The yield curve may be wrong when it comes to predicting recession

Add Axios as your preferred source to

see more of our stories on Google.

Analysts and economists on Wall Street are starting to question the predictive power of the inverted yield curve.

Why it matters: It means they're rethinking assumptions that helped drive many to cut forecasts for U.S. economic growth, amplifying the wave of recession talk.

Driving the news: Economists from both Goldman Sachs and JPMorgan published research this week questioning whether the yield curve inversions that have persisted since the middle of last year are really forecasting a recession.

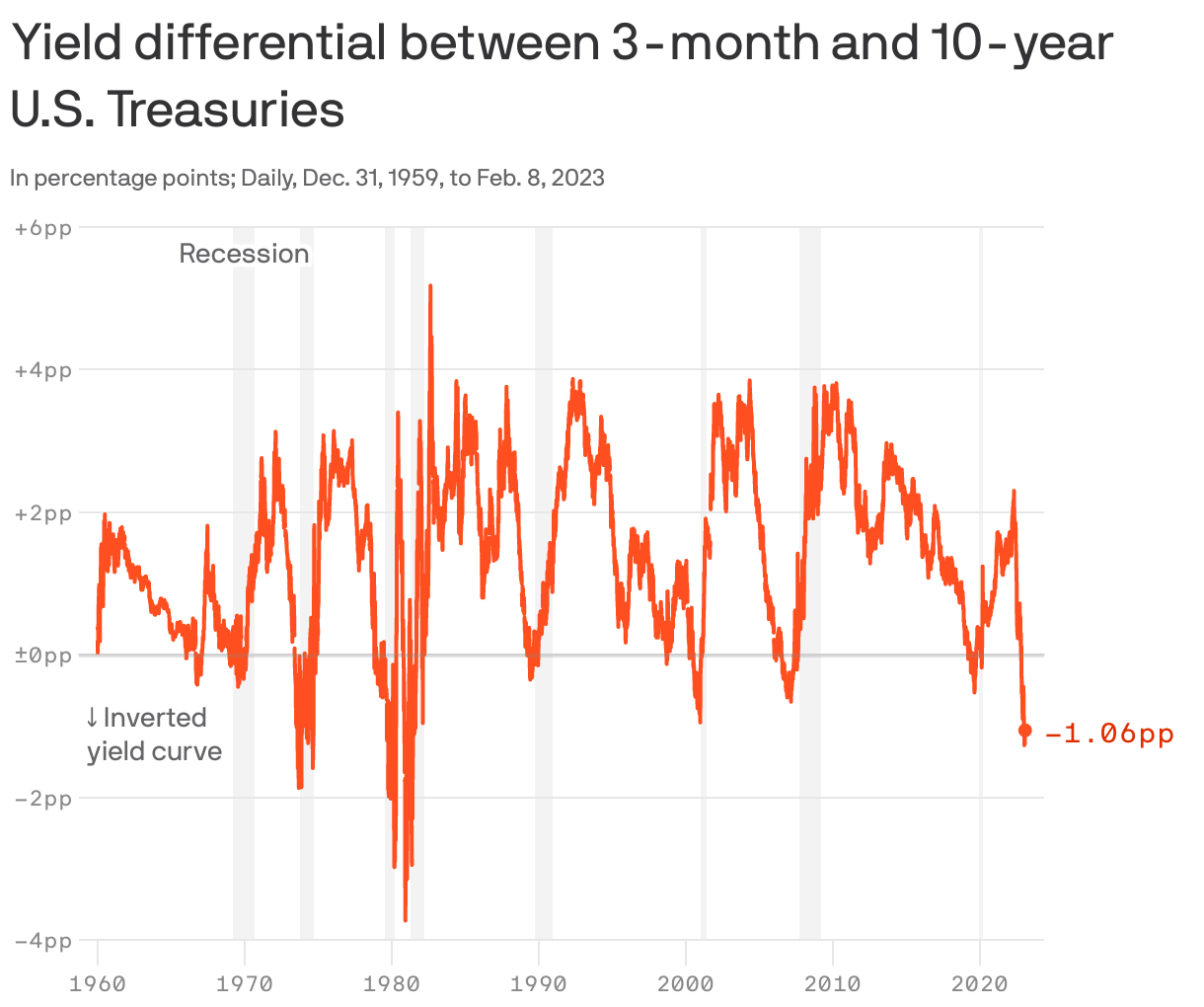

The backstory: An inverted yield curve means yields on long-term U.S. government bonds are below those on short-term bonds. This is abnormal.

- Inverted yield curves are often interpreted to mean investors expect interest rate cuts — something that often happens during recessions.

- What's more, inversions have a strong record of predicting recessions: Over the last 60-odd years, whenever the yield on 10-year Treasury notes fell below those of 3-month Treasury bills, a recession has followed within two years.

Yes, but: Market signals are always subject to interpretation. Long-term bond yields could be lower than short-term yields for a variety of reasons.

What they're saying: In a note published Thursday, JPMorgan analysts suggest that, rather than a recession, yields on longer-term bonds might instead be pricing in a sharp decline in inflation. That would mean the Fed could stop hiking (and maybe even start cutting) interest rates soon-ish.

- "We are respectful that the Treasury yield curve has a successful history of forecasting recessions," they wrote. "So why do we think it is sending a different message this time?"

- The answer: "Rarely (if ever) have markets expected this much disinflation," they went on.

- This is a view that started gaining steam late last year.

Meanwhile, Goldman Sachs' take is a little different. The analysts argue that rather than a swift pullback in inflation, investors are pricing in a return to the secular stagnation of the pre-COVID economy.

- Markets appear to be pricing in a scenario where the Fed cuts interest rates sharply, but over the long term — indicating a return to a low-growth and low-interest rate environment, according to Goldman analysts.

- "A large part of the inversion seen in current US yield curves comes not from high recession odds or inflation normalization, but rather from low long run real rate levels," the analysts wrote in a note published Wednesday. "Investors appear to be wedded to the secular stagnation ... view of the world from the last cycle."

The bottom line: Whatever their rationale for the sudden surge of doubt about the yield curve's predictive power, Wall Street and investors are racing to rethink their previously dour forecasts for growth.

- That's because evidence suggests the U.S. economy is actually pretty strong.