Axios Crypto

September 09, 2025

Good morning from DC! All the reporters from Axios are in the nation's capital meeting up right now.

- Meanwhile, Congress is meeting up about digital assets legislation.

Today's newsletter is 1,220 words, a 4-minute read.

1 big thing: New market structure draft

The Republican senators focused on getting legislation passed to regulate the trading of crypto assets circulated a new discussion draft on Friday night.

- This morning, Democrats put out their own framework for such legislation.

Why it matters: Lawmakers seem to have come to a rough consensus that it's time to pass market structure legislation, the second major crypto bill after the stablecoin one.

The big picture: The question in the cryptocurrency world has been what do members of the industry need to do to create tokens that can be traded in a compliant manner in the United States?

Between the lines: The U.S. uses a disclosure-based regime, and so the real question what do token issuers need to disclose? The Senate discussion draft goes into more detail on that. The kinds of information the bill contemplates seeking disclosure of includes:

- Basic corporate information about the company creating the asset, as well as the experience and asset holdings of relevant leaders.

- The recent activities the issuer has undertaken, its plans for the next year, and information on its budgets, including assets and liabilities.

- The distribution and plans to distribute the token, or what's usually referred to as tokenomics.

In the weeds: The legislation also describes how an issuer can certify that its network has become decentralized, in other words, control over the future of the network has been distributed enough that the original issuer is no longer substantially in charge.

State of play: The first discussion draft on the Senate bill circulated in July ran to only 35 pages. This new version — which Axios obtained but hasn't yet been put out — runs to 182 pages and leaves much less to the discretion of regulators.

- That moves it closer to the spirit of the House version of the bill passed in July. While 78 Democrats in the House voted "yes" to that bill, it was always known that the legislation faced a tougher road in the Senate.

💭 My thought bubble: The 12 Democrats who backed the new framework didn't make it easy to spot where the daylight is between their policy stance and the Republicans.

- Largely, it just seems to say: We should finally regulate this market.

- But that might have been the point. Members of the minority party might finally be forming a message of their own.

What we're watching: If the Senate can get some kind of legislation through this year.

- The Banking Committee reportedly wants to get a markup done this month.

What's next: We expect Senate Ag to also put out its own discussion draft.

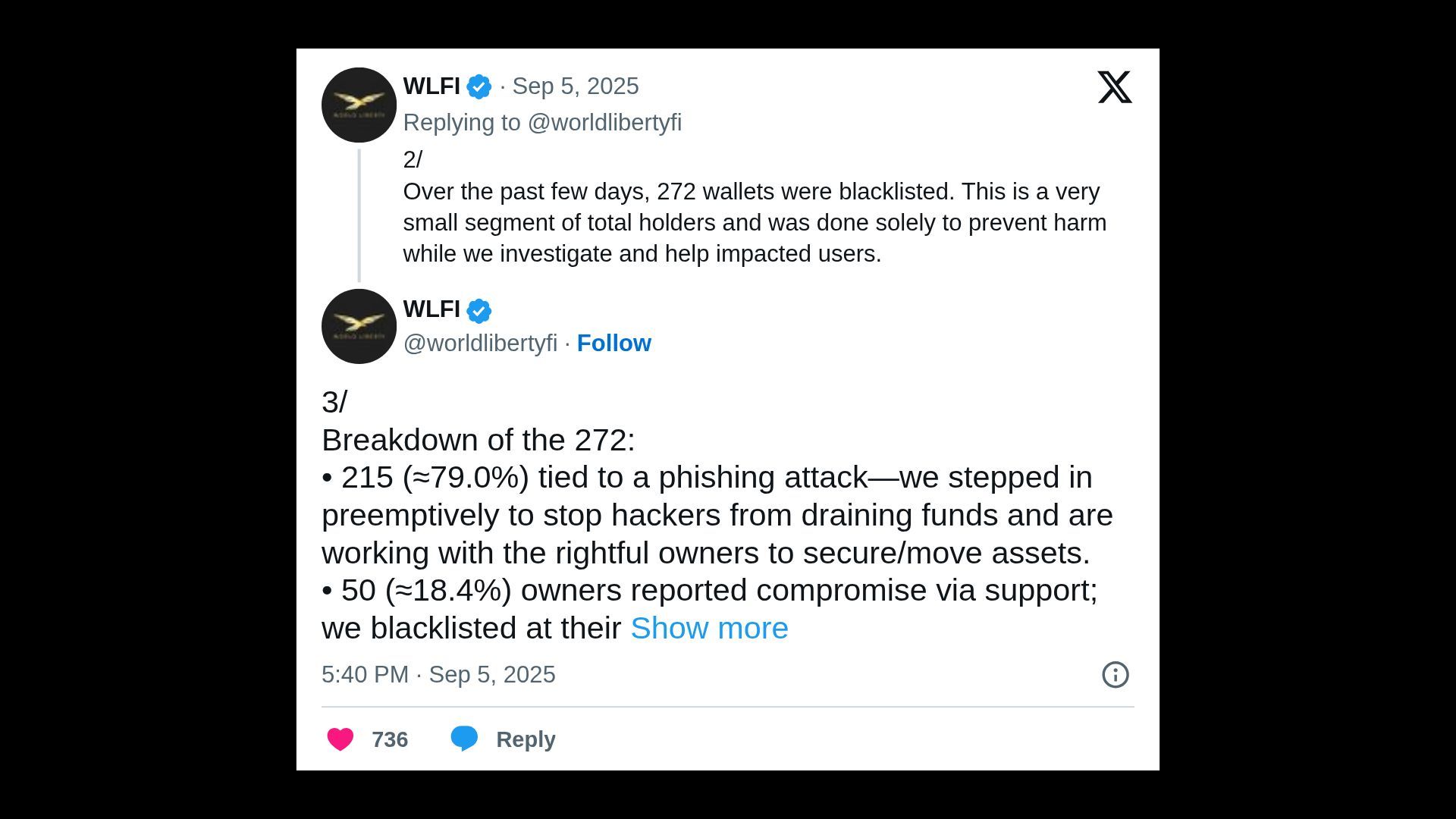

2. World Liberty's explanation

Crypto billionaire Justin Sun, a major investor in the Trump family's World Liberty Financial, announced last week that his tokens had been frozen when trading in them became available.

The latest: On Friday night, World Liberty addressed why 272 wallets had been blacklisted in a thread on social media.

- The reasons ranged from compromised wallets, phishing attacks and high-risk users.

Follow the money: Like many freshly released tokens, WLFI's value climbed quickly when it began trading on public exchanges last Monday, and then fell rapidly.

- This isn't unusual as early investors release lots of supply onto the market at once.

The intrigue: The company noted that the blacklist function had been applied to 272 wallets, but they only offer explanations for 271.

- Analysis by on-chain analytics intelligence firm Nansen confirmed Sun's wallet was blocked with World Liberty Financial's blacklist function.

- It held 544 million WLFI tokens ($122.4 million) on Sept. 4.

- According to Nansen, the other wallets impacted had much, much smaller balances than that of Sun's. The median balance of the other top 20 wallets was $17,981 in WLFI.

The latest: The token is down 27% since trading was enabled.

3. Gemini founders all in on GOP

There's a new megadonor force in Republican politics: the crypto-mogul Winklevoss twins, founders of the Gemini crypto exchange.

Why it matters: Cameron and Tyler Winklevoss, 44, are part of a rising group of millennial and Gen X crypto and tech billionaires bolstering the president, and they could dominate the GOP donor world for decades to come.

- "Who are the donors going to be for the next 20 to 30 years? I put them firmly in that group," said Republican contributor Omeed Malik, a business partner of Donald Trump Jr.'s at 1789 Capital and friend of Winklevosses.

State of play: The Winklevosses began donating to Republican causes in 2017, but their giving has exploded this year. According to a person familiar with the latest totals, they've shelled out more than $32 million to date.

- Much of that — $21 million — has gone to the Digital Freedom Fund, a newly launched super PAC that aims to boost pro-Trump and pro-crypto candidates in the 2026 midterms, Tyler Winklevoss told Axios.

- The PAC hasn't announced which candidates it supports but appears to have an early target to oppose: former Sen. Sherrod Brown (D-Ohio), a crypto skeptic trying to return to the chamber after losing his seat in the 2024 elections in a race where he was opposed by the crypto industry.

What they're saying: "I think it's really important for the Republican Party to maintain control of Congress, if we are going to usher in and realize President Trump's vision to make America the crypto capital of the world," said Tyler Winklevoss.

What's next: The twins — like other crypto and tech donors such as Elon Musk, David Sacks and Peter Thiel — will be courted aggressively by Republicans seeking national office in the future.

- "This alliance of MAGA and tech, that's the future, and (the Winklevosses are) very much a part of that," Malik said.

4. Catch up quick

5. Flashback: Lost texts from SBF days

Back in the midst of the debacle that was the unwinding of the crypto exchange FTX and the eventual conviction of its founder, I used to get messages from people telling me the real story I needed to cover.

- The real story, they said, was the conspiracy between Gary Gensler, then SEC chief, to hand the whole crypto market to Sam Bankman-Fried.

Yes, but: Cool beans, I would tell them, do you have any evidence for this?

- The answer: Well you can see on his public calendar that they had a couple meetings.

- Me: Okaaaaayyyyy...

💭 My thought bubble: Everything Gensler did in his tenure suggested he had it in for the industry. It was always very hard for me to believe that he had any motivation to cut a deal with the whiz kid of Berkeley.

- If anyone had real evidence, I would have pursued it, but no one did. Nor did it pass the sniff test.

The latest: A recent report details how all Gensler's text messages from just before FTX blew up for about a year afterward were accidentally deleted by government technicians, with no hope of recovery.

- That's sure not going to dampen the conspiracy theory.

This newsletter was edited by Pete Gannon and copy edited by Anjelica Tan.

Sign up for Axios Crypto