Axios Markets

June 21, 2022

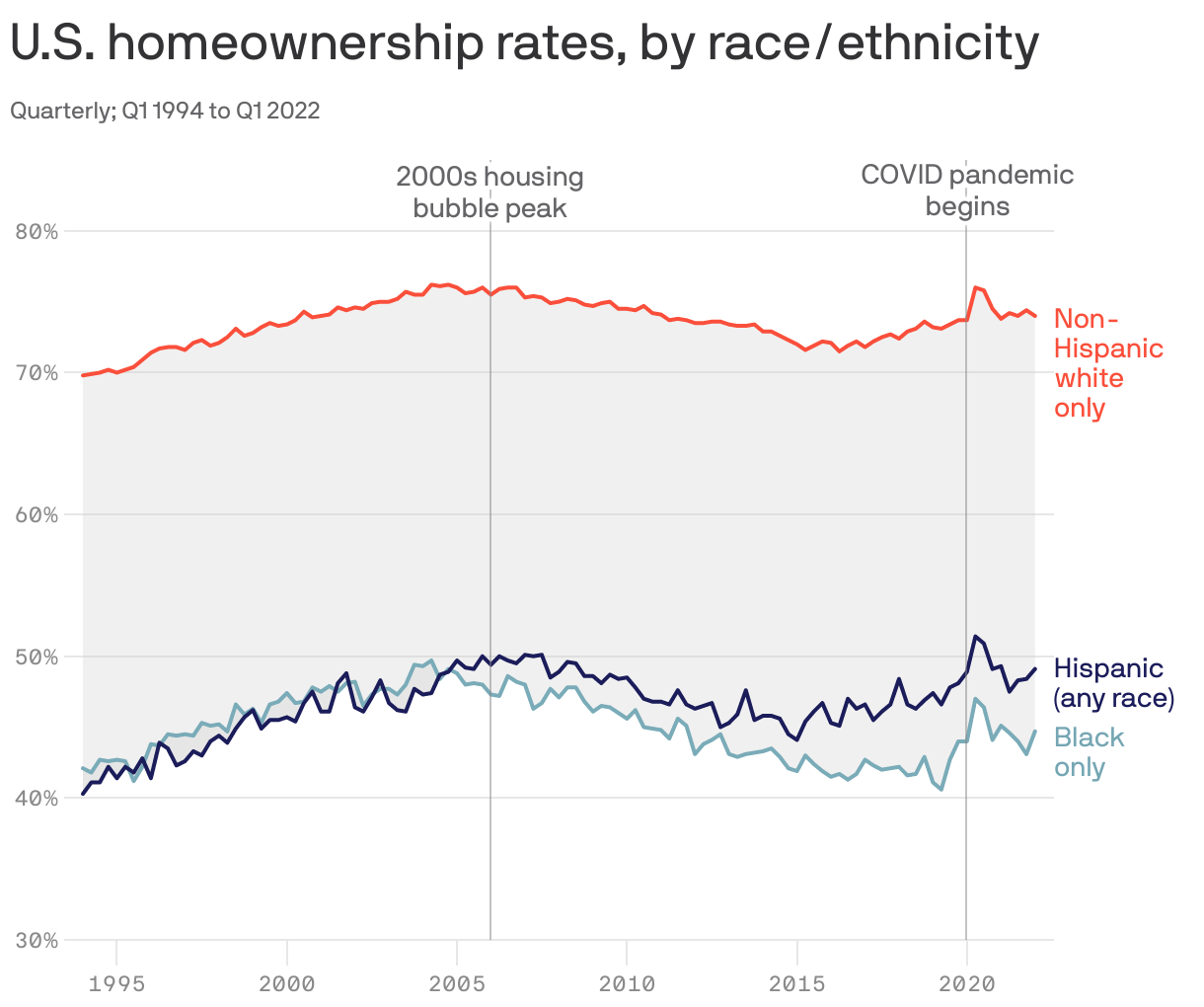

1 big thing: Boosting Black homeownership

For more than a year, Black and Hispanic homebuyers have gotten $5,000 in down payment or closing cost assistance from JPMorgan Chase, part of a new program meant to help close the racial wealth gap, Emily writes.

Why it matters: If adopted on a wider scale, this kind of targeted program — which specifically tracks lending to borrowers of color, a radical departure — might help increase Black homeownership rates. JPMorgan is the first bank to give it a try.

- These types of programs "could provide the kind of homeownership boost to Black communities today that the New Deal provided to white people in the 20th century," write the authors of a February paper published by the Urban Institute.

How it works: The bank created what's known as a special purpose credit program, a policy made possible by the 1974 Equal Credit Opportunity Act that's gaining traction now, especially after federal regulators across several agencies issued a statement on SPCPs in February.

- The law prohibits discrimination in lending, but there's a carve-out that allows banks to create these SPCPs for disadvantaged classes of borrowers.

- JPMorgan implemented the program in specific census tracts with majority Black populations. There are 6,700 such areas across the U.S.

- The bank chose this route instead of simply offering the money to Black borrowers because it's tricky to track the race or ethnicity of homebuyers while staying in line with non-discrimination laws.

Potential drawbacks:

- Gentrification is a "potential unintended consequence" here, Cerita Battles, the bank's managing director and head of community and affordable lending, said at a recent panel on SPCPs.

- The grants could wind up going to white borrowers seeking to move to Black neighborhoods. She said the bank is closely monitoring the process to avoid this. So far, 57%–60% of the bank's SPCP assistance has gone to Black and Hispanic customers, she said.

- The program could also reinforce already existing housing segregation.

The backstory: The large gap in homeownership rates between Black and white Americans drives a massive wealth gap, which in turn perpetuates inequality, as banks typically want to lend to borrowers who already have money.

- "We are deluding ourselves if we believe we will cure centuries of race-based discrimination without targeted measures," wrote the authors of a piece on SPCPs at the National Fair Housing Alliance.

What to watch: In early June, Fannie Mae —a pivotal player in the mortgage market — made SPCPs a central part of a new plan aimed to encourage racial equity in housing.

2. Catch up quick

3. An unsettling pattern

Recent economic reports have repeatedly fallen short of expectations, suggesting slower growth is here, Matt writes.

Driving the news: Friday's report on industrial production failed to match consensus Wall Street forecasts. Factory output declined 0.1% in May. (The forecast was for 0.4% growth.)

The big picture: We're beginning to see a pattern.

- A Thursday report showed housing starts dropped 14.4% in May, compared to April. (Experts expected just a 0.2% decline.)

- The day before, we learned retail sales unexpectedly dropped 0.3% from April to May. (Forecasts called for a 0.2% gain.)

- And the June 10 Consumer Price Index for May showed inflation worsening: Prices rose 8.6% year over year. (Analysts thought it would be just 8.2%.)

Go deeper: In fact, economic data is now falling short of expectations by more than we've seen since the initial shock of the COVID crisis, according to the Citi U.S. Economic Surprise Index.

- How it works: Citi surprise indexes show how economic data compares with consensus expectations.

- Higher numbers mean data has been better than expected; lower numbers, worse.

The bottom line: The Fed is raising rates to slow the U.S. economy and rein in inflation. The slowdown seems to be coming.

4. The friends we lost along the way

Illustration: Maura Losch/Axios

Axios Markets

Stay on top of the latest market trends and economic insights