How Americans are using their homes to fund retirement

Add Axios as your preferred source to

see more of our stories on Google.

When Americans retire, they often move from expensive areas to cheaper ones. That frees up home equity that can rival or even exceed retirement funds held in 401(k) plans and the like.

Why it matters: People still need a place to live in retirement and rarely take advantage of reverse mortgages to get money out of their homes. Moving somewhere cheaper, however, is much more common.

Be smart: The people buying in expensive cities and states are the younger generations who want to live near good schools or high-paying employers. The cash they're borrowing in the mortgage market is being turned into retirement money for older Americans.

By the numbers: About 80% of Americans over the age of 60 are homeowners, per a new Vanguard report entitled "Home is where retirement funding is."

- By relocating, the median American over 60 can unlock about $100,000 of home equity — and even more if they downsize at the same time. That's a meaningful sum given that the same median American retiree has about $223,000 in financial retirement accounts.

Where it stands: About 25% of U.S. retirees sell their homes and relocate to somewhere cheaper over any given 10-year period, per Vanguard's Kevin Khang, one of the authors of the report.

- That doesn't just free up cash; it also reduces their day-to-day living expenses.

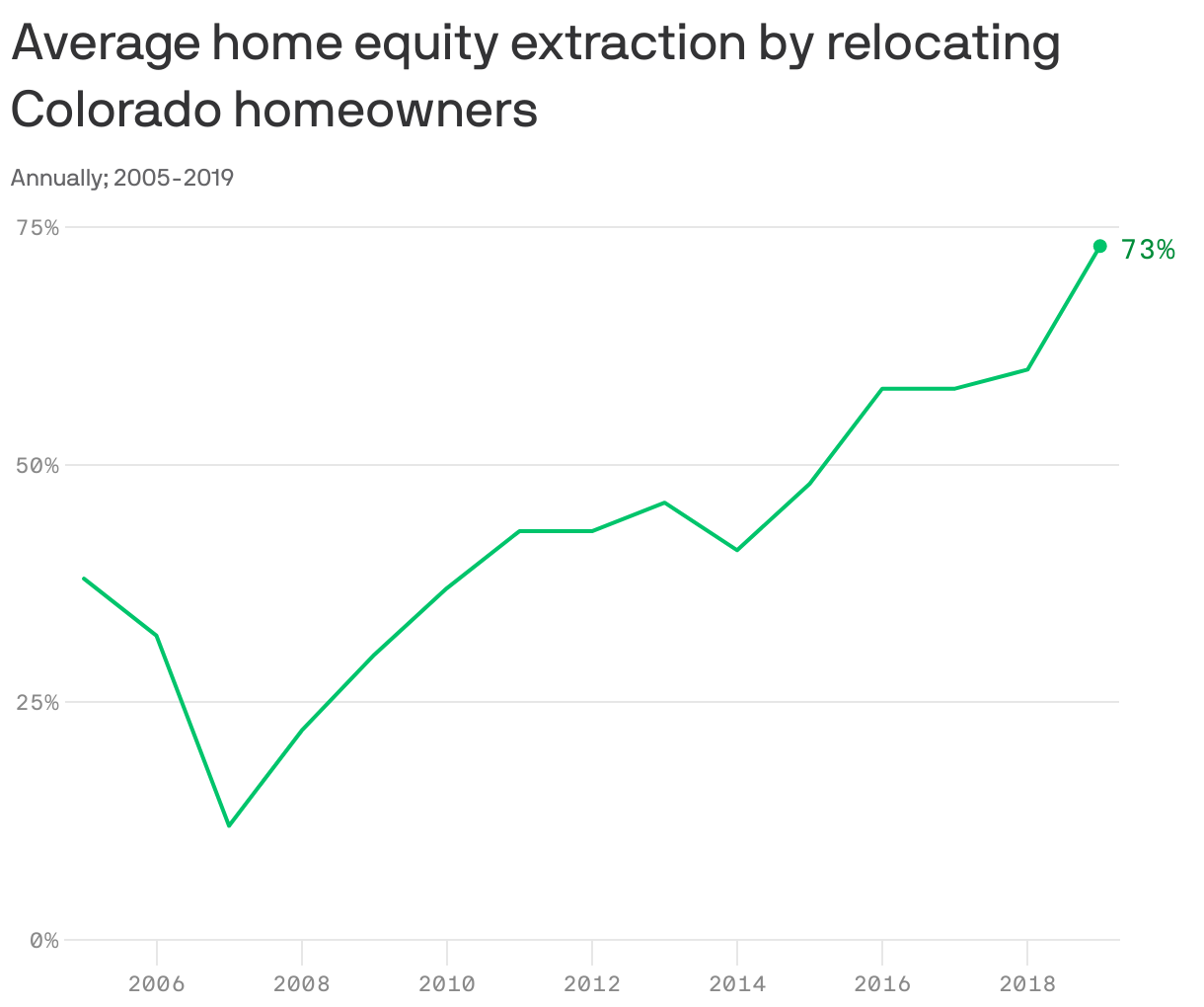

How it works: Let's say a homeowner sells her house in Denver for $600,000, and moves to a similarly-sized house in Florida costing $400,000. That means she's cashing out to the tune of $200,000 — 50% of the value of the new home.

- In fact, in 2019, that ratio averaged 73% in Colorado, up from just 12% in 2007.

- "Given what happened to housing values in Colorado during the pandemic, it's very likely that this number is even higher now," says Khang.

- Other states with lots of cashing-out potential include California (77%) and Hawaii (116%). Importantly, the cashing-out figures include moves within the state, not just moves to a different state entirely.

The bottom line: High housing prices are not the reason why younger Americans move to expensive cities and suburbs. But "when you’re retiring, you’re hyper sensitive to retirement resources," says Khang.

- For older folks who moved to expensive neighborhoods when they were younger, those resources often include their home — which can prove to be a source of substantial liquidity.