Driving the news: Sen. Marco Rubio (R-Fla.) has reintroduced the Sunshine Protection Act, which was surprisingly approved by a unanimous vote in the Senate last year but wasn't voted on by the House.

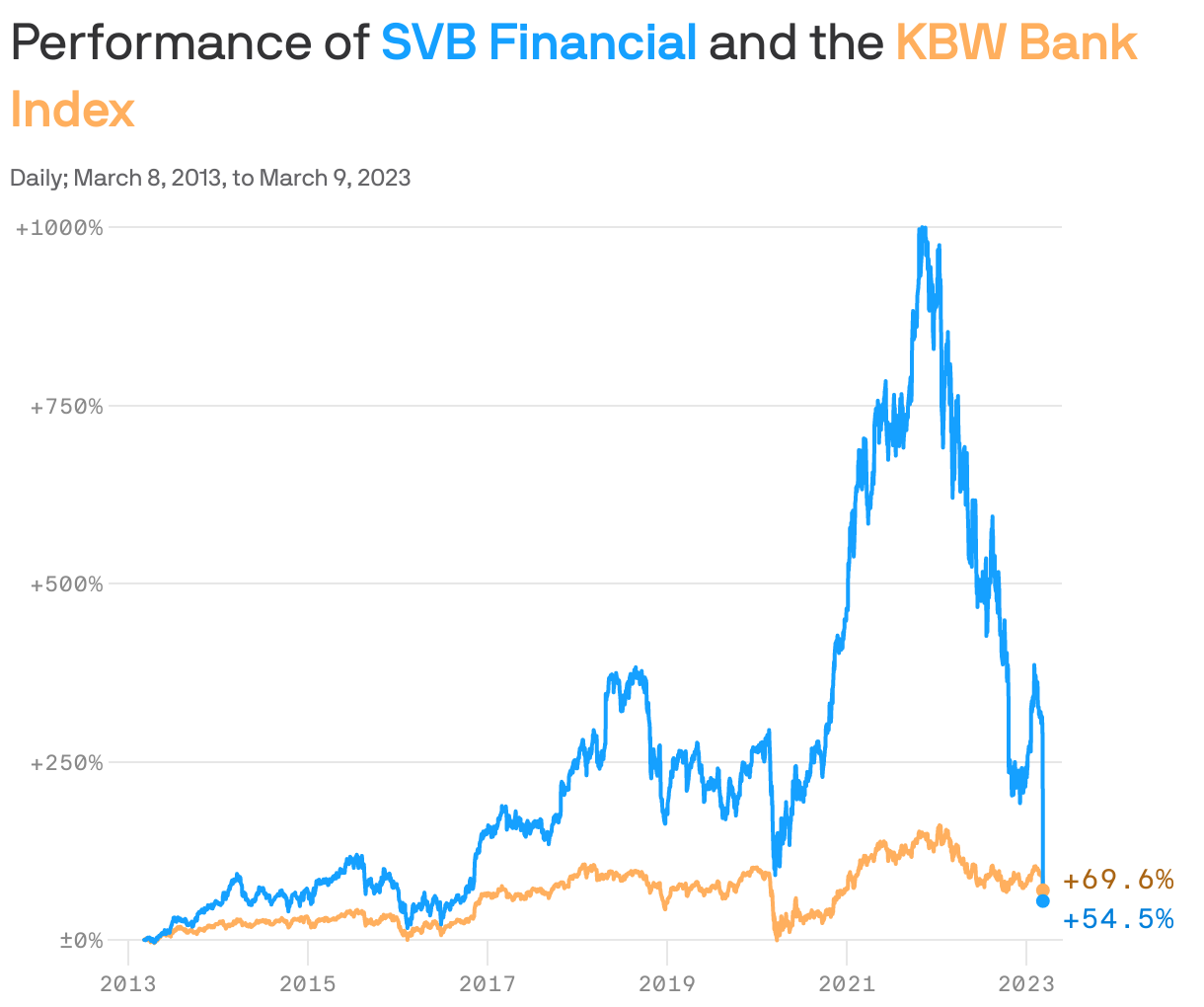

Why it matters: SVB served a range of roles across the industry; it not only took startups' cash but also offered them venture debt and other loans while providing banking and lending money to venture capital firms. Its collapse is the largest bank failure since Washington Mutual in 2008.

Circle's usd coin (USDC), the second-largest stablecoin in the world, fell below its $1 peg, as markets grappled with the fallout from Silicon Valley Bank's failure.

Why it matters: Uncertainty in the U.S. banking system is creating fears for users of the $40 billion stablecoin, because a portion of its cash reserves were held at SVB, which the U.S. government took control of on Friday.

USDC's struggles suggest more financial turmoil is in store, as markets fully digest the collapse of SVB. The stablecoin first surrendered the 1:1 watermark late Friday, according to CoinMarketCap, and struggled to retake it on Saturday.

Last year, the cryptocurrency market was convulsed by the rapid collapse of Terra, another stablecoin; while Tether's USDT (the world's largest) also briefly de-pegged in November.

Silicon Valley Bank on Friday paid out annual bonuses to eligible U.S. employees, just hours before the bank was seized by the U.S. government, Axios has learned from multiple sources.

What to know: The bonuses were for work done during 2022, and were previously scheduled to be disbursed on March 10. That date ultimately coincided with the bank's takeover by the Federal Deposit Insurance Corporation.

Adidas doesn’t know what to do with its collection of unsold Yeezys, the shoes designed by Ye, the artist formerly known as Kanye West. But the company's CEO suggested this week a lot of ideas are on the table.

The big picture: Yeezy shoes are still in high demand and are selling well above retail value on the resale market months after Adidas took the shoes off the shelf after ending its nine-year partnership with Ye over his antisemitic comments.

Last week, Silicon Valley Bank CEO and president Greg Becker was interviewed on stage at the annual Upfront Summit in Los Angeles, by The Information reporter Kate Clark. Here's what he said when asked about the simmering concerns (lightly edited for clarity):

There are some concerns about the liquidity health of the bank … because you parked a bunch of money when interest rates were low in a bad bond portfolio. … Are those valid concerns?

I’ll start with the story I tell our employees. This has been the case for the last 30 years. When you have a cycle and its going really well we get praised to the extreme. Conversely, when the market is down, people pile on because it's like, "Oh my God, the credit is gonna be bad, and liquidity and deposits and all that stuff."

So, to me, what are the important things? The important things are: We have a very low loan-to-deposit ratio, which is important when you think about it.

Credit quality is incredibly strong and actually prepared even if it gets a lot worse, and we expect it to get worse.

And the third thing is liquidity. When you go through liquidity—and banks have different ways to calculate it—but it's like, you can look at your cash, your borrowing availability and what your securities are that you could sell.

So the question that came up in that article you referenced is basically, if you were to sell all your securities, would there be a large loss? And the answer is true. But what we’ve been publicly saying, and we said that last quarter, is that we have is zero intention to sell those securities.

So, it's like a loan portfolio that you lent money when the rates were low, and now if you mark those to market, it would actually be lower than the valuation, so it’s the same thing.

You know, most importantly, we have a stable structure, strong capital ratios to support our clients pretty much no matter what happens

I think the criticism is that you should have seen those interest rates rising. … Do you think you made a mistake in not predicting that we were going to enter this downturn?

If anyone can say that they forecast a 5.5% interest rate from last year, when they were zero, please let me know what your next forecast is.

I really thing that's the fundamental — we expected the following: We expected the rates to increase, but when you do scenario planning, you think about up rates 100 basis points, up 200 basis points.

Then you create your balance sheet in a way that is structured for pretty much no matter what happens, you can manage through that.

So, when I think about it, it’s more of a headwind to what level of profitability we have than any other issue, and that’s really what this storyline is about.

Given how deeply and widely its roots run across the industry, Silicon Valley Bank — dramatically seized on Friday by the federal government amid a crippling bank run and a swooning stock — couldn't have a more apt name.

Why it matters: The stunning events of the last two days couldn't have unfolded as dramatically as it has without such a deep entrenchment. The venture capital industry is well known for its tight-knit network, and propensity to circulate information (and opinions) at the speed of tweets.

Silicon Valley Bank's customers withdrew $42 billion from their accounts on Thursday. That's $4.2 billion an hour, or more than $1 million per secondfor ten hours straight.

Why it matters: To put that in context, the previous largest bank run in modern U.S. history took place at Washington Mutual bank in 2008, and totaled $16.7 billion over the course of 10 days. That's a mere trickle in comparison to what was seen at SVB.

The implosion of Silvergate Bank is an existential event for what remains of the crypto ecosystem. Silvergate underpinned almost every American crypto company; without it, it's hard to see how the industry can possibly thrive.

If Silvergate didn't exist, it would have been impossible to invent it — regulators would not have allowed the creation of a de novo crypto bank in the past, and they certainly don't seem minded to do so in the future.

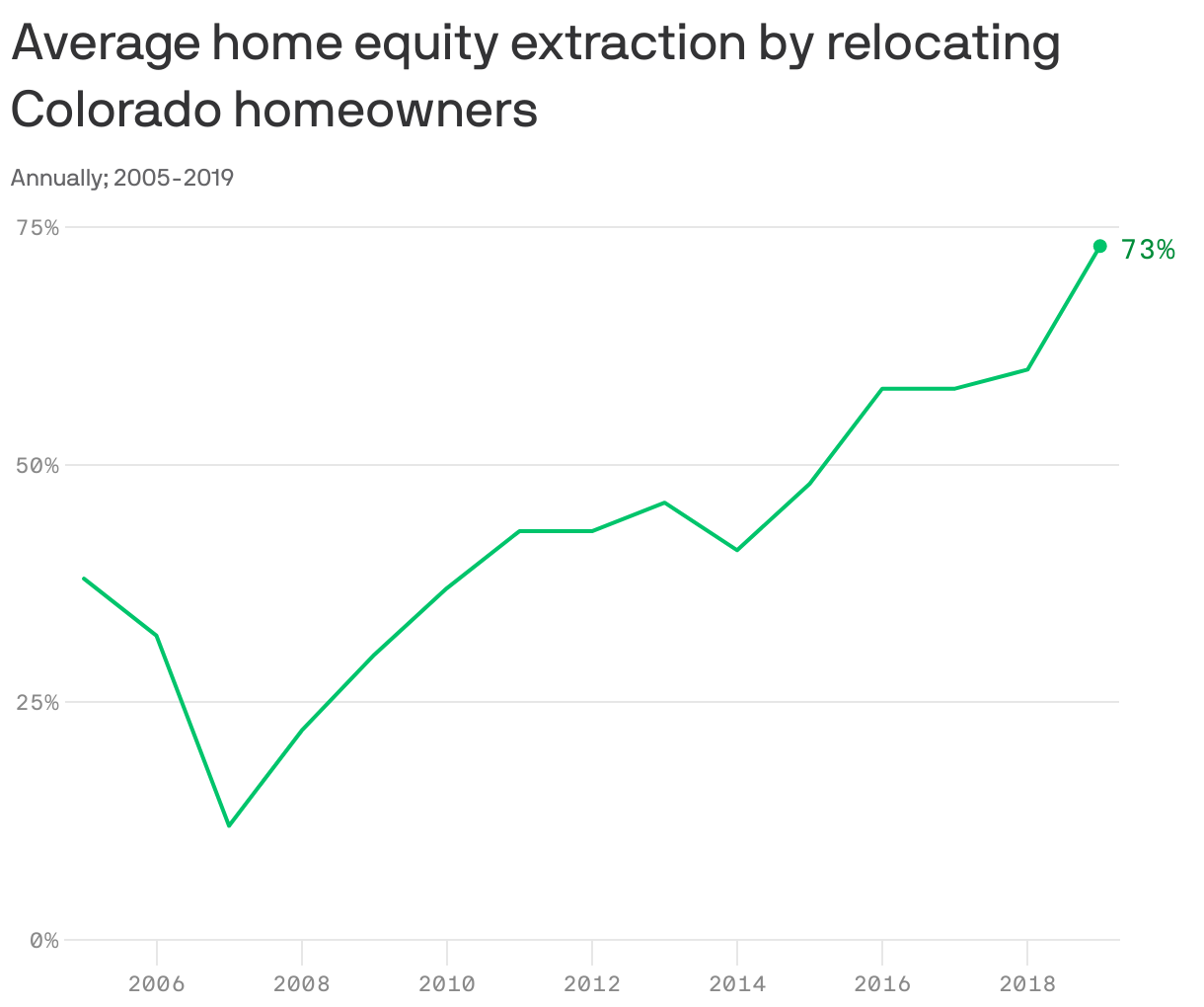

Data: Vanguard; Note: Average difference in value between the house being sold and the house being bought, expressed as a percentage of the value of the house being bought; Chart: Tory Lysik/Axios Visuals

When Americans retire, they often move from expensive areas to cheaper ones. That frees up home equity that can rival or even exceed retirement funds held in 401(k) plans and the like.

Why it matters: People still need a place to live in retirement and rarely take advantage of reverse mortgages to get money out of their homes. Moving somewhere cheaper, however, is much more common.

The big picture: This weekend is key to determining if the situation escalates from an inconvenience to a crisis for SVB clients, most of which are businesses that need to meet payroll.

/2023/03/10/1678406678679.gif?w=3840)