Axios Markets

April 26, 2022

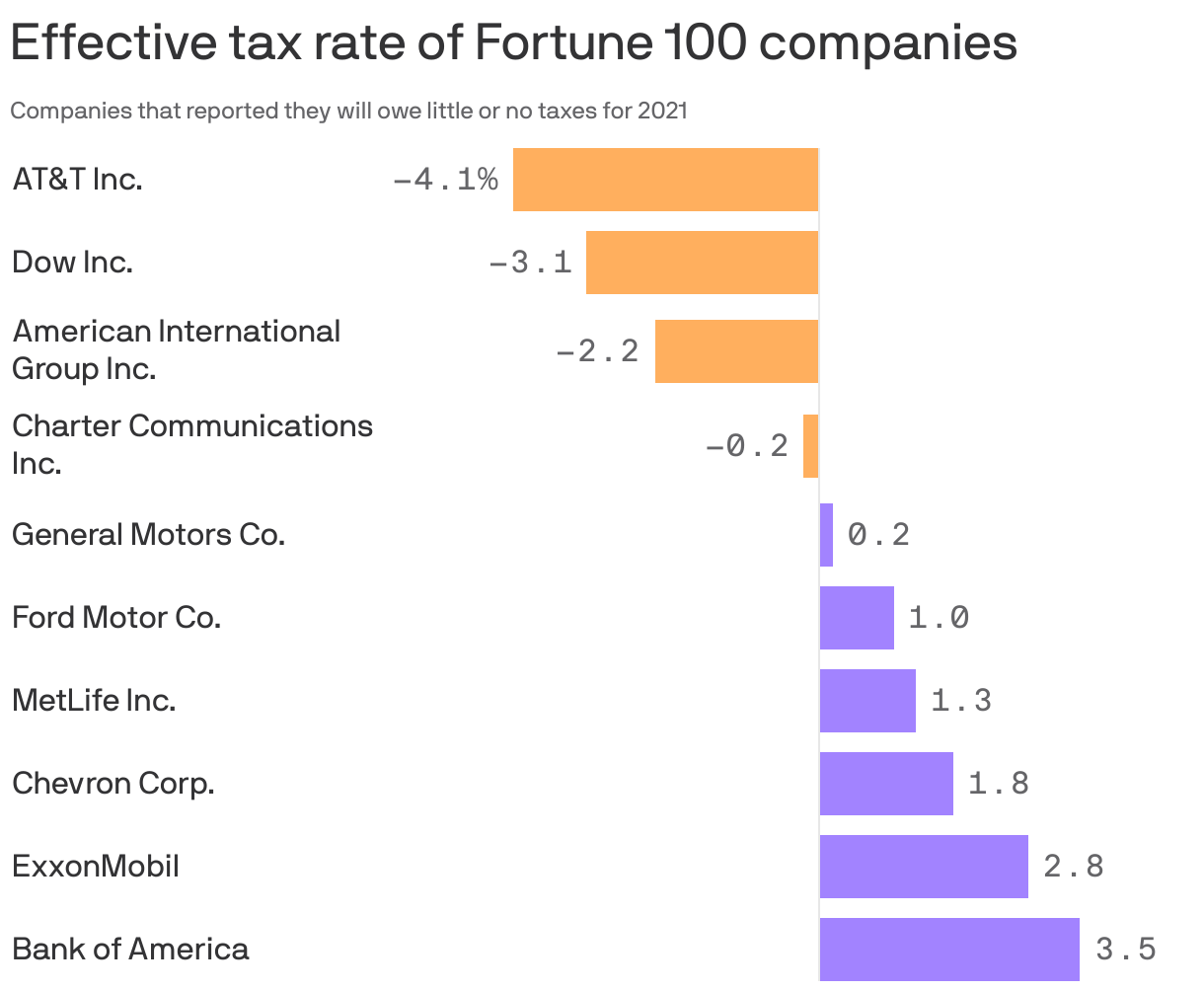

1 big thing: Lowest taxes in the Fortune 100

Nineteen of the biggest companies in the U.S. paid very little in federal income tax last year, according to a new report provided exclusively to Axios by the progressive Center for American Progress, Emily writes.

- Four companies paid less than zero, including AT&T, Charter Communications, American International Group and Dow Inc.

Why it matters: Corporate profits surged to record highs last year, thanks in part to copious amounts of government spending. The idea of companies that earned billions not paying federal tax is sure to fuel calls for reform, but White House proposals to raise corporate taxes have largely gone nowhere.

- "These are huge profitable corporations, and they hardly pay any taxes," said Seth Hanlon, a senior fellow at American Progress who co-authored the report. "It's a glaring sign that something is wrong with the tax system."

The backstory: Companies have been paying lower taxes since the 2017 passage of President Trump’s signature Tax Cuts and Jobs Act, which cut the official rate to 21% from 35%.

- The 19 companies on CAP’s list based on the Fortune 100 all paid an effective rate below 10% — or less than half the official rate.

State of play: Companies don't have to publicly release their income tax filings. This report — and others like it over the years — relies on public companies' annual 10-K filings, where they estimate a “federal income tax expense,” or the money they will pay to Uncle Sam.

- The analysis doesn't include deferred taxes — they haven't actually been paid yet. And it doesn't include foreign taxes.

- Some of the companies on the list argue this methodology distorts the findings.

Flashback: Last year, the Institute on Taxation and Economic Policy found that 55 companies on the Fortune 500 list paid no taxes.

How it works: Companies reduce their tax bill, just like many of us, by taking deductions. Some popular ones, according to Matthew Gardner, a senior fellow at ITEP...

- Tax breaks for capital investments: The 2017 tax law increased the amount a company can write off when it spends money on corporate infrastructure, or the tangible stuff it needs to conduct its business.

- Research and development: This is a big one in the tech sector, Gardner says. Along with capital investments, this is the type of spending that companies would do regardless of tax implications, in order to survive.

- Stock options: Companies can write off the market value of stock options that employees exercise.

What they're saying: Axios reached out to all 19 companies on the list and most that responded said they pay what they're supposed to pay.

2. Catch up quick

3. Muskapalooza: Twitter takes, in brief

Photo illustration: Sarah Grillo/Axios. Photo: Liesa Johannssen-Koppitz/Bloomberg via Getty Images

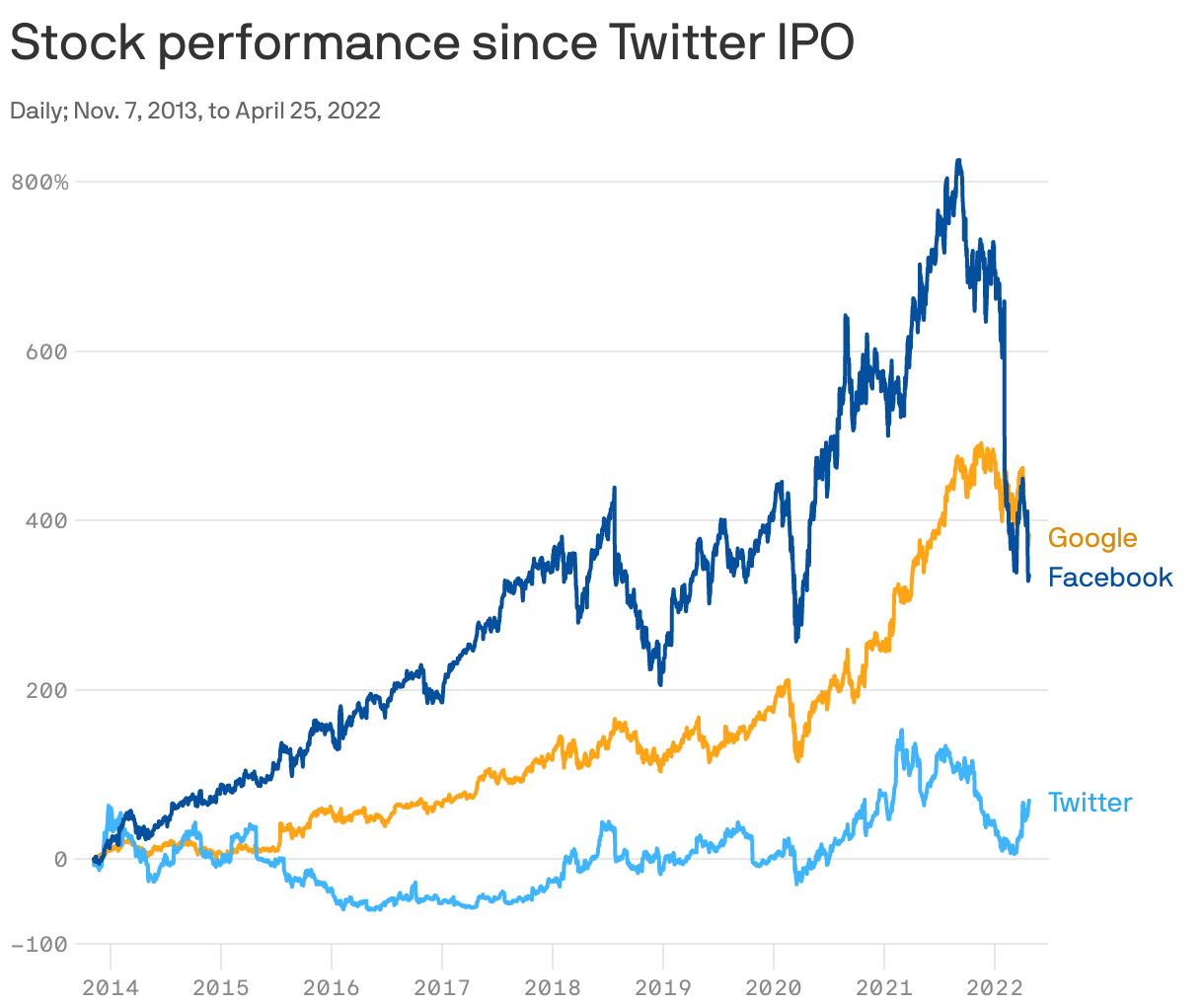

4. Twitter's public company woes

Twitter stock has basically gone sideways since it opened at $45 per share in November 2013, Axios' Felix Salmon writes.

Why it matters: If shareholders had any realistic hope that the share price might be able to follow the trajectory of other social networking companies like Facebook or ByteDance or Snap, they would never have accepted Elon Musk's offer.

The big picture: Twitter's board was duty-bound to care about financial performance and share price first and foremost. Musk has other priorities — which is just as well, given Twitter's historical inability to make profits commensurate with its cultural reach and power.

5. Hedge fund-ing is hard

Illustration: Aïda Amer/Axios

Axios Markets

Stay on top of the latest market trends and economic insights