Student loan repayments starting up for millions of Californians

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Annelise Capossela/Axios

Many San Diegans with student loan debt will face a new monthly bill next week, when payments resume after a three-year pause.

Driving the news: Student loan interests started back up this month, while payments are set to be due starting Oct. 1.

Why it matters: For millions of individuals, the resumption of student loan payments will result in real and often painful spending cuts. Those cuts could also translate to a slowdown for the economy overall, Axios' Emily Peck writes.

- Reality check: Experts say the end to the reprieve won't reduce consumer spending enough to impact the larger economy as some feared.

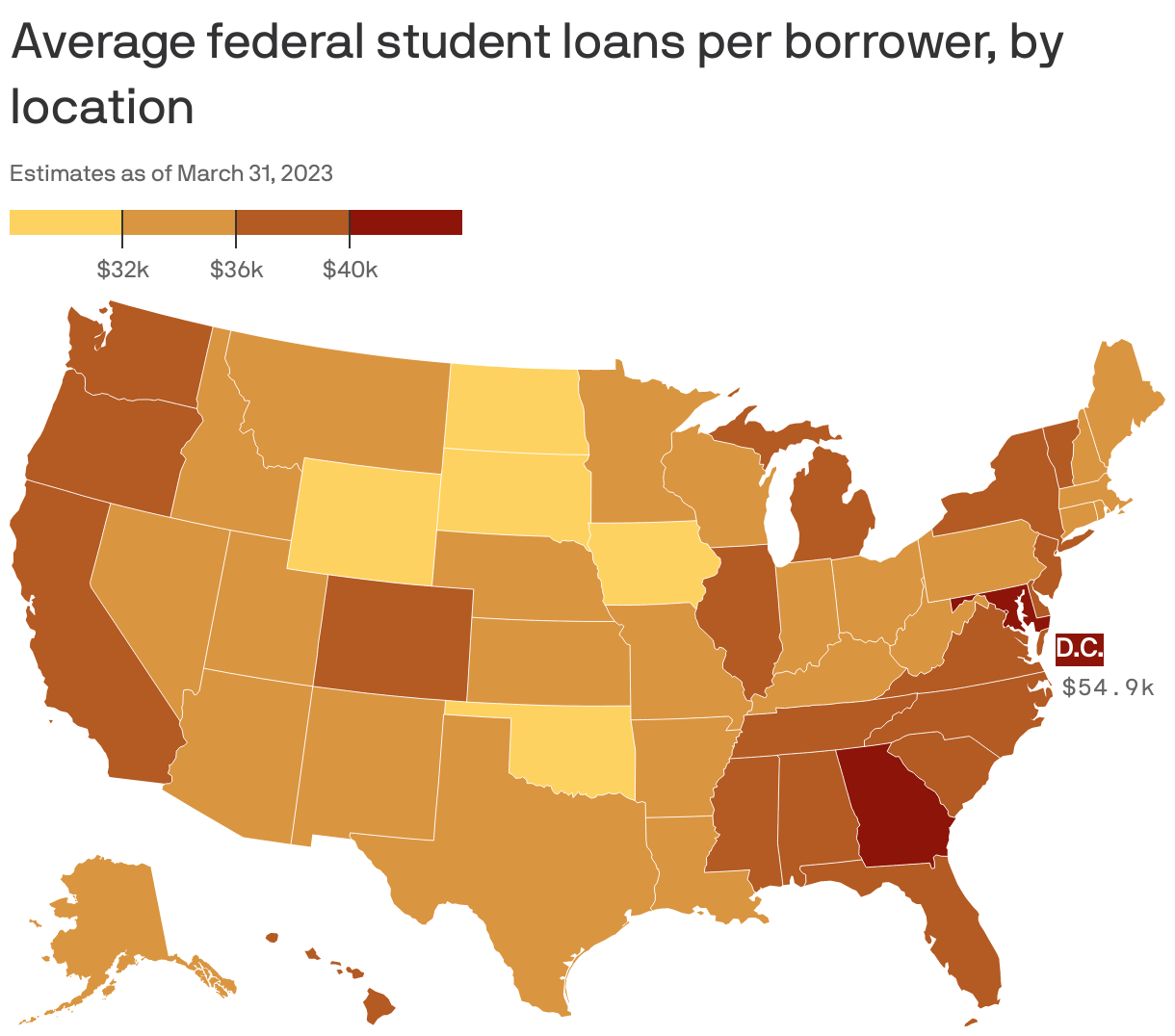

Zoom in: Nearly four million Californians have federal student loan debt that totals more than $149 billion, according to Federal Student Aid data.

- That breaks down to an average of about $37,500 per borrower.

- Yes, but: The majority of California borrowers owe under $20,000.

State of play: Meanwhile, tuition is rising across the California State University System next fall, including at San Diego State University.

- That could affect the system's accolade that more than half of CSU students earning bachelor's degrees graduate without any education loan debt.

Of note: The University of California system also boasts that 57% of undergraduates graduate with no debt at all.

- The average student loan debt for seniors at graduation in 2020–21 was about $18,400.

- That's about a $195 monthly repayment over ten years, just below the national average of $200-$300 for student-loan borrowers.

Zoom out: Nationally and in California, borrowers between 35 and 49 years old owe the most in federal student loans.

- Women and Black borrowers also face higher student loan burdens than their male and white counterparts.

Flashback: The Biden Administration wiped out student loan balances for almost 62,000 Californians who'd been paying off loans for 20 or 25 years under a new measure announced in July.

- That measure followed the Supreme Court's decision to strike down Biden's student debt forgiveness plan.

What's next: Borrowers worried about not being able to make payments right away can apply for the new SAVE Plan, an income-driven repayment plan that calculates monthly payments based on income and family size.

- Plus, the Biden Administration is offering a year-long "on-ramp period" where borrowers won't be reported as being in default to the national credit rating agencies over missed payments.

Be smart: Use this Axios explainer to figure out your student loan status before payments resume.

- Borrowers can also calculate their repayment with Federal Student Aid's loan simulator.

🗣️ Tell us: Take this short survey to share how student loans are affecting you.