Multiple FEMA staff who signed an open letter criticizing the Trump administration's budget cuts to disaster preparedness were placed on leave Tuesday, the Washington Post first reported.

The big picture: Among the workers who signed the letter are "individuals who were directly helping relief efforts in Kerr County, Texas" following July's deadly floods, said a spokesperson for Stand Up for Science, the nonprofit that publicized the declaration, in a Tuesday night email that called the administration's action "illegal."

A forthcoming Trump administration plan to make Cold War-era plutonium available to power companies for reactor fuel deserves a close look, nuclear industry officials said Wednesday.

Why it matters: Experts in arms control and nuclear safety say the idea — which would repurpose plutonium from dismantled warheads — is costly and dangerous.

Uber has placed a lot of robotaxi bets lately, but the three-way deal it struck last month with Nuro and Lucid could be the most consequential — not just for the partners, but for the entire industry.

Why it matters: It's a high-profile experiment to figure out the economics of robotaxis and, perhaps more importantly, to identify a business model that can be profitable for all.

U.S. infrastructure investing is becoming unstable, particularly when it comes to renewable energy projects.

Driving the news: The Trump administration last week ordered a stop to work on an offshore wind farm in Rhode Island, even though 65 of the 85 turbines already are installed.

The Net-Zero Banking Alliance, hit by an ongoing wave of defections, is pausing work while weighing a new structure, the UN-affiliated group said Wednesday.

Why it matters: It's a stark sign of the ESG pullback on Wall Street and the financial sector more broadly, though many banks say they remain committed to low-carbon transition.

President Trump's Interior Department intends to yank late Biden-era permits for a large planned project off Maryland's coast, new court filingsshow.

Why it matters: The motions on US Wind's Maryland Offshore Wind Project are the latest sign of Trump 2.0's escalating efforts to thwart coastal turbine plans.

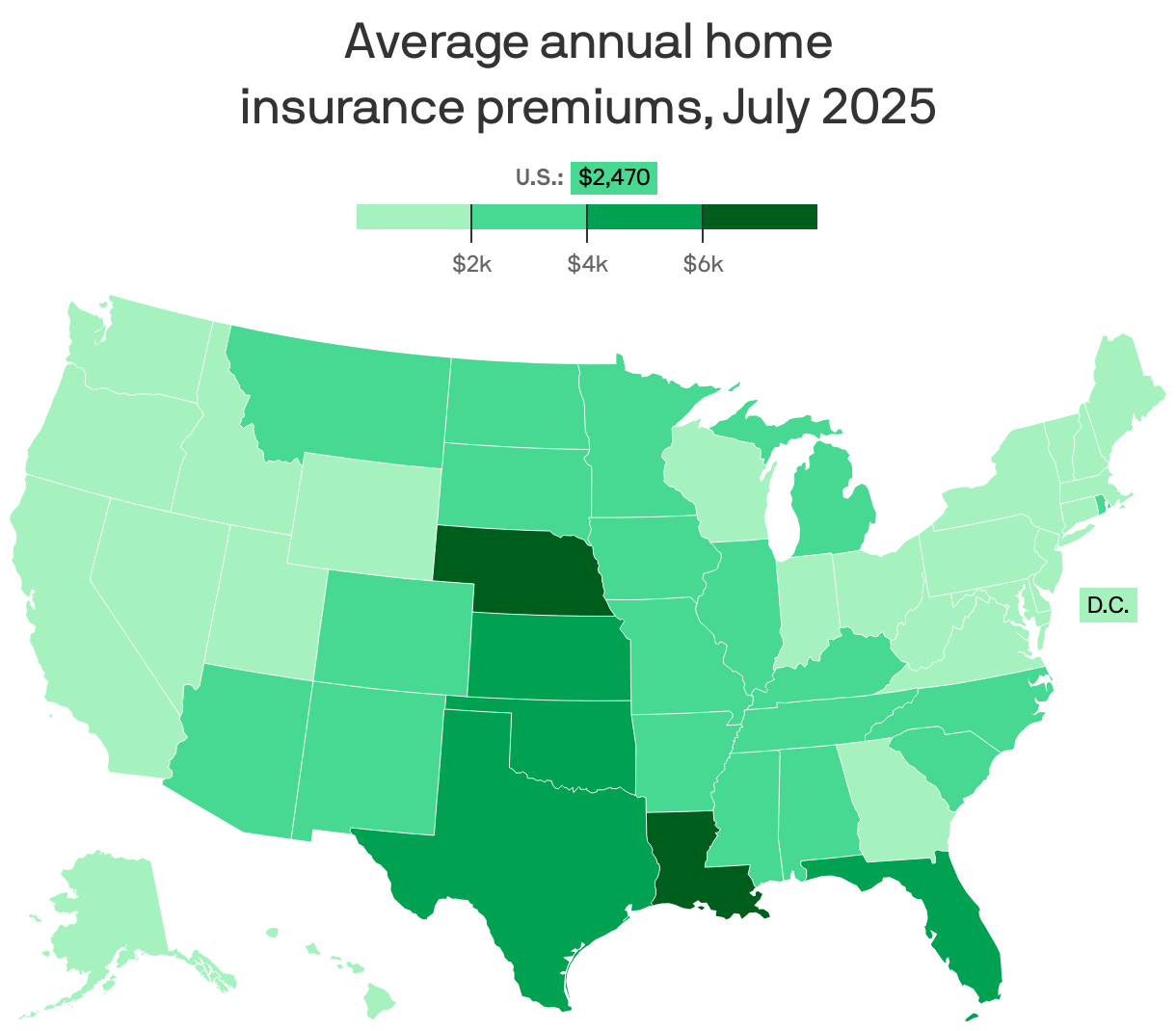

Extreme weather is driving sky-high home insurance prices in some especially storm-prone parts of the country, a new analysis finds.

Why it matters: Climate change is supercharging extreme weather events like hurricanes, increasing the odds of losses and claims and driving up insurance premiums.

Driving the news: The national average for annual home insurance premiums is up 9% since 2023, per a new Bankrate breakdown, hitting $2,470 as of July.

That's based on quotes for married male-female homeowners with an eight-year-old $300,000 home, a clean claim history, and good credit.

Zoom in: Nebraska ($6,425), Louisiana ($6,274) and Florida ($5,735) are just some of the states with shockingly higher-than-average premiums, Bankrate found.

All three are vulnerable to extreme weather, including hurricanes, tornadoes, wind, hail and more.

Caveat: These figures don't include flood insurance.

Stunning stats: Homeowners in the New Orleans metro spend nearly 17.5% of the area's median annual income on home coverage, Bankrate found.

Those in the Miami metro spend nearly 13.4%.

Yes, but: Some places with relatively high average homeowner premiums also have higher median incomes.

In the Denver metro, for example, "the average $300,000 home insurance policy costs $3,644 per year ... but homeowners there earn a median annual income of $103,055, resulting in just 3.54% of their pay going toward premiums," Bankrate says.

"From 2023 to 2025, home insurance costs in Florida decreased by an average of $579, representing a 9% drop," per the analysis.

Between the lines: Climate change is driving non-renewals in some areas, a Dec. 2024 Senate Budget Committee report found.

Non-renewals are correlated with higher premiums and are "often an early warning sign of market destabilization," per the report.

"Premiums are skyrocketing, insurers are non-renewing customers or pulling out of risky markets altogether. As climate change gets worse, insurance availability and affordability will also get worse."

Reality check: The amount you'll actually pay for home insurance depends on many factors — not least of which is your credit score, but also the cost of your home, its materials, and other variables.

Go deeper: Soaring home insurance rates are acting as a "stealth inflation driver," Axios' Emily Peck reports.