Low credit scores bring big home insurance cost jumps to Arizonans

Add Axios as your preferred source to

see more of our stories on Google.

Arizonans with low credit scores will pay a greater percentage-based penalty on their home insurance than people in almost any other state, a new analysis finds.

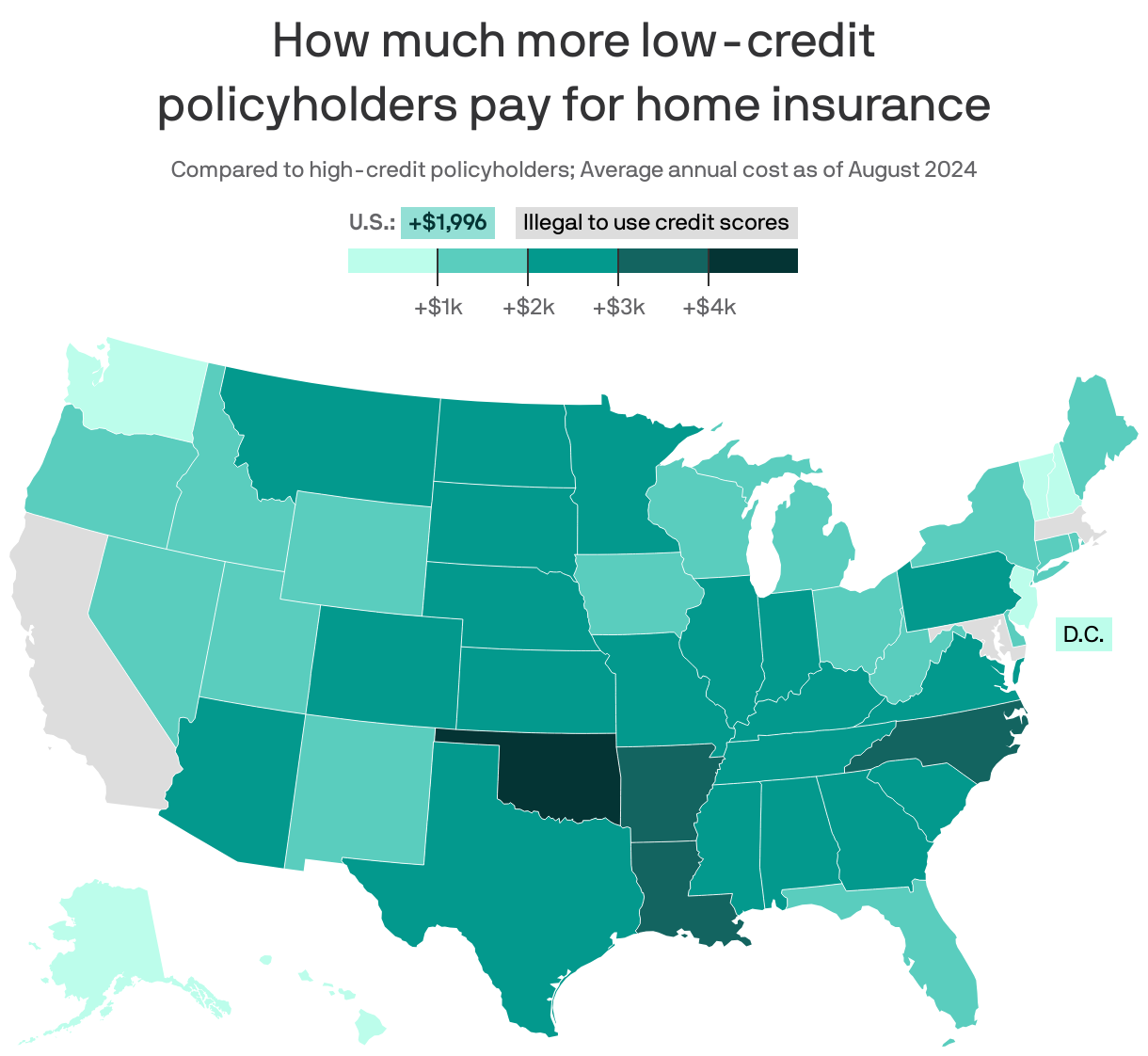

The big picture: People with low credit scores can expect to pay nearly $2,000 more annually on average for home insurance compared to those with high scores.

Why it matters: Credit scores aren't necessarily indicative of somebody's ability to pay their bills — and tying them to insurance prices can disadvantage low-income and minority homeowners, among others.

Driving the news: U.S. homeowners with low credit are charged $1,996 more annually compared to otherwise identical homeowners with high credit, per a new report from the Consumer Federation of America and the Climate and Community Institute.

- That's based on over 600,000 nationwide "test quotes" representing "what a typical, hypothetical homeowner would be charged for homeowners' insurance."

- The researchers controlled for variables other than credit score. They defined a "low" score as about 630 on the 300-850 FICO range, and a "high" score as about 820.

By the numbers: In percentage terms, Arizona (168%) has the second-biggest "credit penalty" — the difference between annual premiums for otherwise identical low-credit and high-credit policyholders — in the U.S.

- Only Pennsylvania (181%) was higher.

- 23 states have penalties of 100% or more, where low credit will at least double the cost of your insurance.

Yes, but: In raw dollar terms, Arizona's average penalty isn't nearly as high as other states — with the 17th-highest dollar penalty ($2,125).

- Oklahoma ($4,138), Louisiana ($3,754) and Arkansas ($3,083) have the biggest credit penalties in terms of total dollars.

- Three states — California, Maryland, and Massachusetts — block insurers from using credit scores in pricing home coverage.

Between the lines: Homeowners' actual premiums are based on many factors, including the value, condition and materials of their house, their work and marriage status, and more.

- But credit scores are part of that mix in most of the country, putting many people at a disadvantage.

- Low-income people and people of color tend to have lower credit scores, for example.

- And young people just starting out in life need time to build up their credit history. Student loans can help if they're paid on time — otherwise they can be a crushing weight.