Axios Macro

April 02, 2026

1 big thing: A year of huge tariffs — and more coming

Trump's go-to tariff tool has been clipped in the year since "Liberation Day."

- But the last 24 hours suggest that the administration will continue to lean on tariffs to force economic changes.

Why it matters: The world is still reckoning with the fallout of a trade policy that has since been diluted, just as an energy shock tied to the Iran war creates new economic challenges.

Driving the news: Trump is reportedly planning tariffs as high as 100% on pharmaceutical companies that haven't cut deals promising lower drug prices.

- The White House may also restructure steel and aluminum tariffs in ways that raise import costs, the Wall Street Journal reported last night.

- Trump's trade officials promise to recreate tariffs scrapped by the Supreme Court with a patchwork of other authorities before the current import taxes expire in July.

The big picture: In the year since "Liberation Day," Trump's tariff wall has been torn down by the Supreme Court, watered down by exemptions and scaled back under trade agreements.

- The Supreme Court ruling "certainly has put limitations on the degree of flexibility that Trump has," Wilbur Ross, former Commerce secretary during Trump's first term, tells Axios.

- "The other trade authorities don't lead themselves very readily to going up, down, up, down in short intervals."

- "They are more of a blunt weapon" that limits Trump's ability to make tariffs fluctuate, though that's not necessarily a bad thing, Ross added. "Businesses can adjust to bad news. It's hard for businesses to adjust to uncertainty."

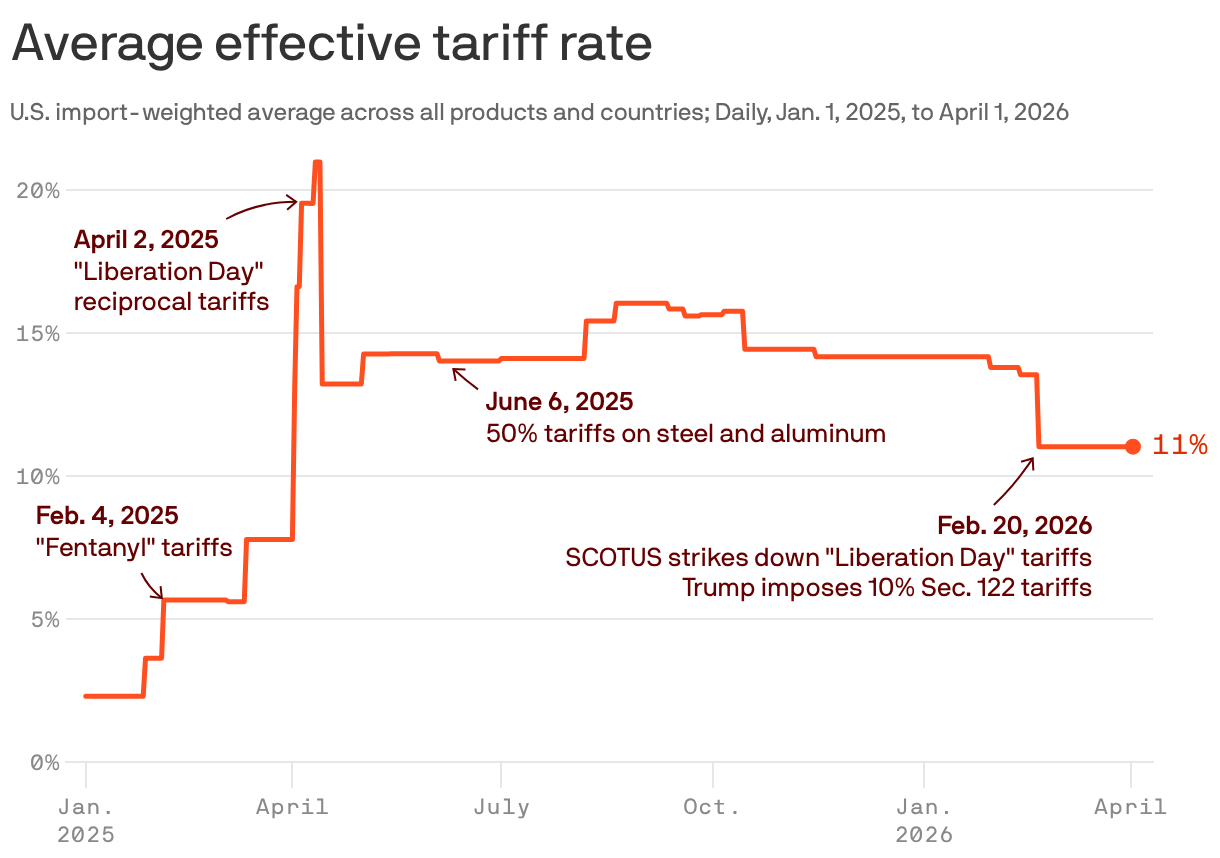

Zoom in: The Trump administration has enacted more than 50 trade policy changes, a historic whipsaw illustrated by a new daily tariff tracker launched by the Budget Lab at Yale. (The necessity for a "daily" tariff tracker says plenty about our times.)

- The effective tariff rate started in 2025 at around 2%. It spiked to the highest in a century after Trump took office, peaking at 21% following "Liberation Day." It now sits at 11%.

Between the lines: Surveys and data suggest U.S. manufacturers have been saddled with higher input prices and that consumer goods prices have risen at a swifter pace.

- It's far from the inflation bomb that economists feared, partly because many threatened tariffs didn't stick or never materialized.

- The White House is encouraged by manufacturing industry surveys, which show activity expanded for a third consecutive month in March after years of contraction. Still, the Institute for Supply Management's prices index is at its highest since 2022.

- Manufacturing employment has decreased in all but one of the 10 months of employment data since "Liberation Day," losing a net 89,000 jobs.

The bottom line: The past year of Trump-era trade policy turned the global trading system upside down in ways that appear irreversible.

- "I worry that we are understating some of the economic impact of the volatility component because what we're focused on is the level of the rates, not necessarily the ways in which these swings are effectuated," Yale's Natasha Sarin tells Axios.

2. The risk of demand destruction grows

Axios Macro