Axios Markets

February 21, 2024

1 big thing: Wall Street braces for Nvidia

Illustration: Natalie Peeples/Axios

2. Catch up quick

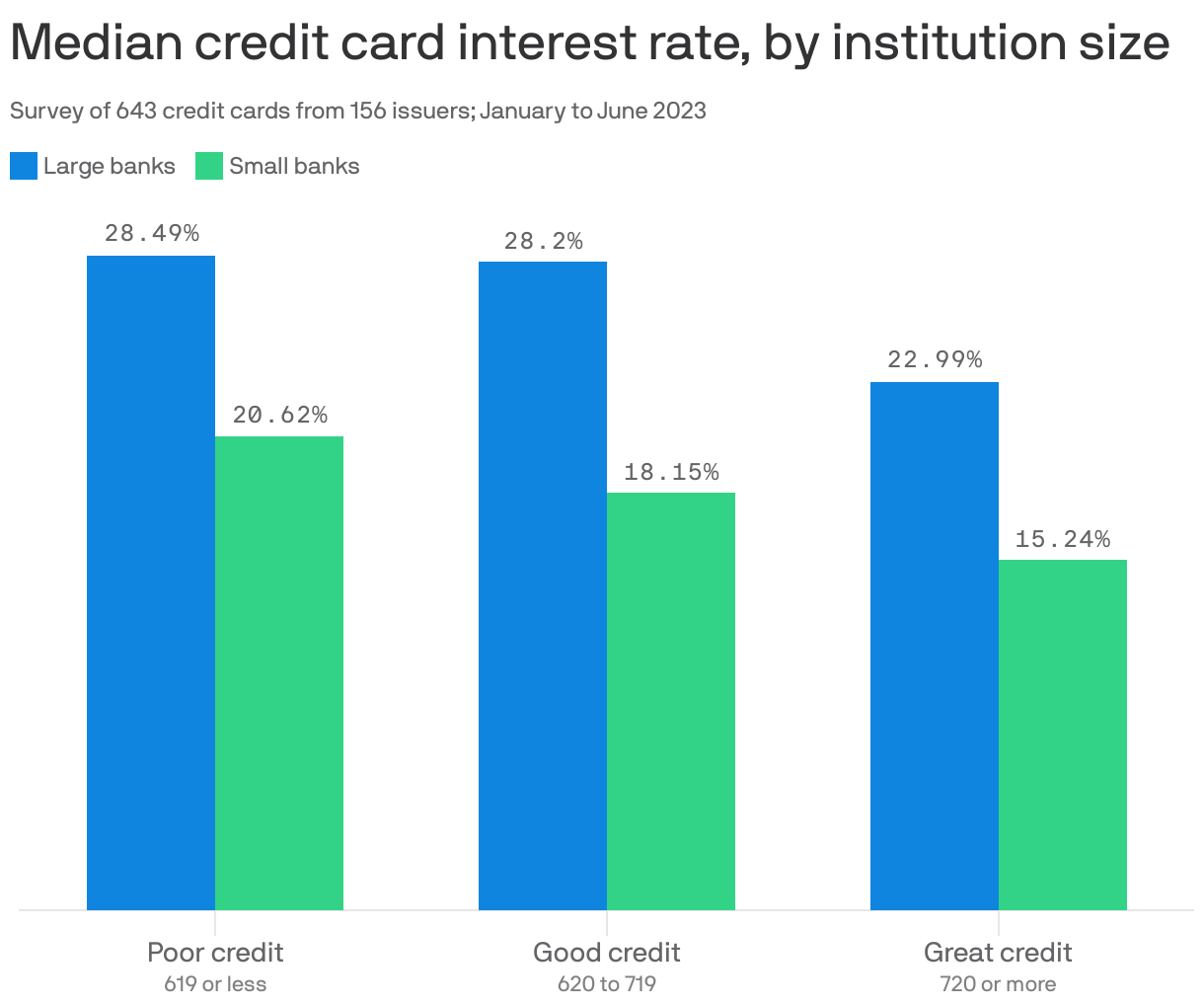

3. 💳 Big credit check

If the Department of Justice decides to challenge the acquisition of Discover by Capital One on antitrust grounds, new research from the Consumer Financial Protection Bureau will surely play a prominent role in the complaint, writes Axios' Felix Salmon.

Why it matters: Even though some 4,000 banks offer credit cards, the top 10 issuers, including both Discover and Capital One, account for more than 80% of loans.

- That concentration seems to have given the biggest lenders the ability to jack up the interest rates they charge on outstanding credit card balances.

The big picture: Consumers with poor credit who have a credit card from a small bank are paying a lower interest rate on their purchases than consumers with excellent credit who carry a card from Discover, Capital One, or one of the other big banks.

- Credit card interest rates have risen sharply over the past two years, spiking from 14.6% in February 2022 to 21.5% in November 2023.

By the numbers: An American who runs an average balance of $5,000 will end up paying between $400 and $500 a year in excess interest payments if they go with one of the big banks.

- On top of that, a holder of a credit card issued by a big bank is three times more likely to be paying an annual fee than someone with a card from a small bank.

What's happening: The biggest banks have massive marketing operations and credit-card reward programs, which make it hard for smaller banks to compete even when their interest rates are much more attractive.

The bottom line: If this deal goes through, Capital One would become the largest credit card issuer in America, with a 19% market share. (JPMorgan currently leads the ranking, with a 16% share.)

- For consumers, however, it's far from clear that bigger means better.

4. Why Discover doesn't worry Visa and Mastercard

Capital One's main argument to antitrust authorities will be that it's going to give Discover the scale it needs to become a serious competitor to Visa and Mastercard.

Why it matters: The big question is whether that argument is going to even pass the laugh test, Felix writes.

The big picture: Visa and Mastercard are pure-play card networks with extremely strong international brands and enviable pricing power.

- Discover, by contrast, is a card issuer, a bank, and a card network all rolled into one. All three of them together are worth $35 billion to Capital One — which means the card network, on its own, is worth just a fraction of that price.

- Visa and Mastercard are behemoths in comparison, both valued at over $400 billion. They have little to fear from Discover, especially since now all banks that aren't Capital One will be even more reluctant to issue cards on the Discover network.

The bottom line: The Discover network will be valuable to Capital One, which says it's likely to save $1.2 billion per year by switching its own debit cards over to the Discover network. But don't expect Discover to become a true Visa competitor.

Axios Markets

Stay on top of the latest market trends and economic insights