Axios Markets

January 31, 2024

1 big thing: The retail apocalypse never happened

A good retail space is getting harder to find with the vacancy rate for shopping centers nationwide at a 15-year low, Emily writes.

Why it matters: The COVID-era doomsday predictions were wrong.

What they're saying: We haven't seen the apocalypse everyone was expecting, Thomas LaSalvia, head of commercial real estate economics at Moody's Analytics, tells Axios.

- Retail commercial real estate is "back for good," per a recent report from Cushman & Wakefield, a real estate services firm.

By the numbers: The vacancy rate at U.S. shopping centers — essentially any retail spaces outside the mall — fell to its lowest level since Cushman began tracking in 2007.

- Average asking rents in the sector were 4.1% higher in Q4 compared with a year earlier. They're up 17% cumulatively from 2019, and 41% over the past decade, per Cushman.

Zoom out: Demand for retail space stayed strong overall in 2023 thanks to a growing economy and strong labor market that kept Americans shopping. Retail sales were up 3.2% in 2023 from the previous year.

The big picture: The retail landscape is always evolving to adjust to changing tastes, spending habits and trends — from Main Street to shopping malls to big box and back again.

- The sector ran a gauntlet of store closures and bankruptcies as it faced web competition — and then COVID hit, leading to worries it would never recover.

- At the time landlords offered big concessions to some retail tenants to keep storefronts filled. Those deals are largely gone.

- That's meant depressed levels of retail construction for the past decade. "Lack of new retail construction has kept a ceiling on the vacancy rate since the start of the pandemic," per the Cushman report.

Context: Last year just 8 million square feet of new retail space was constructed — that's compared to about 20 million in 2019.

- Even those numbers are small compared to a decade ago. From 2008-2014, new construction averaged nearly 40.8 million square feet per year, per Cushman.

What's emerged is a more resilient landscape. These days e-commerce and physical retail now complement each other. Opening a brick-and-mortar store can even increase a brand's online sales, according to a study from late last year. Closing a store has the opposite effect.

Meanwhile: Shopping centers became more diverse — there are medical offices, gyms, day care centers, and pickleball.

Between the lines: Retail's evolution may hold lessons for what's happening in the office market, which is struggling to adapt to a remote-friendly work world.

- Landlords might need to get flexible with all those empty offices, some of them might go away entirely or get converted to residential buildings or transform into a new mixed-use situation.

- It took more than a decade for retail to adapt to a new era, it's reasonable to assume the office market will need a similar amount of time.

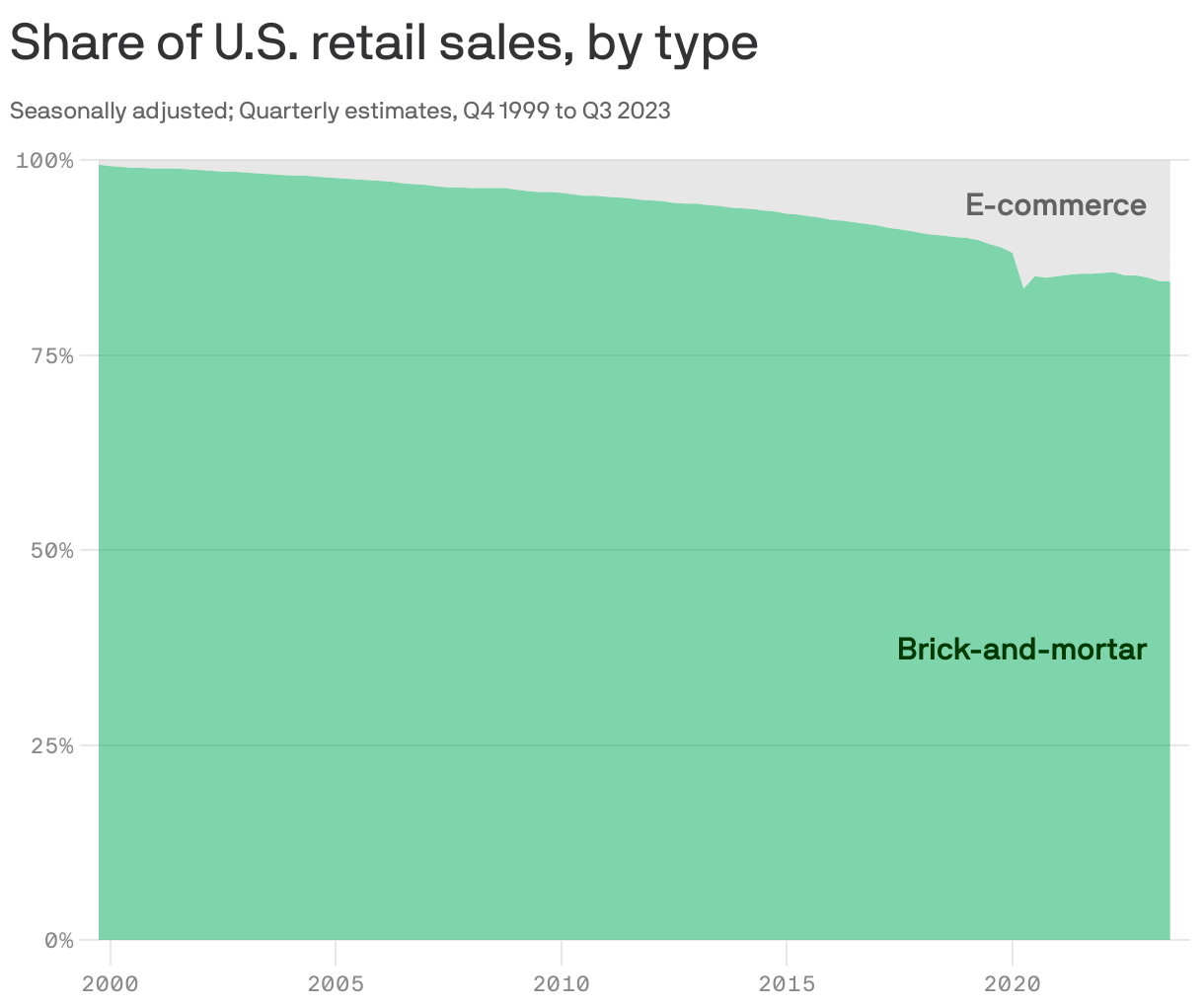

2. Charted: How we buy things

For all the transformation brought by the web, online shopping still only represents about 16% of overall retail sales.

Why it matters: Americans' love of shopping is one more simple reason for brick-and-mortar retail's staying power.

- "We are social beings, we enjoy being out and one of the things we like to do when we're out is to shop," says Moody's LaSalvia.

- That's why the whole notion of a retail apocalypse "never made sense in the first place."

3. Catch up quick

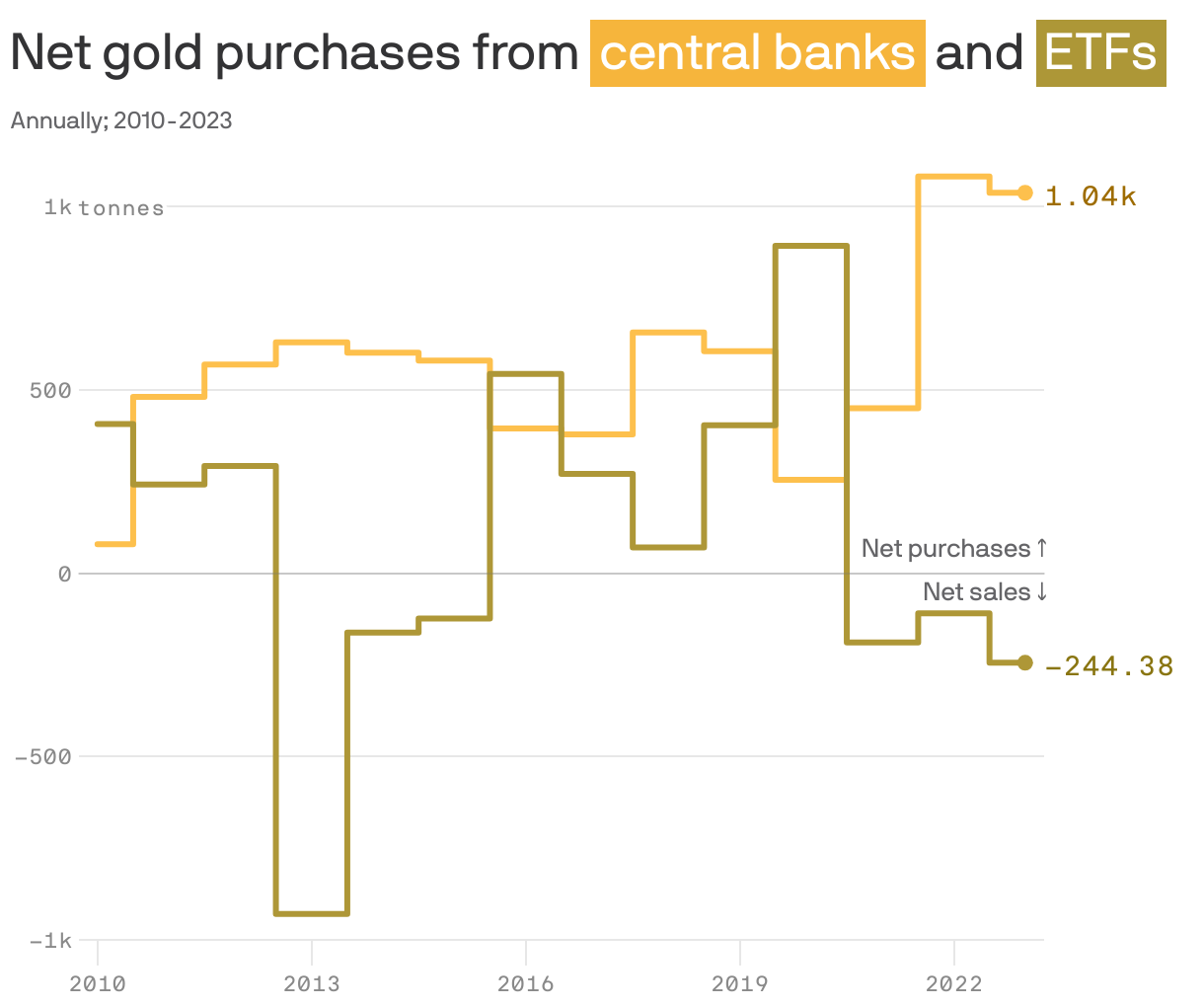

4. Who's buying the gold

Bitcoin bulls want to know: If you can easily buy a commodity on the stock market, in ETF form, does that drive demand for the commodity itself?

- The answer, judging by the past three years in the world of gold ETFs, is a clear no, Axios' Felix Salmon writes.

Why it matters: The run-up in the price of gold over the past few years has not been driven by individual or corporate investors buying up ETFs. In fact, ETFs have been selling gold.

- The world's central banks, by contrast, have been buying at a record pace, according to a World Gold Council report released Wednesday morning.

The big picture: Private-sector investors generally buy gold out of fear more than greed — and the amount of gold they bought in 2023 hit a ten-year low. That bespeaks a broader post-pandemic risk-on attitude.

Between the lines: Insofar as investors are buying gold, they're buying it in the form of bars and coins — not in the form of ETFs, which have been net sellers of gold for three years running.

- Even gold-bar purchases, however, are falling, sometimes dramatically. In Germany, for instance, demand for physical gold slumped by some 75% between 2022 and 2023, according to the WGC.

The other side: Central banks collectively bought more than 1,000 tonnes of gold for each of the past two years — a pace unprecedented in modern history.

- The People's Bank of China alone bought 225 tonnes of gold in 2023, worth some $15 billion at current prices. Its current holdings now stand at 2,235 tonnes and represent about 4% of its international reserves.

- The National Bank of Poland bought 130 tonnes of gold, making the metal 12% of its total international reserves. Its president, Adam Glapiński, has said he would like to see that number reach 20%.

💭 Felix's thought bubble: In a world where U.S. hegemony can no longer be assured, it makes sense for central banks to diversify away from the dollar, which has historically made up the bulk of their reserves. Gold is a natural beneficiary of that move.

The bottom line: Central banks seem much more keen on positioning themselves for a potential future crisis than private-sector investors are.

5. 🗣 Quoted: No margin pride here

Axios Markets

Stay on top of the latest market trends and economic insights