Axios Markets

January 08, 2024

1 big thing: Peaking beneath the surface

Illustration: Annelise Capossela/Axios

2. Catch up quick

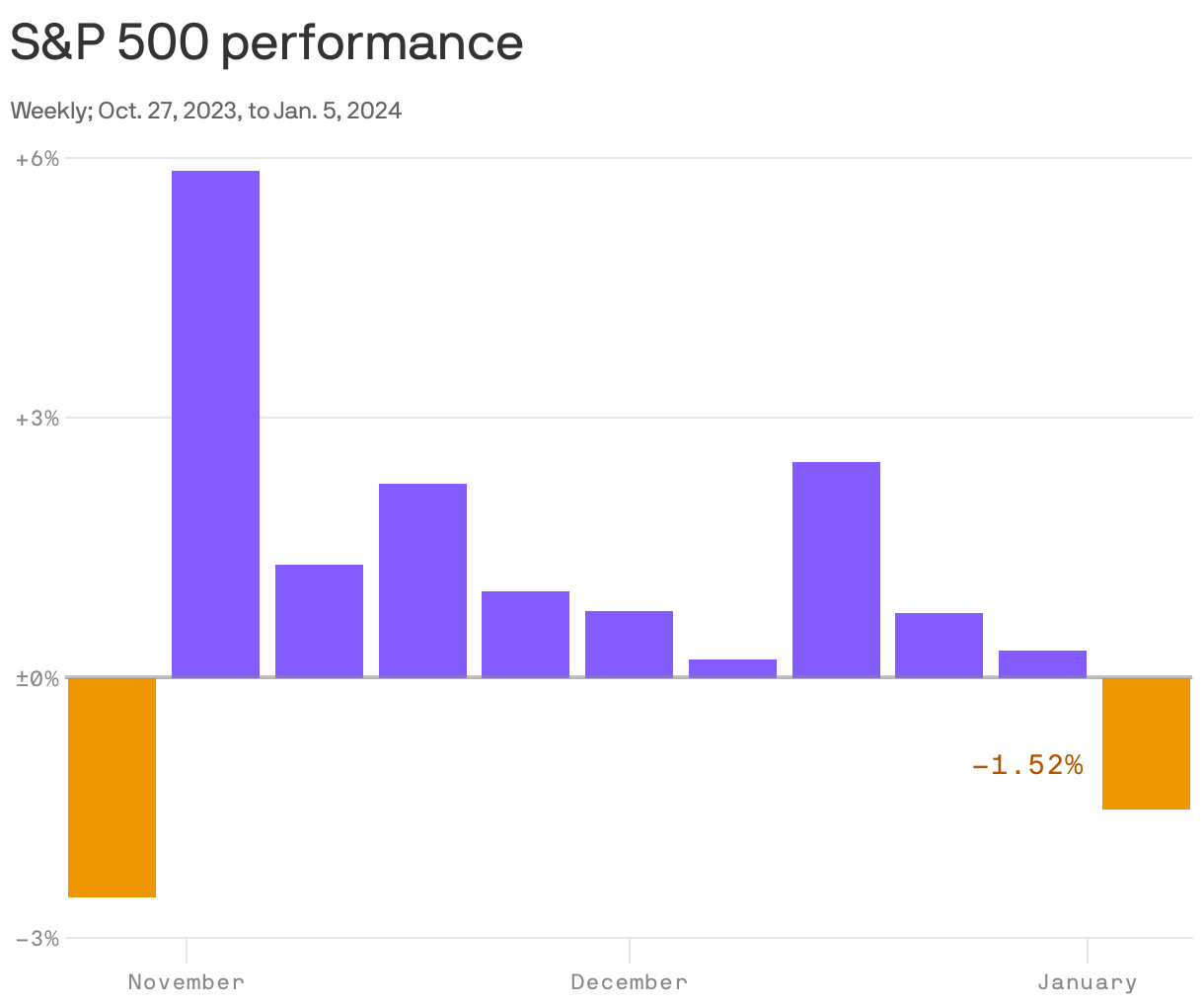

3. Market's streak of weekly gains ends at nine

The S&P 500 snapped its string of consecutive weekly gains last week, Matt writes.

Why it matters: The streak of nine straight weekly gains lifted the stock market index as much as 16% at points.

- It was the longest weekly winning streak since January 2004.

State of play: A bit of a retreat from the sharp rally at the end of last year, as well as concern about higher oil prices and potential trade disruptions related to violence in the Middle East all helped take the spring out of investors' step in the first week of 2024.

What to watch: Coming up this week, the latest report on U.S. consumer price inflation, due Thursday, will likely be the market's main event.

4. Pay is beating inflation again

Americans are now getting an actual pay raise, even after accounting for inflation, Matt writes.

Why it matters: Rising real — that is, inflation-adjusted — earnings are a basic indication of improving standards of living.

Driving the news: Average hourly earnings of private sector employees rose at an annual rate of 4.1% in December, according to Friday's job report, a smidge higher than the 4% gain in November, and roughly 1 percentage point above the 3.1% annual rise inflation that month.

- December CPI data is due Thursday morning.

Yes, but: Don't expect spontaneous parades. From April 2021 to June 2023 — more than two years — inflation was significantly higher than earnings, meaning that workers' standards of living fell sharply.

The bottom line: It'll likely take a long stretch of real wage gains before Americans feel better after that inflationary pinch.

Read more: The majority of workers are making more money now than they were a year ago

5. Child care jobs recovery still lags

The number of employees in child care services crept up by a few thousand to 1.023 million in December — but employment in the sector still isn't back to where it was in February 2020, according to data out Friday, Emily writes.

Why it matters: It's somewhat surprising because there is a record share of parents — mothers, more specifically — in the job market. And their kids need child care.

- In a typical market, an increase in demand from more parents needing care would lead to an increase in supply.

- But child care isn't a typical industry — operators run on razor-thin margins and they're fairly constrained in what they can charge working parents.

Zoom out: Hiring's been slow, partly because this is a low-pay industry and there are better, higher-paying jobs out there.

- Plus, pandemic-era child care funding has run out, leaving many centers scrambling.

The intrigue: Remote work may have been the saving grace here; enabling some parents to manage child care in a more ad hoc way.

Axios Markets

Stay on top of the latest market trends and economic insights