Axios Markets

July 18, 2023

1 big thing: Soft landing comes into view

Illustration: Brendan Lynch/Axios

2. Catch up quick

3. Movie theaters at risk, again

Movie theater operators are the businesses most at risk from a protracted writers' and actors' strike, Moody's Investors Service concludes in a note out yesterday, Emily writes.

Why it matters: Theaters rely on new releases, more so than TV networks or streamers do. If the strikes go on much longer, the pipeline of fresh content may run dry.

State of play: While movie production had been muddling along, even with a writers' strike, the actors' strike that began last week changed the game — grinding all film production to a halt.

The big picture: Theater operators like AMC, Vue Entertainment, and Cineworld are only just emerging, and have not yet recovered, from the horror show of the COVID economy. (h/t to Axios' Tim Baysinger for the chart above)

- "In a prolonged strike in which new theatrical Hollywood tentpole product is spread more thinly or runs dry, these companies could face earnings, cash flow and liquidity pressures," write the authors of the Moody's note.

What's next: The last actors' strike, in 2000, lasted around 180 days.

- If the current strikes go past the fourth quarter — there are 166 days left to the year — there will be bigger reverberations in other sectors of the entertainment industry, including the studios and the TV networks, per Moody's.

- But things could get dire before that. Studio chairs told the New York Times that if the work stoppage goes past Labor Day, it would have a serious impact on next year's release calendar.

Yes, but: For the theater companies, the impact of the strikes isn't likely to be as bad as the hit from the pandemic, when theaters were fully shut down and folks debated if the movies would ever come back.

What to watch: "Barbie" or "Oppenheimer." Theatergoers are expected to flock to these films — Barbenheimer-style — which open this weekend. It could be the industry's last gasp before the strike impact hits.

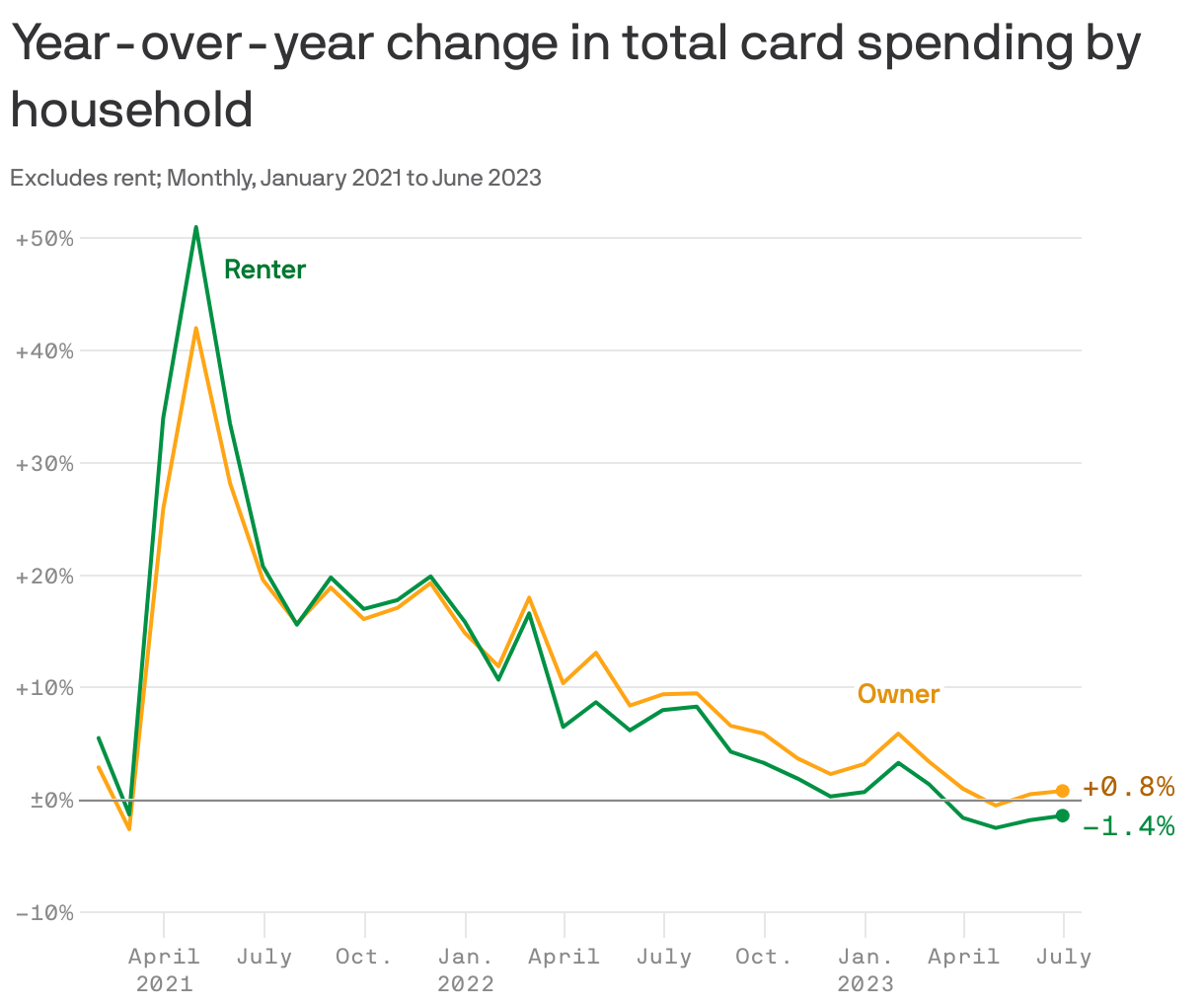

4. Renters vs. owners

Years of staggering rent inflation are taking a toll: Renters are pulling back their spending on non-rent stuff, Axios' Kate Marino writes.

What's happening: Spending growth among renters and homeowners used to largely move together. But starting in early 2022, a gap emerged — renters' spending growth started lagging that of owners, per Bank of America's internal card spending data.

- This year, renters' spending growth has gone negative. In June, it was down 1.4% from a year ago.

Why it matters: It's another way of showing how homeowners who locked in low-rate mortgages before the Fed started hiking rates last year are effectively immune to a major slice of U.S. inflation — housing costs.

- More than 60% of mortgage holders are sitting on rates below 4%.

Details: The spending gap emerged around the time that rent inflation really took off — the consumer price index for rent surpassed its 2018-2019 average in early 2022, according to a report by Bank of America Institute.

- "Renters' spending appears to have been sapped by rent inflation, while homeowners have been somewhat insulated from higher interest rates so far," the report noted.

What to watch: That insulation only benefits homeowners until they have to sell. As more home buyers take on higher mortgage costs — and rent inflation moderates, potentially — that gap could narrow again, BofA Institute notes in the report.

5. Default flip-flop

Just like homeowners, companies with fixed-rate bonds issued during the ZIRP times haven't seen those interest costs go up, Kate writes.

- On the other hand: The cost of floating-rate debt has risen by about 5 percentage points since March of last year.

Why it matters: That helps explain why default rates on floating-rate debt (known as leveraged loans) have been higher than default rates on fixed-rate high-yield bonds, ever since the beginning of 2022.

- Importantly, that's a flip-flop of the long-standing relationship between the two — the chart above shows that high-yield bonds have almost always had a higher default rate.

The background: Both high-yield bonds and leveraged loans are debt borrowed by below-investment-grade companies — meaning, companies with lower credit ratings.

- Loans tend to be secured by collateral and are first in line for repayment if there's a bankruptcy.

- Bonds, typically, are lower in the repayment pecking order and thus cost more — making them more risky for investors and more prone to defaulting.

What they're saying: “Going against the long-term norm, loan defaults are now tracking higher than HY," wrote BNP Paribas U.S. credit analysts in a recent note — adding that “Fed hikes have filtered through more immediately to higher interest expense" for loans.

The bottom line: For homeowners and companies alike, things are tough out there if you didn't lock in your debt costs before the Fed started hiking.

Axios Markets

Stay on top of the latest market trends and economic insights