Axios Pro Rata

July 30, 2022

1 big thing: Climate insurance is risky business

Illustration: Shoshana Gordon/Axios

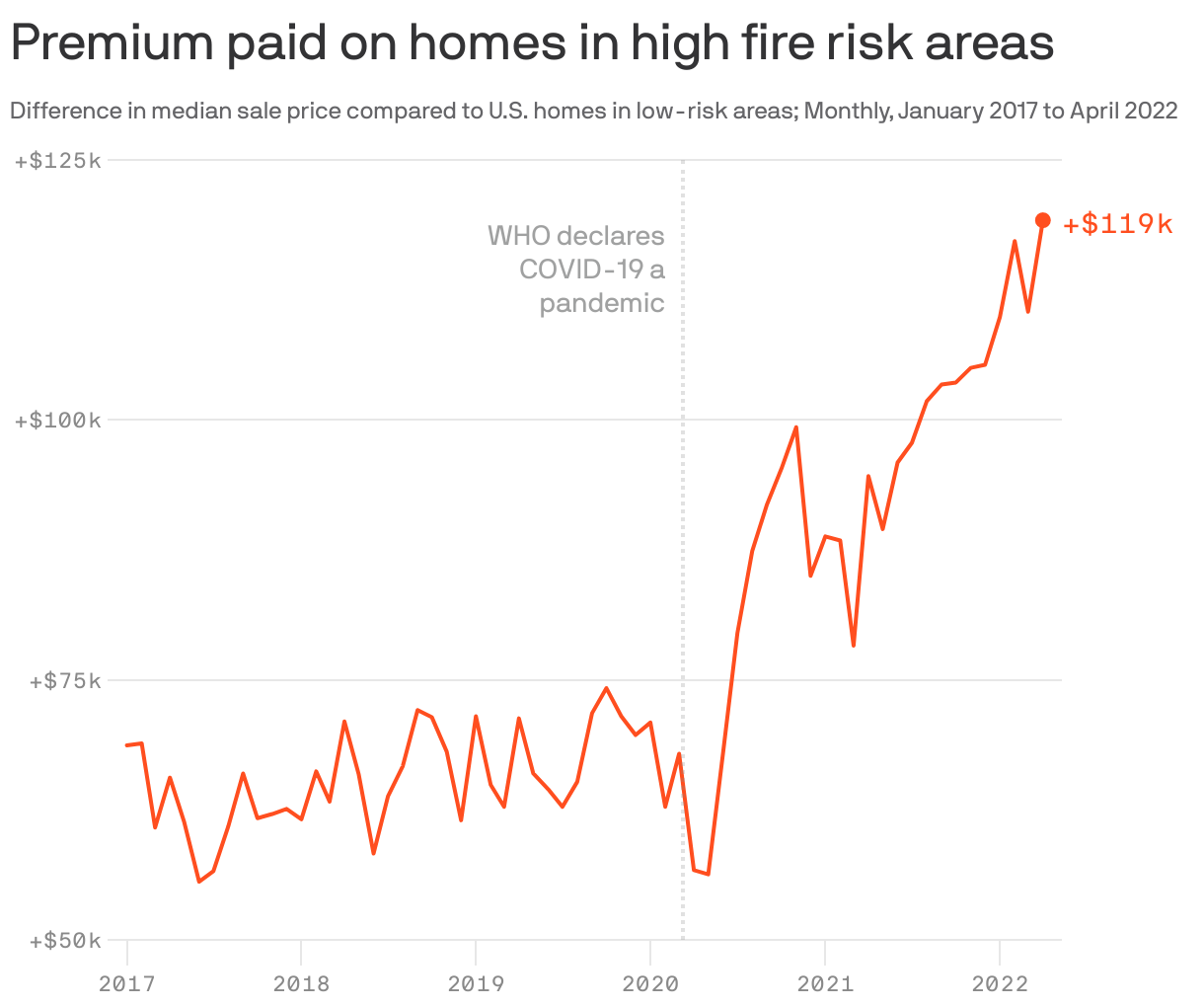

2. Homebuyers add climate risk to checklist

Home shoppers have more information than ever to see how a potential new home will be threatened by wildfires, floods, heat and other climate risks. But research shows that large swaths of homebuyers and renters can't (or don't) act on that data, writes Axios Pro's Alan Neuhauser.

Why it matters: Climate-risk data can empower decision-makers, but it can also exacerbate inequality.

What's happening: Each listing on Redfin and Realtor.com now includes "Climate Risk" scores: a 0-100 gauge of how likely a flood, fire, severe storm, drought or extreme heat will strike the home.

- The data is supplied by First Street Foundation, a nonprofit working to map climate risk.

What they found: Communities of color face a disproportionate risk of flooding and extreme heat.

- Redlined neighborhoods are 5 degrees hotter than non-redlined areas, per a 2020 study that attributed the trend to the urban heat-island effect.

- And when it comes to flooding, 8.4% of homes in redlined areas face high flood risk, compared with 6.9% of homes in non-redlined areas, per Redfin.

Yes, and: Research is underway, but one hypothesis is that climate intelligence could entrench these inequities by further depressing home values in areas that are still marked by the impacts of segregation.

- "People ... can’t get equity to compensate them to move," Redfin chief economist Daryl Fairweather tells Axios.

- A greater number of families who live in formerly redlined areas are renters rather than owners — and renters, at least in theory, have more flexibility to move.

Yes, but: There are also plenty of high-net-worth areas that have seen huge investment despite the climate risks. Miami has boomed despite hurricane and sea level threats, and ski towns like Tahoe, Park City and Aspen have grown in the face of severe fire risk.

- "There may be a 1% risk each year," First Street Foundation CEO Matthew Eby tells Axios. "But when you have cumulative risk of 1% every year over 30 years, you have a 1 in 4 chance of being impacted by that event."

Meanwhile: Then there's the middle-band: Homebuyers forced out by astronomical home prices in certain sections have to accept a suburb in central or northern California that will likely experience a wildfire.

- "People sacrifice on climate risk because it’s abstract, it’s in the future, versus looking at your monthly mortgage payment, which is a lot more tangible," Redfin's Fairweather says.

3. Hurricane season to allow some companies to showcase their tech

Illustration: Brendan Lynch/Axios

📚 Due Diligence

🧩 Trivia

🧮 Final Numbers

Axios Pro Rata

Dan Primack’s briefing on VC, PE & M&A for dealmakers.