicon Valley Bridge Bank — helmed by CEO Tim Mayopoulos — has been on the charm offensive this week, sending emails to customers and holding video calls to answer questions.

"[P]lease keep a portion of your deposits and operating business at SVB as part of your diversification strategy. Bringing any portion of your deposits back to Silicon Valley Bridge Bank is a vote for us to succeed," the bank said in an email to customers seen by Axios.

State of play: Startups and VCs have opted for a couple of approaches:

Move away from SVB: Others have fully pulled out their funds from SVB and moved to a bigger bank — “the scar tissue is very very deep,” says Logikcull CEO Andy Wilson.

A mix of banks: A growing group of companies are doing it all, keeping some funds in SVB (typically $250,000 or less) and putting the rest in one or more other banks.

Some are surely opting to stick with SVB, though it's unclear how popular this this approach is.

Between the lines: While not a universal sentiment, a non-trivial portion of the startup world says SVB should survive and remain a sustainable business. This would be a good outcome for the U.S. banking system, and because SVB itself is a unique startup friendly institution.

A group of VCs put out a support statement, advising startups to keep at least 50% of their cash at the embattled bank (as of late Friday, it still hasn't found a buyer).

The intrigue: “I miss SVB” has become a growing refrain from folks who’ve opened new accounts at other banks and noticed the differences in the customer experience.

Also, the minimum balances at other banks are posing a challenge for smaller companies looking for SVB alternatives.

Meanwhile: A slew of fintech companies providing various services, to startups and other businesses, have stepped in to offer alternatives to SVB, and banks in general. For example:

Brex, best known for its corporate credit cards for startups, announced over the weekend emergency credit lines for companies. It also offers various other cash management options like the ability to split funds across several banks, in FDIC-insured $250,000 chunks.

Arc, which also offers a similar slew of services and rolled out same-day payroll financing and venture debt this week, said on Wednesday that since the prior Thursday, it’s seen “15x growth in deposit volumes and 500+ applications for hundreds of millions in both short-and-long-term financing.”

Ramp, yet another fintech startup focused on business cash management, set up a referral program to direct customers to alternative banks, facilitating over $1 billion in deposits within the first 48 hours after SVB shut down.

Yes, but: These fintech companies have some limitations — namely, that they aren’t banks.

“[Banks are] always better at doing loans because they have the lowest cost of capital,” Brex CEO Henrique Dubugras tells Axios, adding that his company returned its SVB funds to the bank and even added a little more.

The bottom line: The past week has been an education in cash management for Silicon Valley.

Good bankers know the industry they serve. They know its idiosyncrasies, its cast of characters, its business cycles. They help their clients through good years and bad — and are rewarded with deep loyalty and fat deposit accounts.

Why it matters: The industry that bankers know differs from bank to bank — but it's never banking. A wine-industry relationship banker at Silicon Valley Bank has to know much more about malolactic fermentation than about Tier 1 capital adequacy ratios.

The spikein the number of individuals directly holding Treasury bills makes it more likely that the government will find its way to raising the debt ceiling.

Why it matters: The biggest reason the debt ceiling is such a big political problem is that most Americans don't care about it, and most of those who do think that its existence is a good thing and that it shouldn't be raised.

Here's a riddle for you. Shares in First Republic Bank closed at $31.21 on Monday, and opened at $49.69 on Tuesday — an overnight spike of 59%. There was no news about the bank over the course of the intervening hours. So why did the stock move so much?

The answer: The stock moved so much because there was no news about the bank over the course of the intervening hours. But also, once banks start to get into trouble, the share price naturally becomes incredibly volatile, just because their balance sheet leverage is so enormous at that point.

With T-bills yielding 5%, it's hardly any wonder there's been a huge surge of enthusiasm for them, even when the main website for purchasing them feels like it's stuck in 1998.

State of play: The above chart shows the number of people buying T-bills on TreasuryDirect through February, before the banking crisis.

America needs technical workers — and supply isn't measuring up to demand.

The big picture: Older workers in the skilled trades are retiring and not enough young people are training up to take their jobs as construction workers, plumbers, electricians and beyond.

/2023/03/17/1679039555008.gif?w=3840)

/2023/03/18/1679104583109.gif?w=3840)