Axios Crypto

September 27, 2023

🥸 1 big thing: Unregulated ramps

Illustration: Shoshana Gordon/Axios

🍰 2. Charted: Arbitrum leftovers

"Wen token" so the saying goes, Crystal writes.

Flashback: Arbitrum, one of the more popular blockchains built atop Ethereum, airdropped its much-anticipated governance token ARB to its users in March — opening a six-month-long claim window.

Driving the news: That window just closed, with 93.3% of addresses having claimed those tokens, according to a Dune dashboard by Blockworks Research.

- Roughly 69.4 million ARB remained unclaimed.

- So after a vote about what to do with the leftovers, the Arbitrum Foundation sent the remainder to the DAO by the same name.

What he's saying: "We knew we'll never get to 100%, because we knew there would be some wallets not claiming," Offchain Labs co-founder Steven Goldfeder tells Axios.

- Some of their employees wouldn't claim, per policy.

- Others may have simply forgotten.

- And 93% retention isn't bad anyway, Goldfeder added.

Quick take: Tokens worth roughly $56 million is pretty good for leftovers.

🎁 3. Celsius bankruptcy's end

Illustration: Shoshana Gordon/Axios

🚴 4. Catch-up quick

Illustration: Shoshana Gordon/Axios

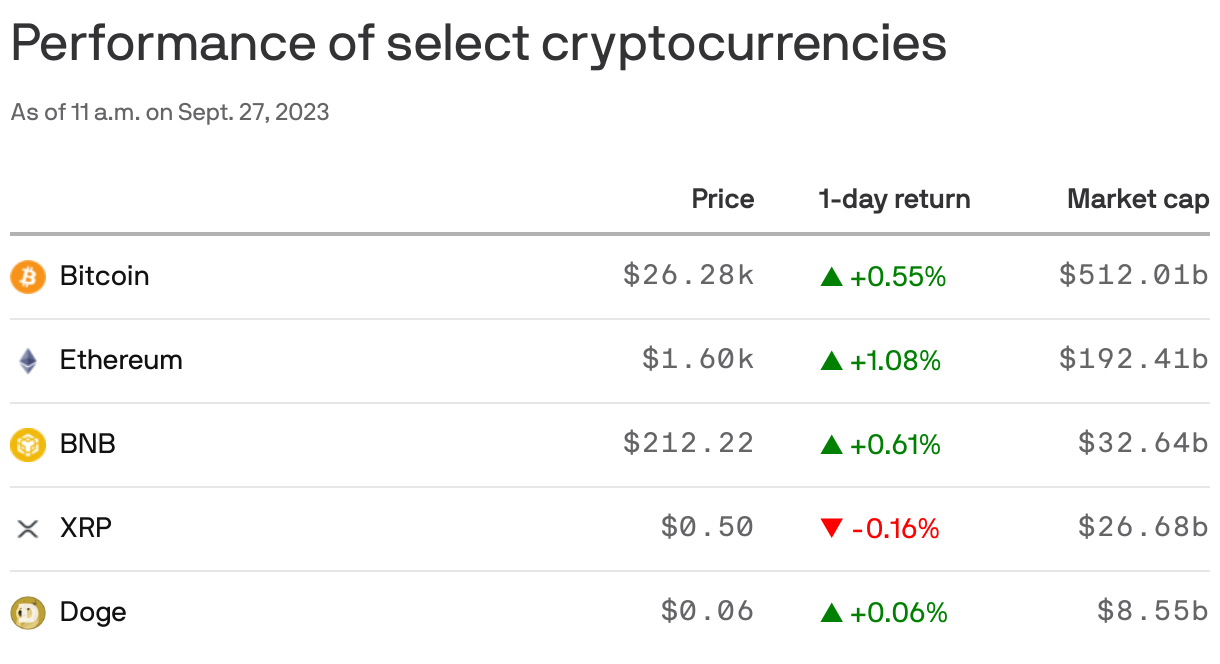

Top coins

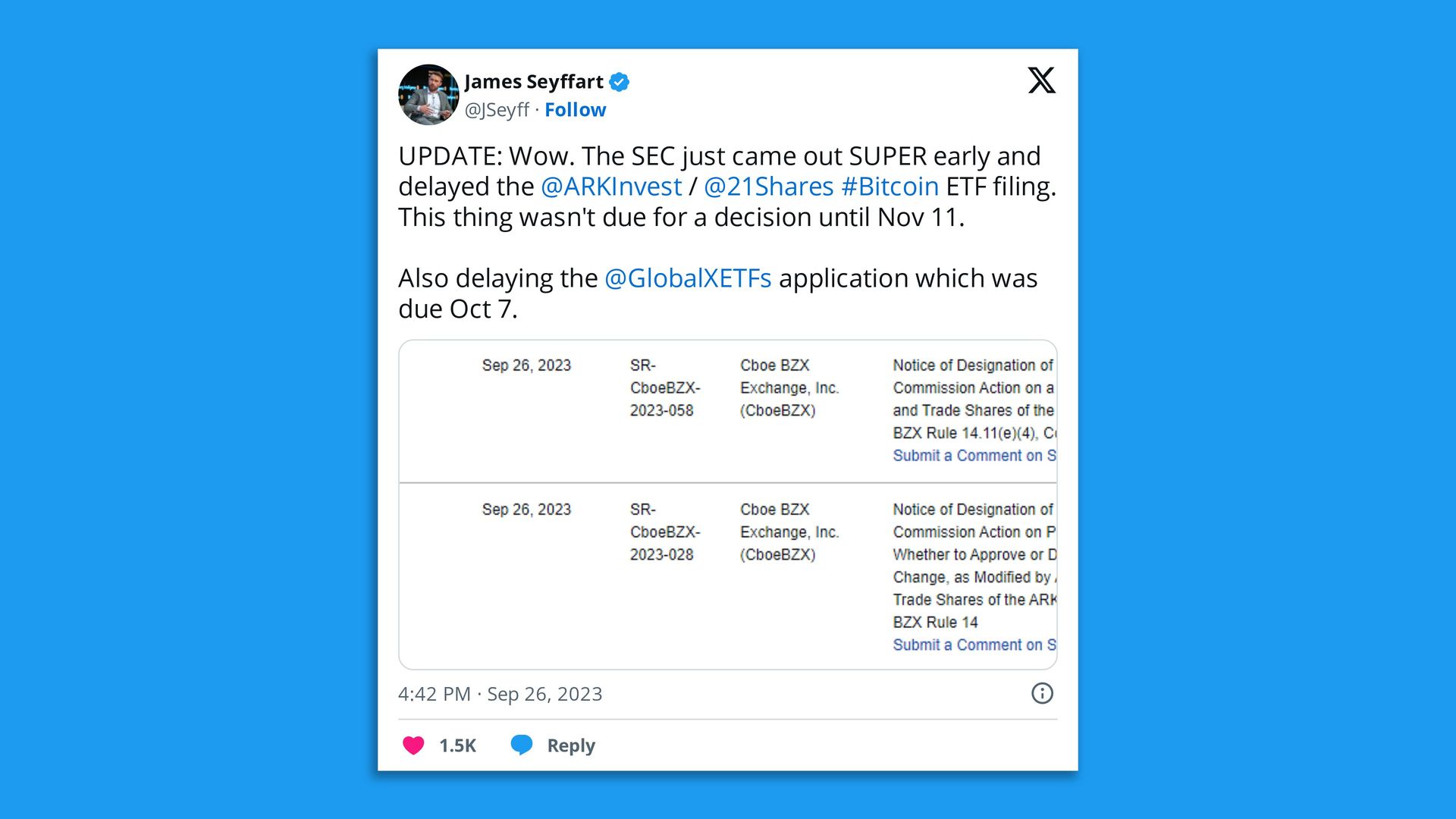

5. 🥫 Culture hash: Kick the can

Screenshot: @JSeyff (social media)

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.