Flooding risk threatens Philadelphia insurance premiums

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

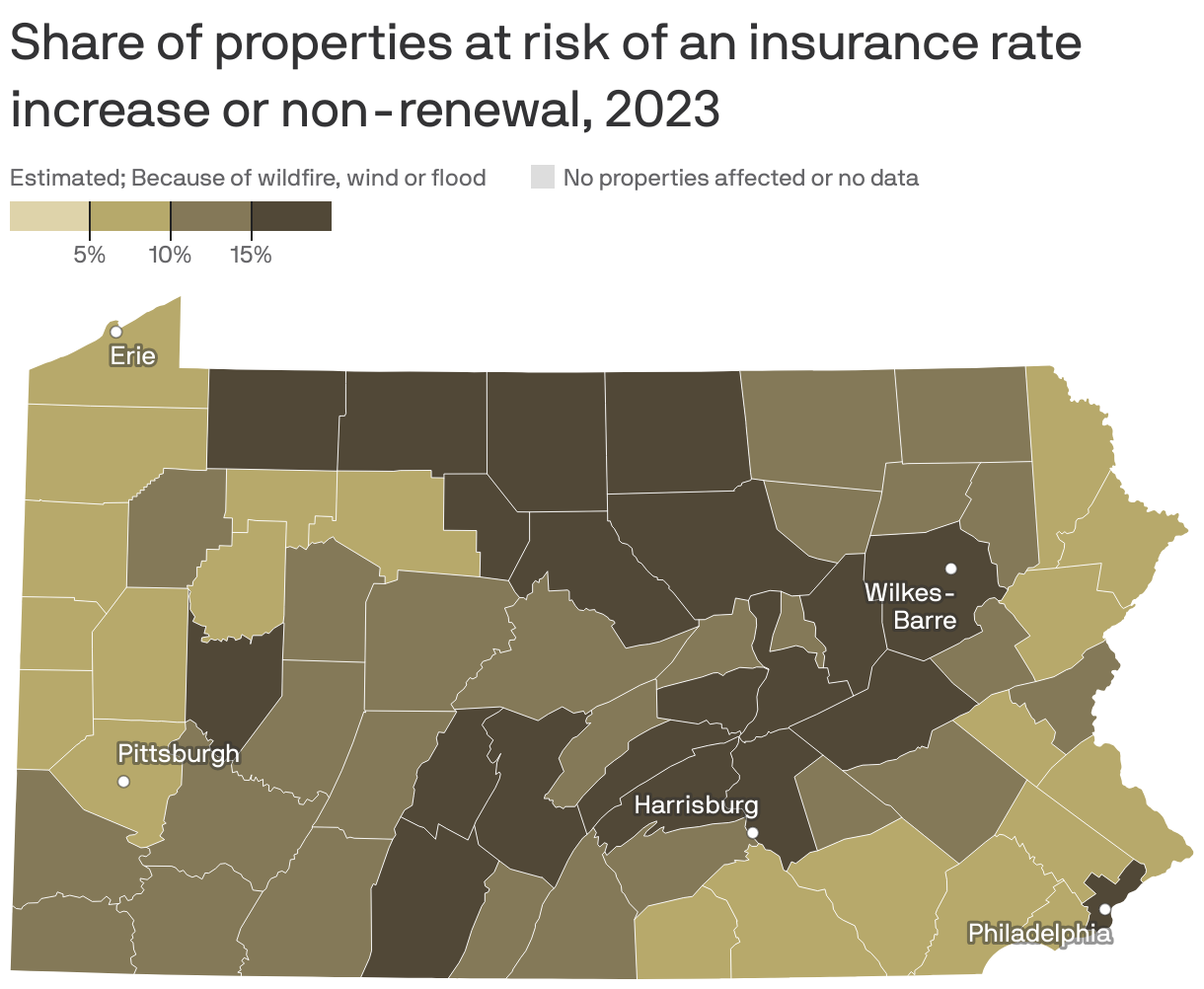

Open embedded content from datawrapper.dwcdn.netAbout 12% of properties in the Philadelphia metro area could be facing higher insurance premiums or policy non-renewals due to the risk of high winds and flooding, per a new analysis.

Driving the news: Insurers are changing how they factor climate and extreme weather risks into premiums. Others are suspending coverage altogether.

The big picture: Millions of properties nationwide could see higher premiums because of these climate- and weather-related risks, per estimates from the First Street Foundation, a climate data nonprofit.

- Nearly 24 million U.S. properties may face higher premiums because of the risk of potential wind damage, about 12 million because of the risk of flooding, and about 4.4 million due to wildfire risk.

What's happening: When it comes to wildfire and wind damage, some private insurers are dropping policyholders as the risk of those threats grows, says Jeremy Porter, First Street's head of climate implications research.

- That's leading many homeowners to opt for public "insurer of last resort" plans — but often at higher rates.

- Rising rates driven by climate- and weather-related risks are particularly pronounced in states like Florida and Louisiana.

What they're saying: While Pennsylvania doesn't have the same risks, Ben Keys, a professor of real estate and finance at the University of Pennsylvania, told WHYY that states like Florida and California can gauge how the industry will respond to climate change.

- "I think of insurance as being one of the very first movers in a much longer chain of responses to climate risk," he said. "They are the most mobile and have the most money at stake in the event of disasters."

Meanwhile, FEMA recently updated its flood insurance pricing model for the first time since the 1970s, leading to higher premiums that are more reflective of today's flooding risks, Porter says.

- The intrigue: Eight million households are in FEMA flood zones, but only 4.7 million have active flood insurance policies.

Zoom in: In Philadelphia, nearly 20% of properties are at risk of insurance increases due to flooding, per the analysis.

What we're watching: Climate and extreme weather risks — and the associated financial costs — are starting to influence where people choose to live, Porter says, but only to a slight degree.

- For example, Florida's population grew from 2020 to 2022, per the latest census data. But Miami — home to the country's most expensive homeowner's insurance — shrunk slightly.

- Miami is still a popular place to live, but people are leaving areas such as South Beach for communities at higher elevations, like Little Haiti, Porter says.