Axios Markets

March 13, 2023

1 big thing: Trying to quell the crisis

Photo: Philip Pacheco/Getty Images

2. Catch up quick

3. Let the bailout debate begin

Illustration: Lindsey Bailey/Axios

4. Charted: Bond cliff

It’s not just common shareholders in Silicon Valley Bank looking at possible zeroes, Axios' Kate Marino writes.

- The company has borrowed about $7 billion from investors in the form of bonds and fixed-rate preferred shares — and as Matt noted, a senior administration official said bondholders may be “wiped out.”

State of play: SVB Financial Group senior bonds lost about half their value on Friday, trading at an average price of around 48 cents on the dollar, according to MarketAxess' BondTicker.

- Friday’s sellers were lucky. When the bond market opens for trading today, prices will undoubtedly be much lower.

Go deeper: J.P. Morgan, PNC among suitors for SVB holding company

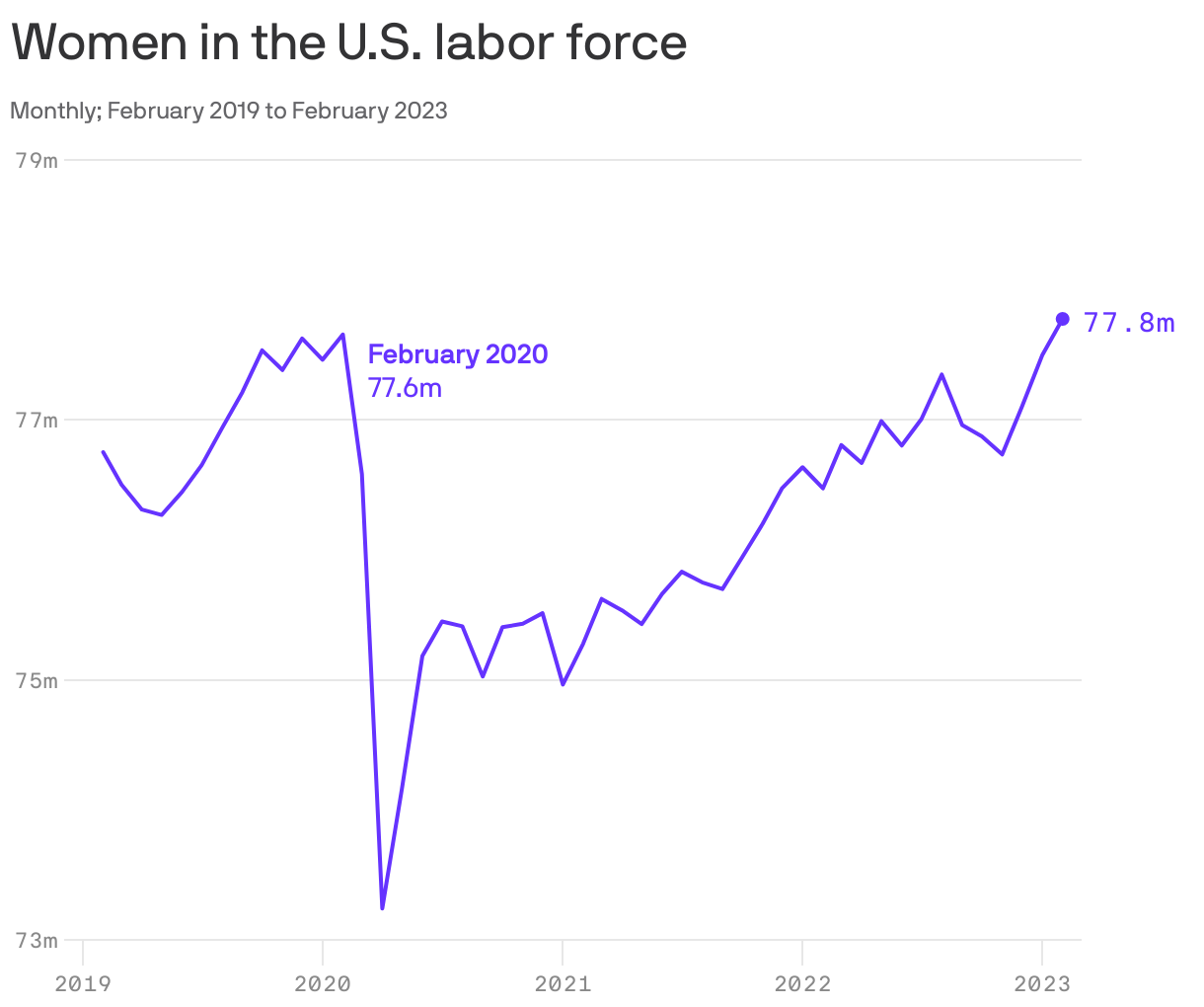

5. It was Jobs Day

With all that bank failure in the air, you didn’t think we’d forgotten that Friday was Jobs Day, did you?

- Here’s one stat from the February report worth highlighting: The number of women in the workforce in February was higher than pre-pandemic levels for the first time, Emily writes.

Why it matters: The strength of women's return to work was faster than anyone could've imagined just a few years ago when dire predictions about a "she-cession" flooded the news.

By the numbers: 105,000 of the 311,000 jobs added in February were in the leisure and hospitality sector, where women hold the majority of positions.

- Overall, women's labor force participation — that is, the percentage of women working or looking for work — is at 57.2%, almost back to the February 2020 number, 57.9%.

- Men's labor force participation rate is much higher than women's, at 68%, but still down more than a point from pre-pandemic levels.

- Read more from our Axios Macro colleagues about why Friday's report was a crowd-pleaser.

Go deeper: College-educated women did not leave labor force during pandemic

Axios Markets

Stay on top of the latest market trends and economic insights