Friday's economy & business stories

Pudgy Penguin NFTs see floor price rebound

There was an insurrection in the world of Pudgy Penguins in January, when owners of the popular NFTs revolted against its creators, pushing them to sell the collection to a new owner in April.

State of play After an initial surge in excitement, it took the new management a little bit of time to get the house in order, but recent upswings in price suggest the sale is working out.

Credit card charge disputes on the rise as consumers cheat businesses

Consumers are cheating businesses out of payments at increasing rates by fraudulently disputing credit card charges that they genuinely made.

Driving the news: Incidents of "friendly fraud" are up anywhere from 20% to 30% in 2022 depending on the market, Visa chief risk officer Paul Fabara tells Axios.

Exclusive: SBF secretly funded crypto news site

The Block, a media company that says it covers crypto news independently, has been secretly funded for over a year with money funneled to The Block's CEO from the disgraced Sam Bankman-Fried's cryptocurrency trading firm, sources told Axios.

Why it matters: The payments, which employees of The Block were previously unaware of, could undermine the news company's credibility and cast doubt on its coverage of Bankman-Fried, the now-bankrupt FTX and Alameda Research, Bankman-Fried's trading firm.

The rule that silences the White House on economic data

Within a few minutes of major economic data releases, news organizations send out alerts, analysts push out research notes, and Economics Twitter parses the details and implications.

- But White House officials — who presumably have the most reason to celebrate a good number, or explain away a bad one — have to keep quiet until well after the initial flurry of discourse has passed.

Why it matters: It is a case study in how rules set in a different era can long outlive their practical usefulness — and in this case, oddly limit economic debates.

Catch up quick: A Nixon-era rule says executive branch officials must keep mum on a range of indicators for a full hour after the release.

- Some former and current economic policy officials view this as outdated and inconvenient in an era of fast-moving information. But no one, it seems, has been able to update it.

Driving the news: Upon entering office, officials across several administrations, including the current one, were at first puzzled by one sentence in the nearly 2,500-word directive, which states: “[E]mployees of the Executive Branch shall not comment publicly on the data until at least one hour after the official release time.”

- The rule also spells out that economic data must be issued in a press release or another printed report, and indicators must be consistently released at a pre-determined time.

At the very least, the rule proved to be a major scheduling annoyance.

- During the Obama era, the departure of Air Force One would have to be delayed in a few instances so President Obama could comment on good jobs numbers and still be in compliance with the rule, former Council of Economic Advisers chair Jason Furman tells Axios.

- “In a world where every analyst can post and share detailed thoughts on the data on Twitter and elsewhere minutes after, it is fanciful to believe that the government can really do much to shape the interpretation of the data,” Furman says.

Flashback: In 2019, the Trump administration — which broke the rule at least twice — explored changing it. That hit a dead end after worried responses from the statistics community.

What they’re saying: “There is a lot to be said in favor of letting the data speak for themselves,” says Jim Stock, another Obama administration CEA member.

- Still, “the one hour rule is fairly old and with modern information technology that could potentially be shortened, so it is easier to get the White House perspective into the conversation,” says Stock (who adds that he, of course, abided by the directive).

The backstory: When the rule was first instituted in the early 1970s (and strengthened in 1985), there was no social media, cable news — and certainly no instant analysis by Econ Twitter.

- There were, however, rampant concerns among statistics wonks that lines could be muddled between neutral descriptions of economic data from statistics agencies and political statements from the White House.

- There were simultaneous, yet opposing characterizations of labor market developments in 1971 — one from the technocrats at the Bureau of Labor Statistics and another from the White House, which painted a rosier picture, according to a written history of the BLS.

Where it stands: The one-hour rule was meant to draw a bright line between the policy-neutral statistics and political commentary so the public knew the difference.

- “Holding commentary for a while to allow data to be absorbed and analyzed by the market makes sense to me,” says Laura Tyson, who served as President Bill Clinton's CEA chair in the early 1990s.

The bottom line: “While watching Jobs Day tweets roll in without being able to say anything ourselves is not the most fun White House ritual, we are not discussing any changes to the one-hour rule," a White House spokesperson tells Axios.

Good news/bad news on wholesale inflation

This morning's inflation news is either good or bad, depending on the eye of the beholder. November's Producer Price Index suggests price pressures are indeed receding — but not quite as fast as analysts had thought.

Driving the news: Wholesale prices are up 7.4% for the 12 months ended in November, down from 8.1% in the year ended in October, and the lowest reading since May 2021.

- But core PPI — which excludes food and energy — rose 0.4%, compared to the 0.2% forecasters had expected. It shows price pressures aren't dissipating as rapidly as they seemed.

- Food prices rose 3.3% in November alone, which could weigh on Americans' budgets.

What they're saying: "With Food PPI rising strongly in November, one can be sure to see continued upward pressure on household grocery bills as those producer prices are passed on to the retail level," said Kurt Rankin, senior economist at PNC.

- "The holiday shopping season will likely be accompanied by plenty of restaurant goers as well, meaning higher costs for the ‘Food Away from Home’ category," Rankin said in a note.

What's next: The more widely-followed Consumer Price Index for November is due out Tuesday morning. Analysts expect it to show an 0.3% rise in consumer prices last month, down from 0.4% in October.

How ChatGPT could disrupt the business of search

/2022/12/08/1670531574610.gif?w=3840)

A new artificial intelligence thingamajig called ChatGPT set the internet abuzz this week.

Why it matters: Essentially an artificial intelligence (AI) interface that texts you like a know-it-all human, ChatGPT could portend major disruptions ahead for Big Tech — particularly for the business of search.

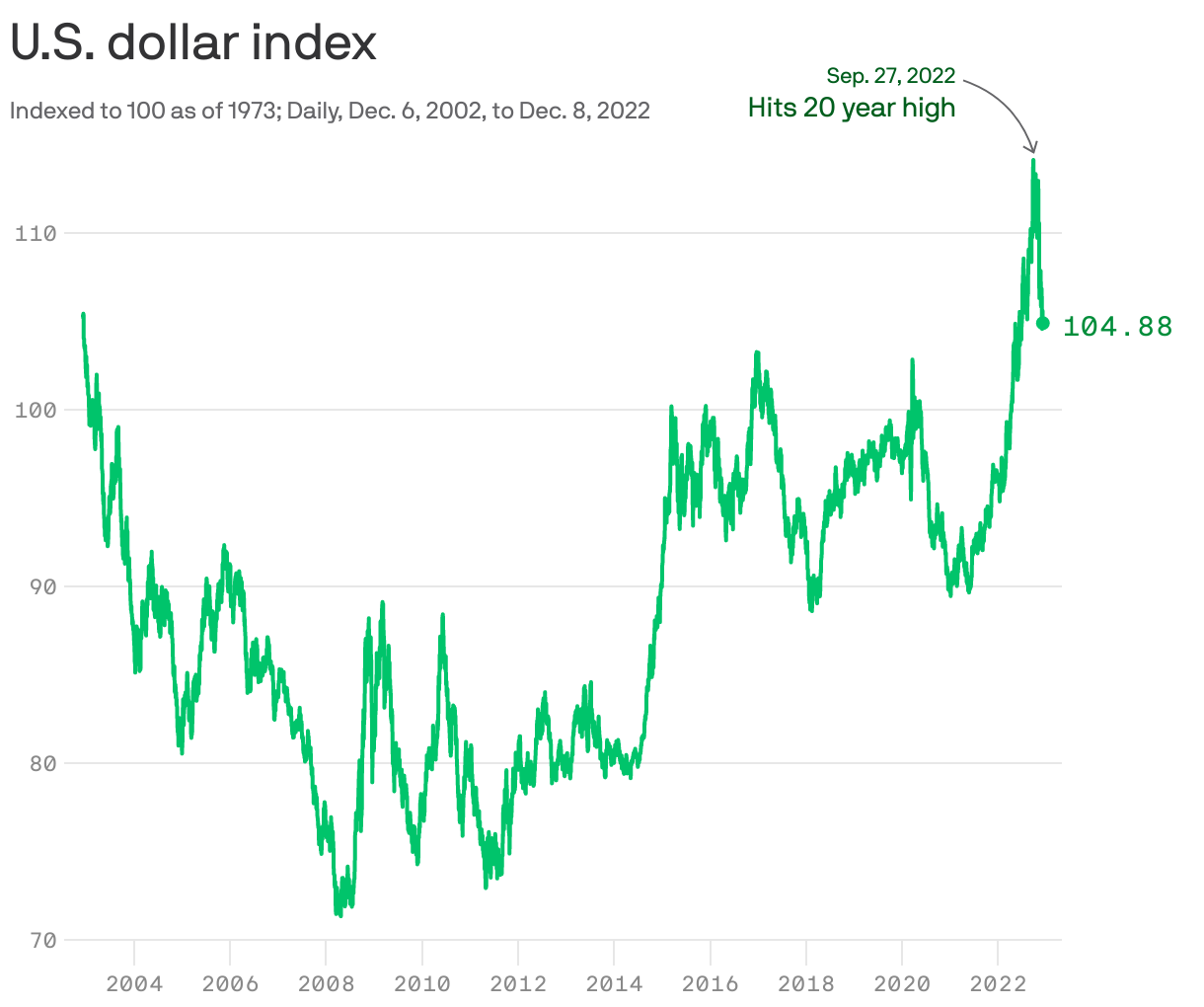

Greenback's slump could signal good news for economy

After hitting a 20-year high this fall, the dollar is now weakening fast.

Driving the news: The U.S. dollar index — which tracks the buck against a basket of six other major currencies — is down more than 8% from its September peak.

Mortgage rates are falling

The average 30-year fixed mortgage rate fell for the fourth straight week, to 6.33%, according to Freddie Mac. It's a big retreat since rates went over 7% during early November.

Why it matters: The long stretch of declines is a sign that inflation worries are easing, as the Federal Reserve is expected to start slowing its aggressive rate-hiking campaign.

Over-the-top cruise ship amusements

When it comes to amusement park rides, cruise lines are playing a game of one-upsmanship.

Why it matters: The pandemic left the cruise industry for dead, but lately it has come roaring back, thanks in part to an aggressive PR campaign and new attractions.

VA official hopes laid-off tech workers will take on a new mission

The U.S. Department of Veterans Affairs is hoping that the recent wave of tech layoffs could help it fill around 1,000 open positions in areas ranging from cybersecurity to software development.

Why it matters: The VA serves over 9 million veterans in more than 2,000 locations, but its digital transformation efforts have been hampered by tech talent shortages.

Portable lavatories go upscale

Portable toilets with bluetooth stereo systems, hot and cold running water, LED lighting, hand sanitizer, air conditioning and plush rolls of paper are starting to pop up across the country, to the surprise (and relief) of outdoor bathroom-seekers.

Why it matters: The COVID-19 pandemic raised our hygiene standards and expectations — and highlighted the critical shortage of public restrooms in the U.S., particularly in cities.

Musk's second "Twitter Files" claims "secret blacklists"

Outside journalists working with Twitter owner Elon Musk posted a new batch of internal communications from the company Thursday night with what they said was evidence the firm's employees "build blacklists, prevent disfavored tweets from trending, and actively limit the visibility of entire accounts."

Why it matters: Musk has framed the "Twitter Files" as an effort to show that his predecessors at Twitter engaged in censorship. Others, including experts in online platforms, say the documents just depict Twitter executives imperfectly but conscientiously struggling to apply complex policies in difficult cases.

Boeing retiring iconic 747 jet

The last-ever Boeing 747 airplane left the company's Washington state factory this week, ending production of the iconic jet after half a century soaring the skies.

Why it matters: The world's first twin-aisle aircraft transformed global travel after making its debut in 1970.

Axios Finish Line: Why you should start a company

I was among the most unremarkable, underachieving, unimpressive 20-year-olds you would have stumbled across in 1991.

- Reeling with a 1.491 GPA, I drank copious amount of beer, smoked Camels and delivered pizza.

- There was good reason my high school guidance counselor told my deflated parents there was no way I was college-bound after graduating in the bottom third of my 100-person class at Lourdes Academy in Oshkosh, Wisconsin.

- And good reason I had to attend the University of Wisconsin-Menasha Extension, a two-year school just to smuggle myself into the University of Wisconsin-Oshkosh, a four-year one in my hometown. It took years to erase that 1.491 pearl.

Why it matters: The fact that 30 years later I have helped start three companies, Politico, Axios & Axios HQ — creating nearly 2,000 jobs — shows what an amazing place America is for ordinary people to build businesses.

- Too many people too often whine about America’s flaws. But there is no better place to start a company. And no better time to do it than now.

Here are five reasons why you should consider launching — or joining — a startup:

1. It beats the hell out of working for the man. Few things are more liberating or intoxicating than controlling your own fate. Yes, it’s terrifying. But if you are young and/or free of responsibility, take wild risks to do things you truly love — on your terms.

2. Fail up! The best piece of advice I got when I almost chickened out of starting Politico was an aside from a lawyer: “Worst case, you’ll fail up!” Everything you learn by trying and failing proves indispensable in whatever’s next.

3. Discover the real you. Nothing reveals true spirit, grit, and creativity like starting something with a high probability of flopping. It’s easy to be cool, nice and sane when things are easy. Fear and exhaustion unearth unfathomable layers.

4. Get a free Masters in psychology. There is no better lens into what makes people tick than watching them work under pressure, on an impossible mission, with total reliance on each other. It’s ugly, beautiful, enlightening, and vitally instructive.

5. Make a difference. Any good entrepreneurial idea solves a big problem for individuals, business or society. If you nail it, you make the world a better place and create jobs and wealth for others.

The big picture: Notice what I left out — the possibility of getting rich yourself.

- Do it because you believe in an idea or yourself, not simply to make a lot of coin.

- Chances are you will fail anyway. But, trust me, it’s worth it.

Sam Bankman-Fried ignores Senate request, setting up subpoena

Sam Bankman-Fried missed a Thursday evening deadline for responding to a Senate Banking Committee request that he testify at an upcoming hearing, setting up the possibility of a subpoena.

Why it matters: Bankman-Fried has given a slew of media interviews since FTX collapsed, but hasn't yet spoken under penalty of perjury.