Axios Markets

May 04, 2023

1 big thing: Housing hullabaloo

Illustration: Aïda Amer/Axios

2. Catch up quick

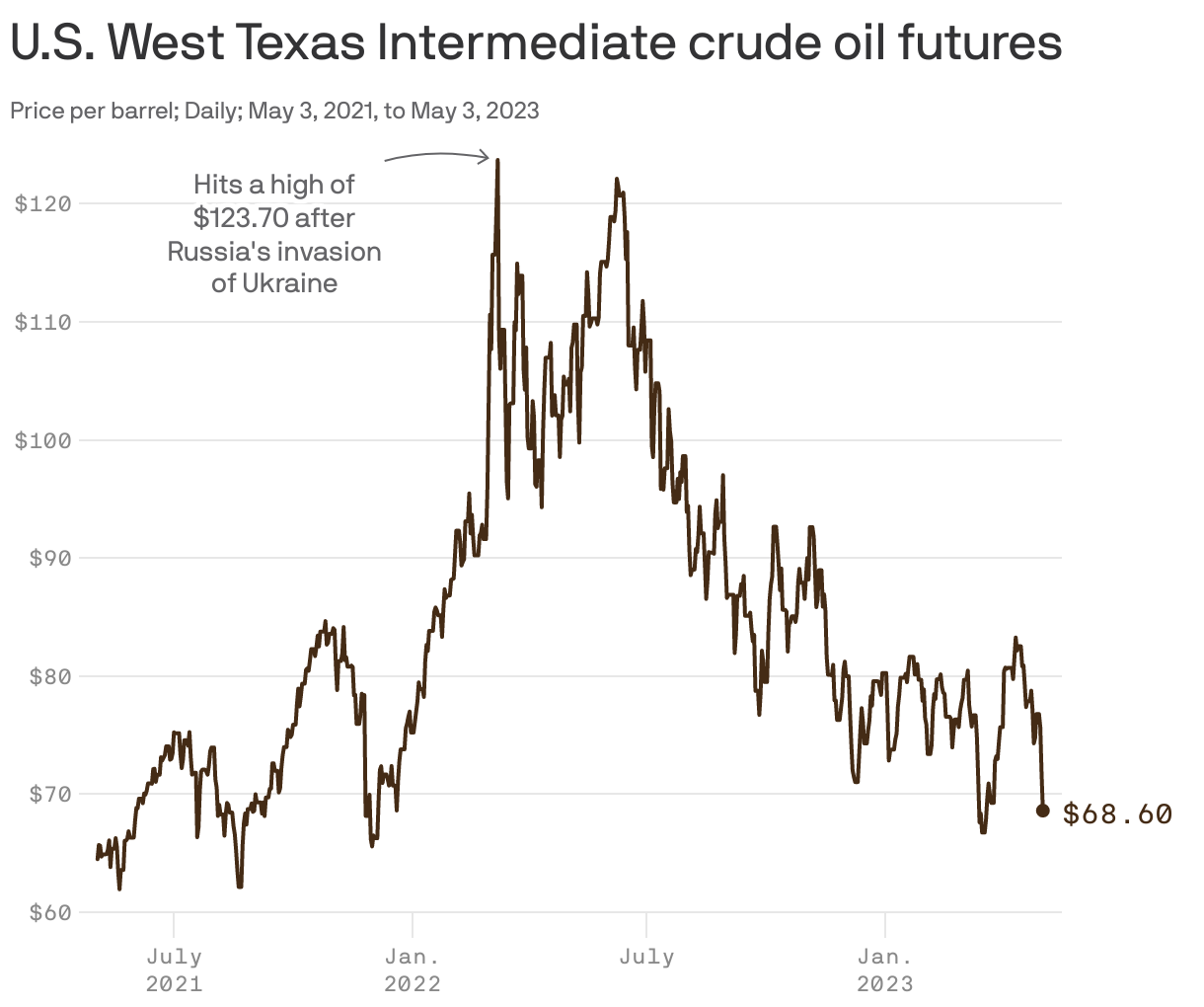

3. 📉 Charted: Crude tumbles

U.S. oil prices fell more than 4% to less than $69 a barrel yesterday, amid what seems to be growing concern about the outlook for global growth, Matt writes.

Why it matters: Oil is a key input into the world economy. Big price moves for crude can signal a shift in investor expectations.

- The downturn in oil prices may mean they expect the economy to weaken.

What they're saying: "Investors seem to be getting increasingly nervous about the macro outlook and its implications for oil demand," ING analysts wrote in a client note Tuesday.

- Prices are down more than 10% this week.

Between the lines: Basically, investors think China's recovery from its disastrous Zero-COVID policies has been pretty lackluster.

- At the same time, they think banking jitters could crimp U.S. growth.

The bottom line: The selloff in crude is consistent with other evidence that the global industrial economy — or the goods-producing part — of the world economy is suffering. But that may not be the end of the world...

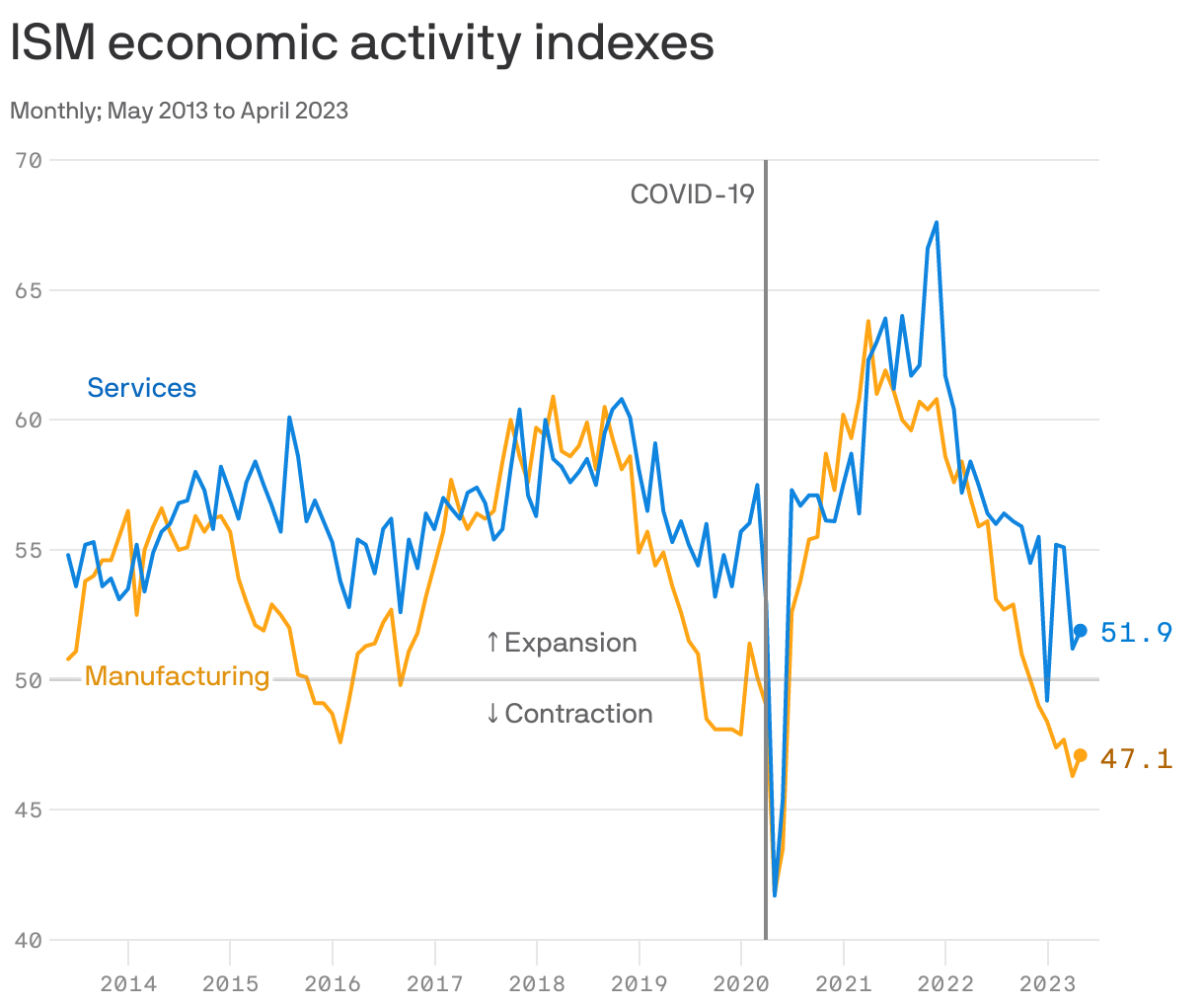

4. ⚖️ Goods vs. services

The economy continues to shift away from buying and selling goods — which was big during and after the pandemic — and back toward services, traditionally the driver of the U.S. economy, Matt writes.

Why it matters: Focusing on the slowdown in manufacturing, or falling commodities prices — such as crude oil, above — may obscure the importance of the service sector, and could give a false impression of how the economy is doing overall.

Be smart: Services — haircuts, restaurant meals, IT consulting, lending money and a vast swath of other activities in which people pay other people to do things for them — accounts for over 70% of the U.S. economy.

The latest: Updates this week from the Institute for Supply Management's surveys of manufacturing and services activity in April confirm the growing divergence between these two parts of the economy.

- Manufacturing is clearly shrinking, while services activity remains above the threshold — 50 —that separates contraction from expansion.

The bottom line: The uptick in services, since it's such a large part of the economy, could outweigh the downward momentum we're seeing in goods.

5. Quoted: Uncharted territory

Axios Markets

Stay on top of the latest market trends and economic insights