October 15, 2022

Welcome to the middle of October, dear readers!

- 🙏 Reminder: Feel free to send me tips or comments by replying to this email or on Twitter @imkialikethecar.

Today’s Smart Brevity™ count is 1,044 words, a 4-minute read.

1 big thing: The curious case of 2022's venture fundraising

Illustration: Natalie Peeples/Axios

It's becoming increasingly clear that 2021 will be an outlier year in virtually every way for startups... except one. U.S. venture fundraising is on track for a new record this year, per new Pitchbook data.

Why it matters: This incredible amount of capital will be more concentrated than before.

The big picture: With startup funding deals slowing down in 2022, the big question has been whether activity will completely vanish.

- Many experts have pointed to the record amount of dry powder as a clue that it won't, since VCs don't get paid to sit on cash.

Still: Who raises funds (and how much of it) affects how that capital will be deployed in the startup market.

By the numbers: In the first three quarters of 2022, VCs have raised $150.9 billion across 593 funds, per Pitchbook.

- That's compared to the 1,139 funds that raised $147.2 billion in all of 2021.

- So far this year, 62% of the capital has gone to 6% of funds, and in Q3 alone, 86.7% of the money was committed to just 66 funds.

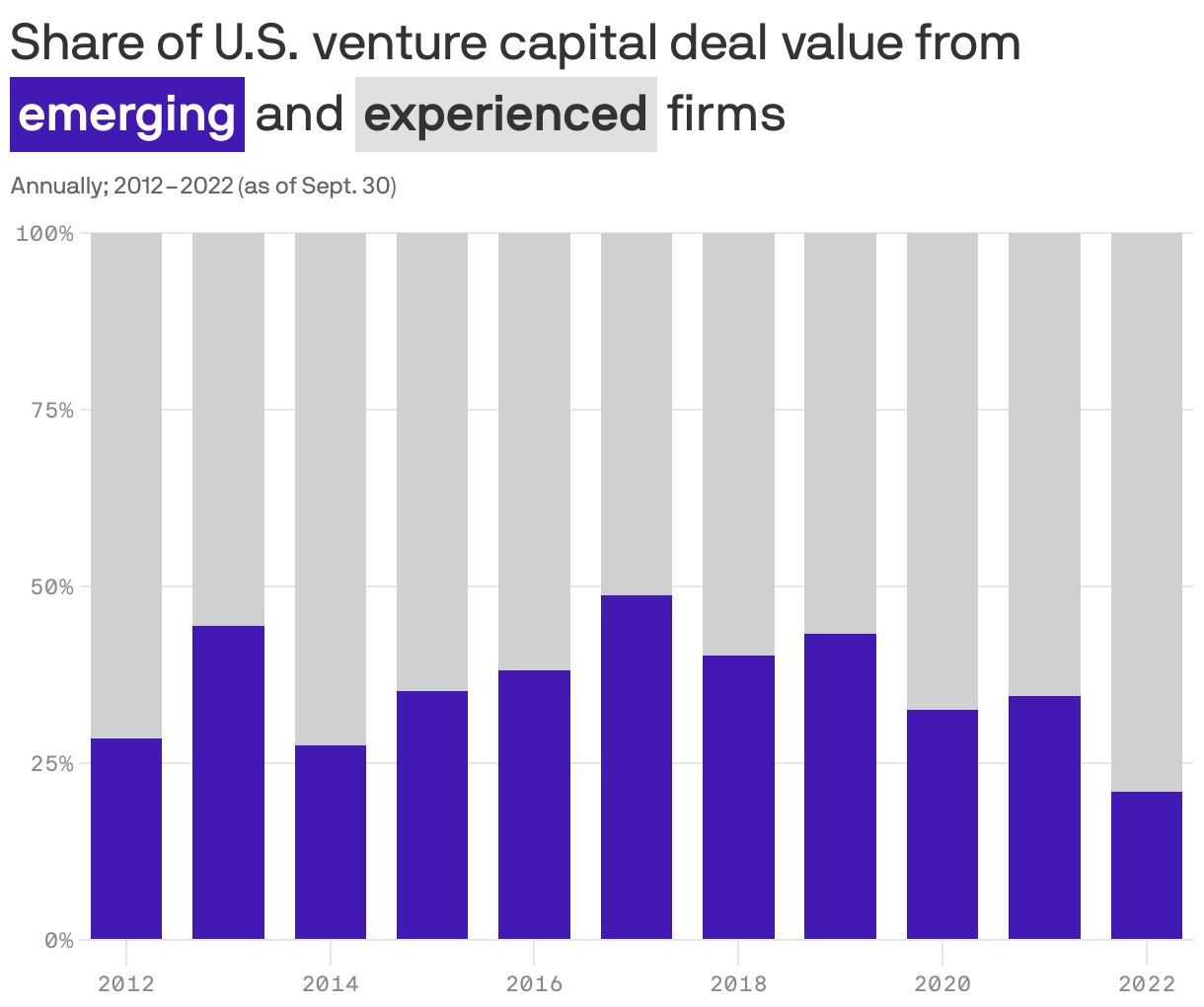

Between the lines: This is bad news for emerging managers as limited partners (LPs) stick to established managers, instead of backing newer ones that could be riskier investments.

- Already this year, the share of dollars that went into experienced VCs is at its highest in the past decade, per Pitchbook.

- The number of first-time managers raising funds this year is expected to fall below 2014 levels, though overall dollars have almost doubled.

- Microfunds, often raised by first-time or emerging managers, have also slowed in fundraising activity.

What they're saying: "Portfolios are overweight so there’s not much room for anything," including emerging managers, Cornell University investment officer Roger Vincent said during a panel at SuperReturn in NYC last month.

- And while there's a bit of natural attrition in portfolios, Vincent noted, it's "smaller than you'd think."

The other side: "From our discussions during our raise, we heard LPs started feeling empowered, even significantly motivated, to say no to new funds from some VCs they’ve felt inertia to stay with despite seeing performance lagging," Primary Venture Partners general partner Brad Svrluga tweeted this week.

- "Everyone’s eligible for the chopping block these days," he added. Still, Primary raised two new funds this summer.

Yes, but: Megafunds are having a great year — a record 35 funds of over $1 billion have raised about $91 billion so far.

- Last year, funds in that category raised just under $51 billion.

What we're watching: How this plays out over the next couple of years as pandemic-era funds get fully deployed; how this year's new capital makes its way into startups; and how returns will compare (many years down the line).

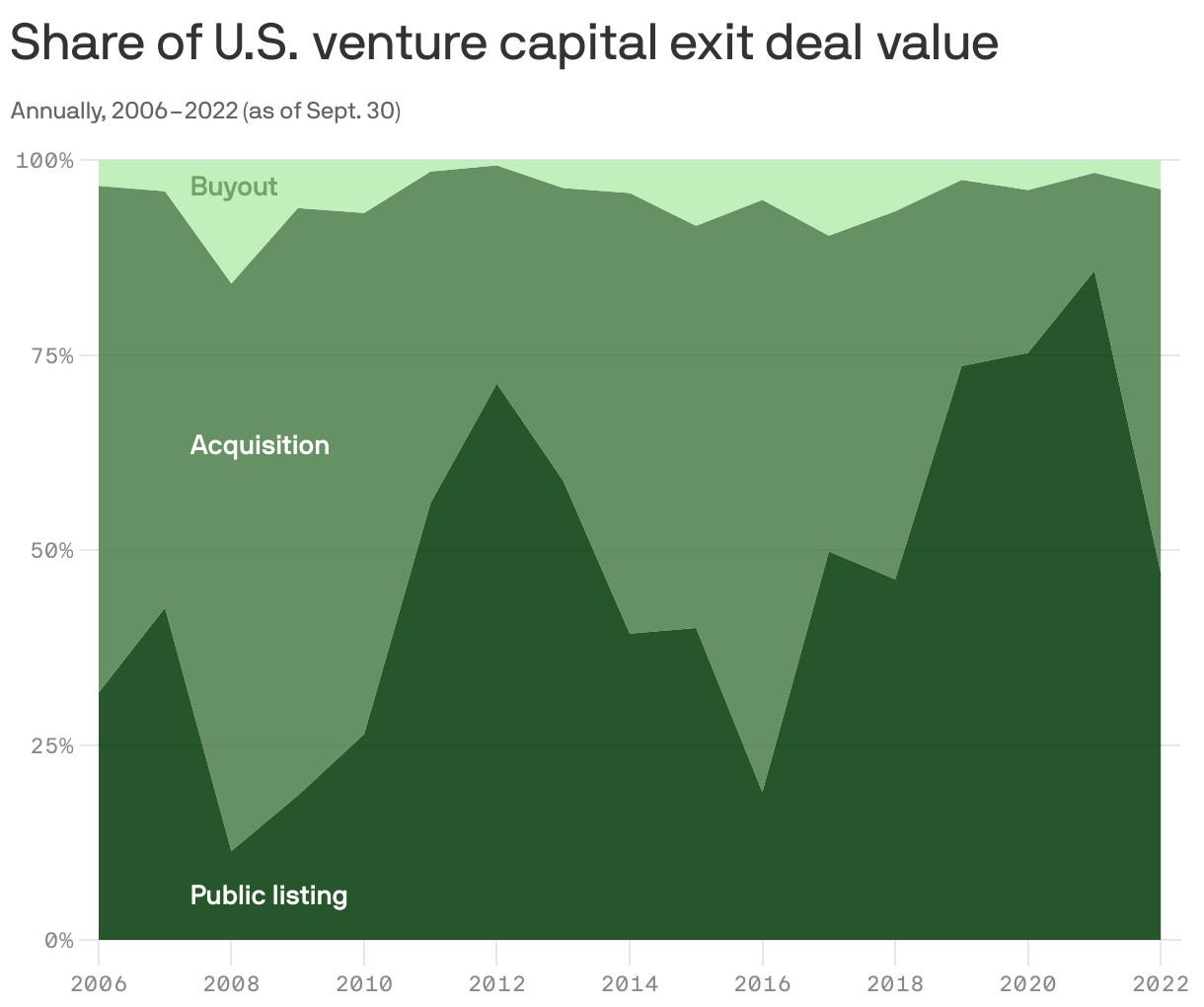

2. 🙏 Unanswered prayers for exits

The data is in, and it has confirmed what everyone's suspected: Venture-backed exits this year are on track to hit a five-year low, per Pitchbook.

Why it matters: Fewer distributions back to VCs' own investors are adding to the ongoing squeeze those investors have been feeling. The market's in turmoil, and many have been stretching their allocations into the asset class during the pandemic boom.

Zooming in: With the IPO window virtually shut most of this year, it's no surprise that almost 50% of exit value so far this year has come from acquisitions.

- The last time acquisitions represented about this portion of exit value was in 2018. Last year, 86% came from public listings, which represented a record 16% of exit counts.

And so far this year, seed-stage startups are the majority of venture-backed companies getting acquired — the highest proportion since at least 2012.

- This suggests that a slew of smaller companies may be opting for a sale amid the more challenging fundraising environment.

Yes, but: One brighter spot is that median acquisition exit value remains above historical figures, at about $100 million. That's up from $66.6 million last year.

- Meanwhile, median public listing and buyout values plunged to $353.6 million and $65 million, respectively (down from $722.5 million and $175 million).

The bottom line: All eyes are on what 2023 holds for exits.

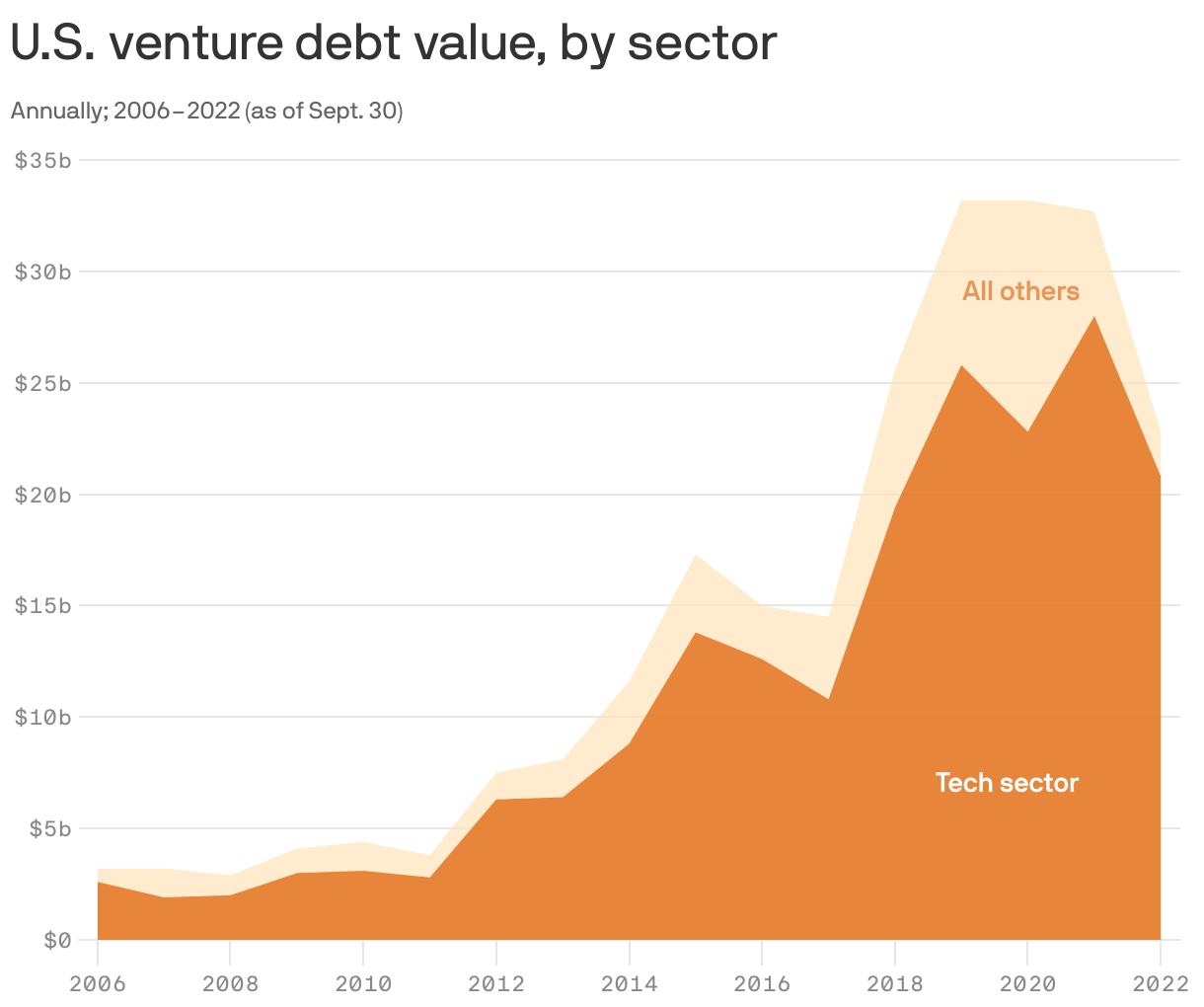

3. 🤔 Who's really venturing into debt...

Venture debt financing so far this year is not as high as the previous three years despite its surge in popularity amid the tighter venture market, per new Pitchbook data.

Yes, but: As expected, most (70%) of the venture debt dollar is going into late-stage companies: Early-stage loans are becoming a smaller portion of overall counts.

Between the lines: Larger, later-stage companies have been the fastest and hardest hit by the public market downturn, as IPO plans evaporated and VCs quickly started to rethink their valuations.

- Debt has become a more popular alternative to provide such companies the cash they need, avoid a down round, and extend their runway as they adjust their fundraising plans.

Bonus: Female founders

There's good and bad news for female founders: On the one hand, capital and deal count for female-founded startups continue to trend upward (excluding 2021's outlier numbers), per Pitchbook.

- On the other: Those startups are getting a smaller portion of capital and deals relative to the overall industry so far this year.

Another bifurcation: While the proportion of financings of late-stage female-founded startups continues to grow, the proportion of capital going into seed-stage startups is also growing.

- This is likely due to a few unusually large early-stage rounds in recent months.

1 👀 thing: The gap in funding and exits for all-female startup founder teams compared to those with mixed genders remains stubbornly persistent.

📚 Due Diligence

- Instacart cuts internal valuation third time, to $13 billion (The Information)

- North American startup funding shrank over 50% in Q3, led by late-stage declines (Crunchbase News)

- A really ugly Q2 for VC (Axios)

🧩 Trivia

Much ink has been spilled over the dramatic drop in 2022's startup funding.

- Question: Is this year on track to surpass 2020 in terms of dollars invested? (Answer at the bottom.)

🧮 Final Numbers

🙏 Thanks for reading! And to Javier E. David for editing and Amy Stern for copy editing. See you on Monday for Pro Rata's weekday programming, and please ask your friends, colleagues and 2022 vintage fund managers to sign up.

Trivia: Yes, and it already has according to Pitchbook data (YTD for 2022: $194.9 billion, compared to $168.7 billion in 2020). However, it's less clear if it will have more or fewer deals.