The largest Powerball jackpot of the year grew again after no one matched all of the numbers in Saturday night's drawing.

Driving the news: The jackpot for Monday’s drawing is an estimated $1.55 billion — with a cash value of $679.8 million — the nation's fourth-largest lottery prize ever.

Best known for his relentlesspublic criticism of Google as a monopoly, longtime Yelp public policy chief Luther Lowe has a new gig: heading up policy efforts for Y Combinator.

Why it matters: Startup-land has historically shied away from politics, but the famed Silicon Valley accelerator is now embracing it head on.

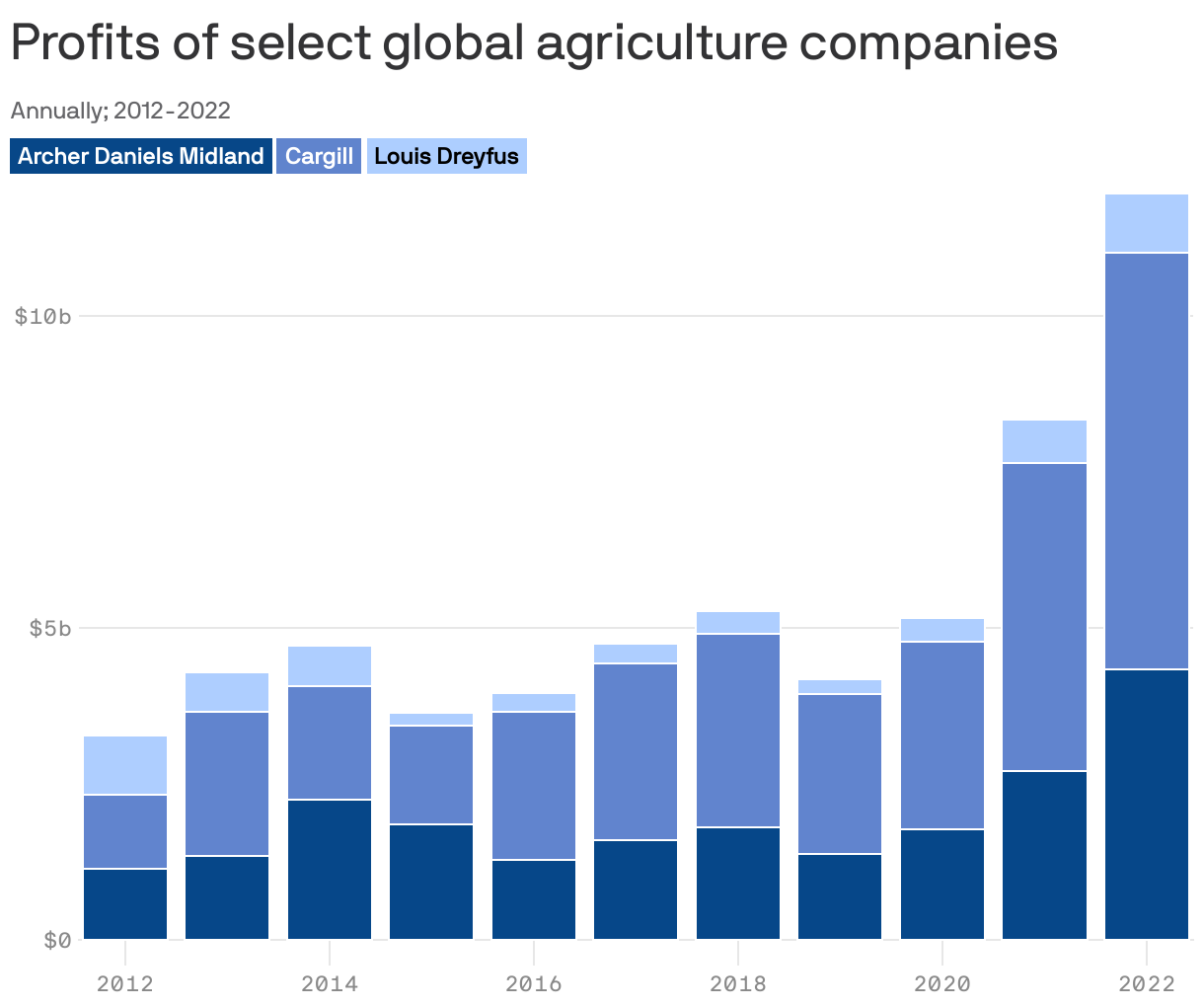

We're in a major hunger crisis — and private corporations are reaping the benefit.

Why it matters: The largest food-trading companies have the status of oligopolies and have become "unregulated financial institutions," according to a blistering 29-page chapter of the 2023 UNCTAD trade and development report, entitled "Food Commodities, Corporate Profiteering and Crises."

The main reason mortgage rates are so high — closing in on 8% — is just that long-term interest rates are high. But the main reason mortgage rates are so much higher than other long-term rates is that U.S. mortgages can be prepaid without penalty.

Why it matters: Prepayability is broadly great for homeowners, since it gives them the ability to refinance whenever rates come down. By the same token, however, it's bad for lenders, who are now charging a lot of money to cover their prepayment risk.

The interest rate on a 30-year fixed-rate mortgage is the second most salient price in the American economy, after only the price of gas. And it looks like it's going to hit 8% sooner rather than later.

Why it matters: A world of 8% mortgages is one Americans haven't seen in over 23 years. The last time mortgage rates were that high, Bill Clinton was president, Brad Pitt married Jennifer Aniston, and Apple Computer was worth $15 billion — a mere 0.5% of its current value.

Everything you thought you knew about moral hazard in the banking system is probably wrong. That's the provocative yet compelling message from a new paper by two economic sociologists, Kim Pernell and Jiwook Jung.

Why it matters: Policymakers worry greatly about deposit insurance and the way in which it allows or even encourages excessively risky behavior on the part of banks. That moral-hazard argument is often given as the prime reason why deposit insurance shouldn't be increased to, say, $25 million.