Why the inverted yield curve may not signal a recession this time

Add Axios as your preferred source to

see more of our stories on Google.

An inverted yield curve is normally a bearish signal. Right now, however, it might just be bullish.

Why it matters: It's easy to be scared by the current state of the yield curve. But maybe — just maybe — this time is different.

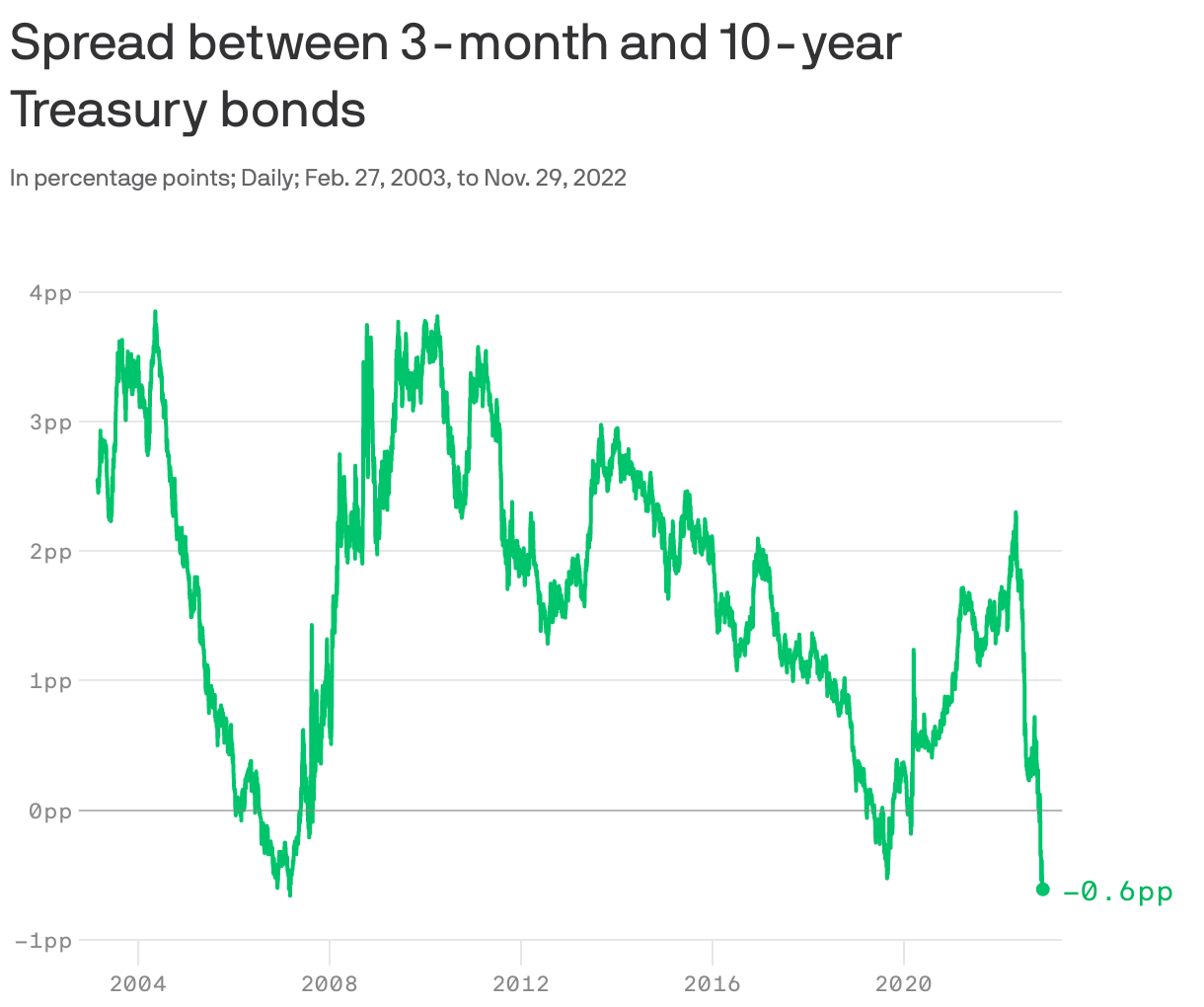

By the numbers: The yield on 10-year Treasury bonds is now an astonishing 0.61 percentage points lower than the yield on 3-month Treasury bills. With the exception of one date in March 2007, that's the most inverted the yield curve has been in over 20 years.

- As Axios explained last month, this particular piece of arcana has a 60-year-strong track record of predicting a recession. (It even seems to have successfully predicted the arrival of COVID-19.)

How it works: The yield curve has historically inverted when investors expect the central bank will be forced to cut rates as a recession-fighting measure.

- Right now, however, 10-year yields have come down for a different reason — markets increasingly believe the Fed is going to win the battle against inflation, and therefore won't need to keep rates high for very long.

- As Sam Goldfarb writes in the WSJ, "the yield curve has become more deeply inverted in recent weeks due largely to good economic news."

Between the lines: It's important to distinguish between nominal rates (what we see in the yield curve) and real rates, which account for inflation, as St. Louis Fed president James Bullard said in an interview on Monday.

- If investors believe that inflation will be a steady 2%, then nominal rates of 4.35% at three months and 3.74% at 10 years work out to real rates of 2.35% and 1.74% respectively — still inverted.

- But let's say you believe inflation will run at a 5% pace over the next three months but only 2% over the next 10 years. Then the real rates are -0.65% at three months and +1.74% at 10 years. In real terms, the yield curve isn't inverted at all.

The bottom line: A recession is still bound to happen eventually. But the yield curve probably isn't being very helpful in pointing analysts to when that will be.