Axios Markets

March 27, 2023

1 big thing: Where some of those deposits went

Over the last couple of weeks, cash crowded into U.S. money market funds at the fastest clip since the COVID crisis hit, Matt writes.

Why it matters: The flow of dollars to money market funds for safekeeping highlights the anxiety that the collapse of Silicon Valley Bank introduced into the financial system.

State of play: The overwhelming majority went into funds that invest in only the safest U.S. government securities, such as short-term Treasury bills and overnight loans to the Federal Reserve, known as "reverse repos."

- "This suggests institutional deposits are leaving the U.S. banking system," wrote analysts with Moody's, referencing the large deposits controlled by corporations and small businesses that are not explicitly insured by the FDIC, due to their size.

- Such accounts have appeared especially flighty since the crisis broke out.

Meanwhile: Some of the cash moving into money market funds also comes from the sales of stocks and bonds that picked up amid the banking jitters.

- For example: About $10 billion flowed out of equity and bond mutual funds in recent weeks.

Between the lines: While government-bond-focused money market mutual funds are not explicitly guaranteed by the government, they can conceivably be considered safer than banks, since they use investors' cash to buy some of the most highly rated, short-term, and easy-to-trade investments on Earth.

- The concern about banks is that, like Silicon Valley Bank, they invested in longer-term government bonds that can generate losses if they're forced to be sold to come up with cash for depositors.

- Oh, and the yields investors earn for stashing cash in money market funds are now actually quite high — more than 4% in some cases — compared to bank deposits (now yielding roughly 0.35%, the FDIC says).

The bottom line: "Not only are money market funds offering superior yields, but they also look safer than bank uninsured deposits," wrote JPMorgan analysts in a note last week.

2. Catch up quick

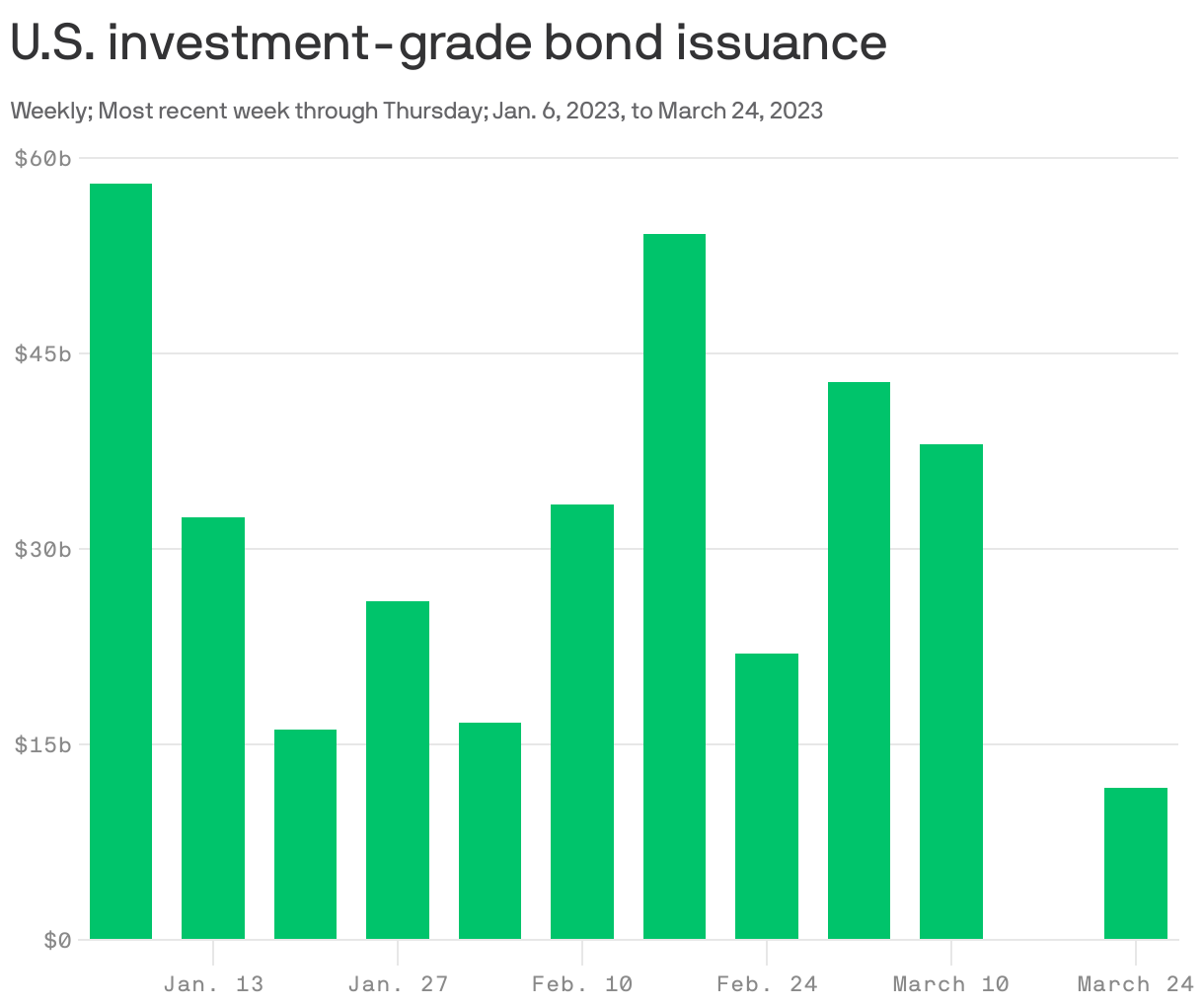

3. Deal freeze

Deals in the corporate bond market came to a halt after the abrupt bank failures earlier this month, Axios' Kate Marino writes.

Why it matters: For all the talk of an eventual credit crunch working its way through the system, this is one example of how the flow of credit can seize up pretty quickly.

What happened: There’s been record volatility in the Treasury market that corporate bonds are benchmarked to — and spreads have moved wildly amid investor concerns that a soft landing is looking less likely.

- That makes it near impossible for investment bankers to give their corporate clients a sense of where they can price a deal. Expectations when a deal launches to market in the morning could be out the window by the end of the day.

- It’s not a great look for a banker — or for a company trying to raise money — to bring a deal to market that they have to either materially change or pull altogether. Better for all involved to just wait out the volatility.

By the numbers: Zero investment-grade bond deals priced during the week after the failures of Silicon Valley Bank and Signature Bank, according to Pitchbook LCD. Deals started up again last week, but as of Thursday, it was the second-slowest week of the year.

- In the high-yield bond market (for riskier companies with lower credit ratings) there was zero issuance last week, and near-zero in each of the two weeks prior.

What we’re watching: The corporate bond market may crank back to life if volatility subsides. But in a deeply interconnected financial system, ripple effects like these may continue to play out for quite some time.

4. Muzzles come off

Illustration: Aïda Amer/Axios

Axios Markets

Stay on top of the latest market trends and economic insights