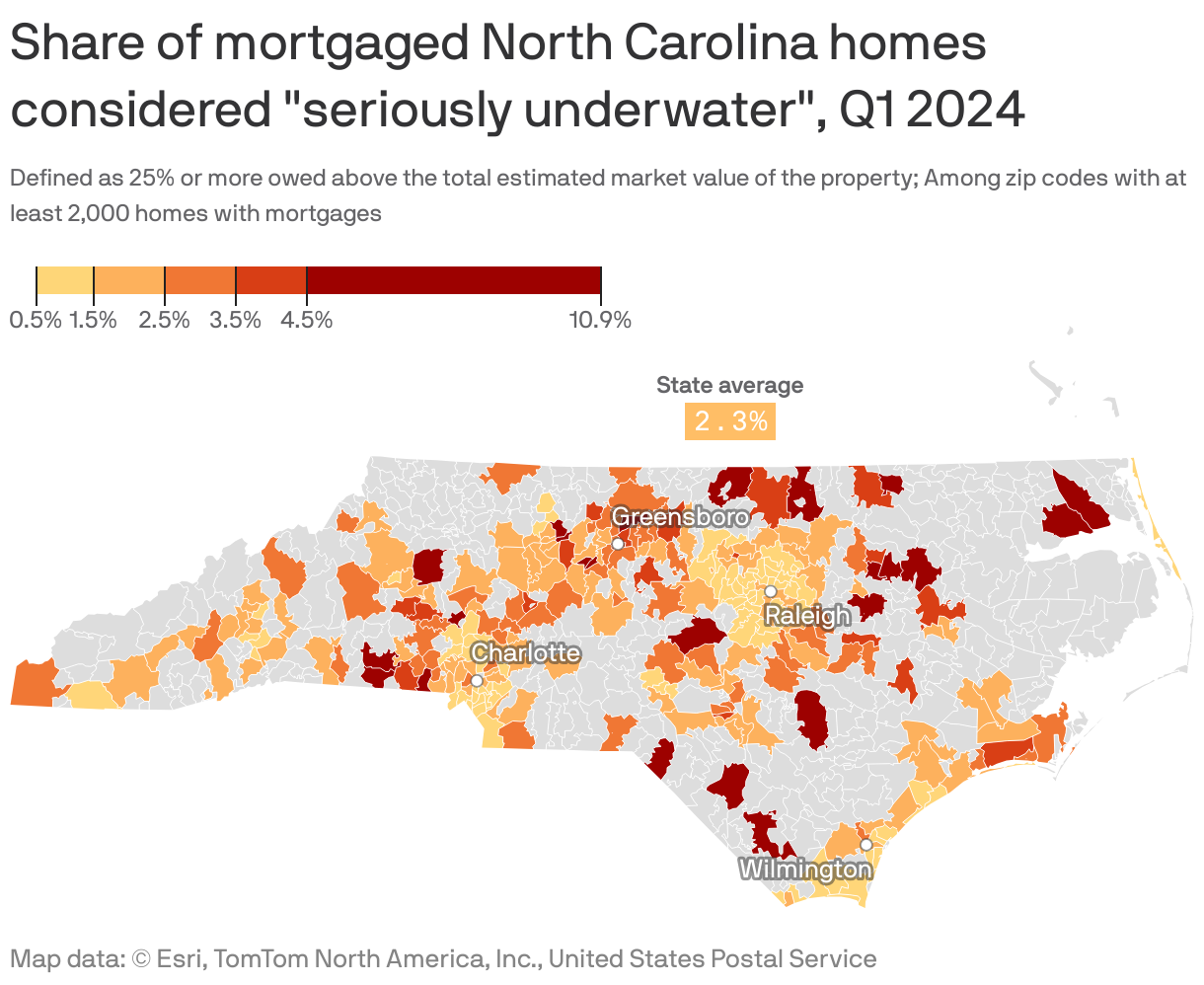

Where N.C. mortgage holders are underwater on their home loans

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netWhile most U.S. homeowners are sitting on a mountain of home equity after years of rising house prices, a number of mortgage holders in pockets of North Carolina are underwater on their loans.

Why it matters: That means these folks owe more on the mortgage than their home is worth, which puts them in a horrendous financial situation if they need to sell their house, Axios' Brianna Crane writes.

Zoom in: Rocky Mount had some of the highest percentages in the state of homeowners with underwater mortgages as of the first quarter of this year, per Attom.

- One ZIP in the eastern part of the town clocked a rate of nearly 11%.

- ZIP codes in Henderson — near the Virginia border — and Lumberton — just south of Fayetteville — had the second and third highest rates, at 9 and 7%, respectively.

Open embedded content from datawrapper.dwcdn.net

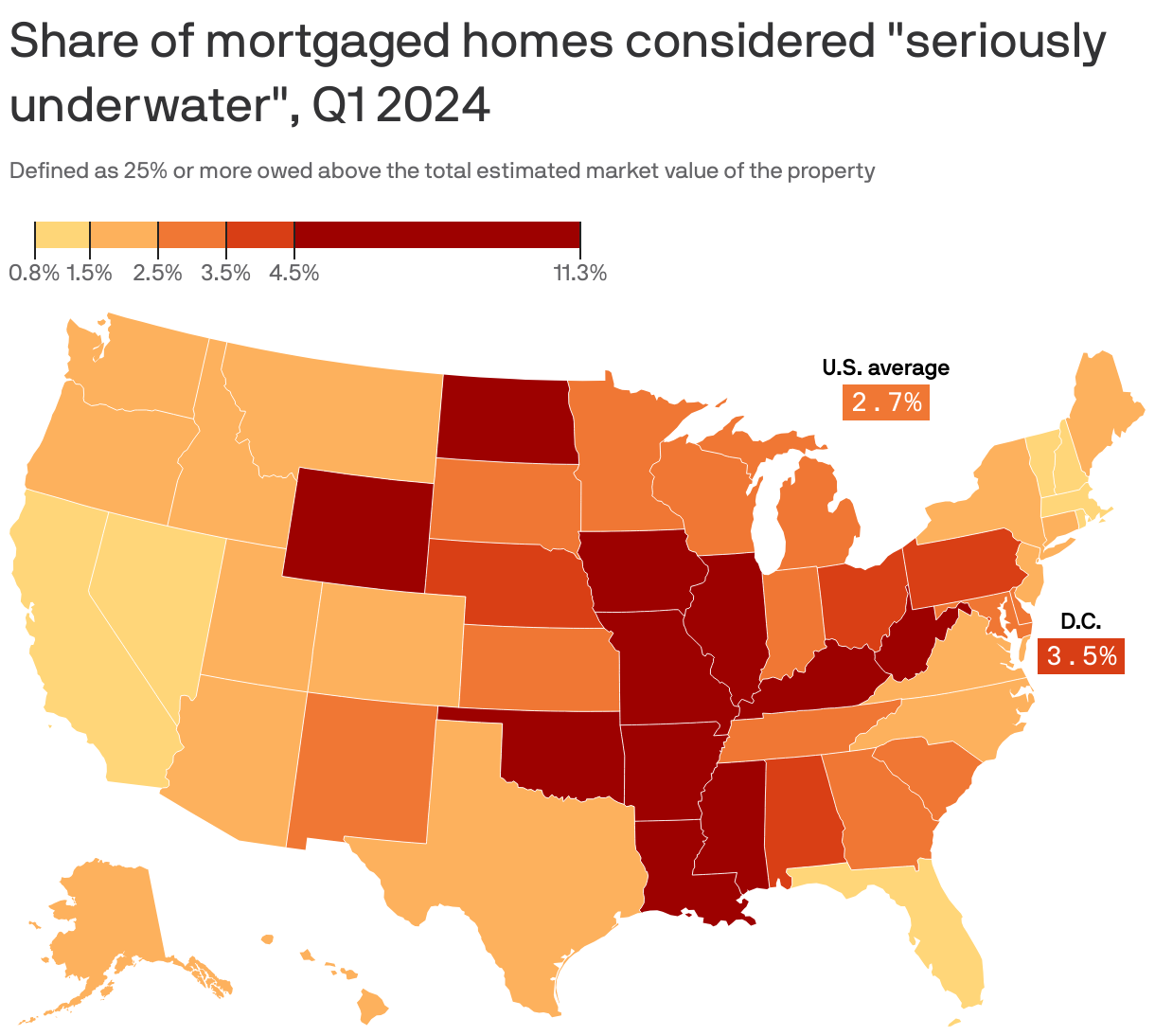

Open embedded content from datawrapper.dwcdn.netYes, but: While the South has some of the highest shares of underwater mortgages, North Carolina is an outlier in the region: just 2.3% of homeowners statewide are upside down on their mortgages.

- Many of the beach and mountain towns of North Carolina have some of the highest rates of equity-rich homeowners: Oak Island, Emerald Isle and Nags Head have the most, with rates all above 67%.

Reality check: After the housing crisis of 2008 one in four homes with mortgages were underwater.

- Unemployment was high in that recession and many people who couldn't pay back their loans by selling their house were forced into foreclosure or short sales.

- Right now, unemployment in the U.S. is low — and the economy is strong.

The bottom line: If the labor market or economy takes a turn, underwater homeowners are more at risk.

- With today's high mortgage rates, the most financially secure people are buying in cash, Redfin chief economist Daryl Fairweather says.

- Recent buyers who took out a mortgage likely have less cash to fall back on.