Arkansas home insurance rates among highest in U.S.

Add Axios as your preferred source to

see more of our stories on Google.

Extreme weather is driving sky-high home insurance prices in some storm-prone parts of the country, a new analysis finds — including in Arkansas.

The big picture: Climate change is supercharging extreme weather events like hurricanes, increasing the odds of losses and claims and driving up insurance premiums.

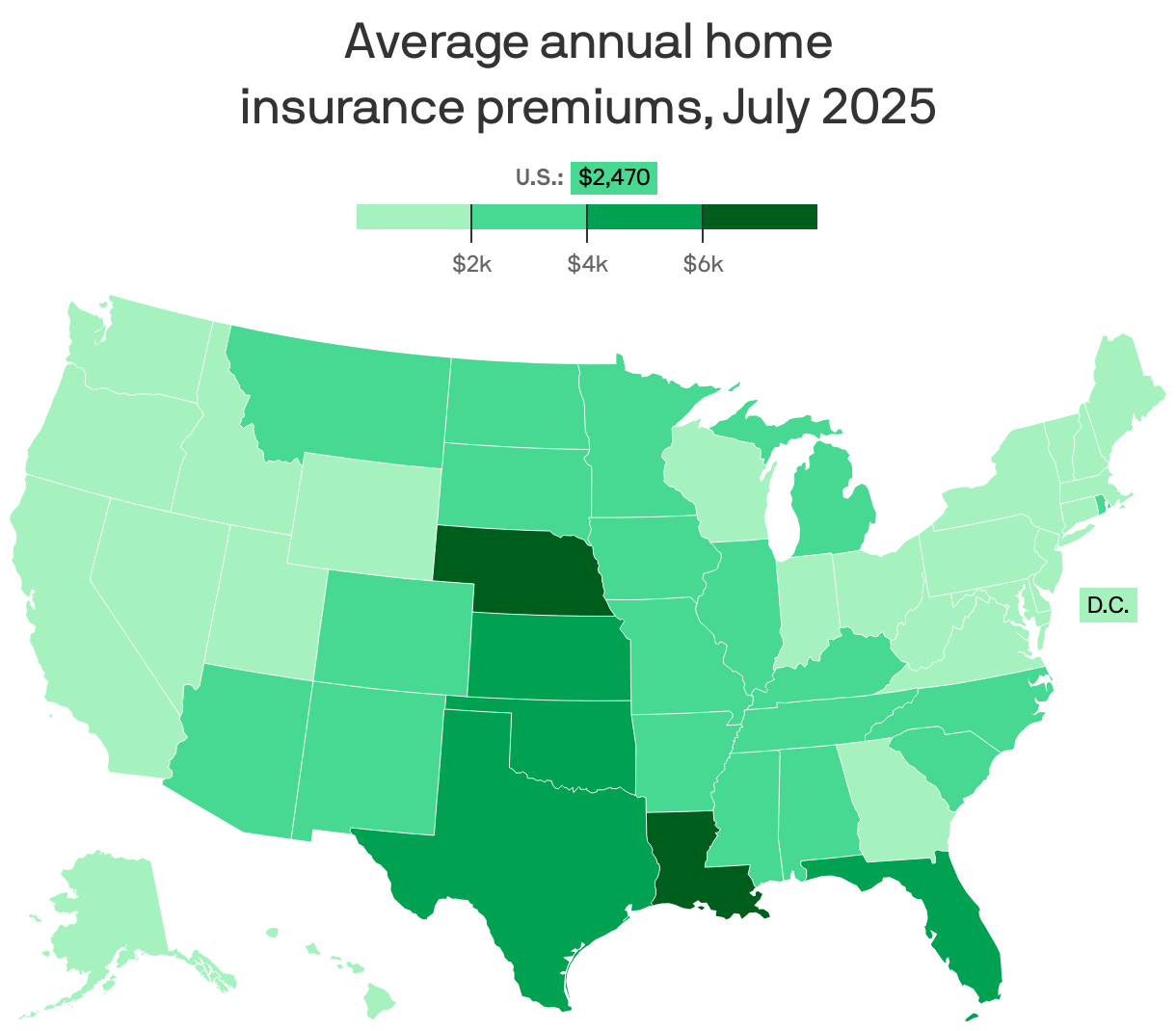

Driving the news: The national average for annual home insurance premiums is up 9% since 2023, per a new Bankrate breakdown, hitting $2,470 as of July.

- The average in Arkansas is $3,103.

- That's based on quotes for married male-female homeowners with an eight-year-old $300,000 home, a clean claim history, and good credit.

Zoom in: Arkansas is the 11th most expensive state, the data shows, following increased tornadic activity in recent decades.

- According to data collected by the Southwest Times Record, there were 601 tornadoes recorded in Arkansas between 1980 and 1999.

- The number jumped to 982 between 2000 and 2019.

Zoom out: Nebraska ($6,425), Louisiana ($6,274) and Florida ($5,735) are just some of the states with shockingly higher-than-average premiums, Bankrate found.

- All three are vulnerable to extreme weather, including hurricanes, tornadoes, wind, hail and more.

Caveat: These figures don't include flood insurance.

Stunning stats: Homeowners in the New Orleans metro spend nearly 17.5% of the area's median annual income on home coverage, Bankrate found.

- Those in the Miami metro spend nearly 13.4%.

Yes, but: Some places with relatively high average homeowner premiums also have higher median incomes.

- In the Denver metro, for example, "the average $300,000 home insurance policy costs $3,644 per year ... but homeowners there earn a median annual income of $103,055, resulting in just 3.54% of their pay going toward premiums," Bankrate says.

- On average, Arkansans pay more than 5.25% of their income for home insurance.

Between the lines: Climate change is driving non-renewals in some areas, a December 2024 Senate Budget Committee report found.

- Non-renewals are correlated with higher premiums and are "often an early warning sign of market destabilization," per the report.

- "Premiums are skyrocketing, insurers are non-renewing customers or pulling out of risky markets altogether. As climate change gets worse, insurance availability and affordability will also get worse."

Reality check: The amount you'll actually pay for home insurance depends on many factors — not least of which is your credit score, but also the cost of your home, its materials, and other variables.

Go deeper: Soaring home insurance rates are acting as a "stealth inflation driver," Axios' Emily Peck reports.