The CDC announced today that it has created new metrics for determining when people should use masks and take other COVID precautions, and now recommends universal masking for less than a third of the U.S. population.

Why it matters: The new metrics are intended to reflect the evolution of the pandemic amid widespread vaccinations and the less-severe Omicron variant.

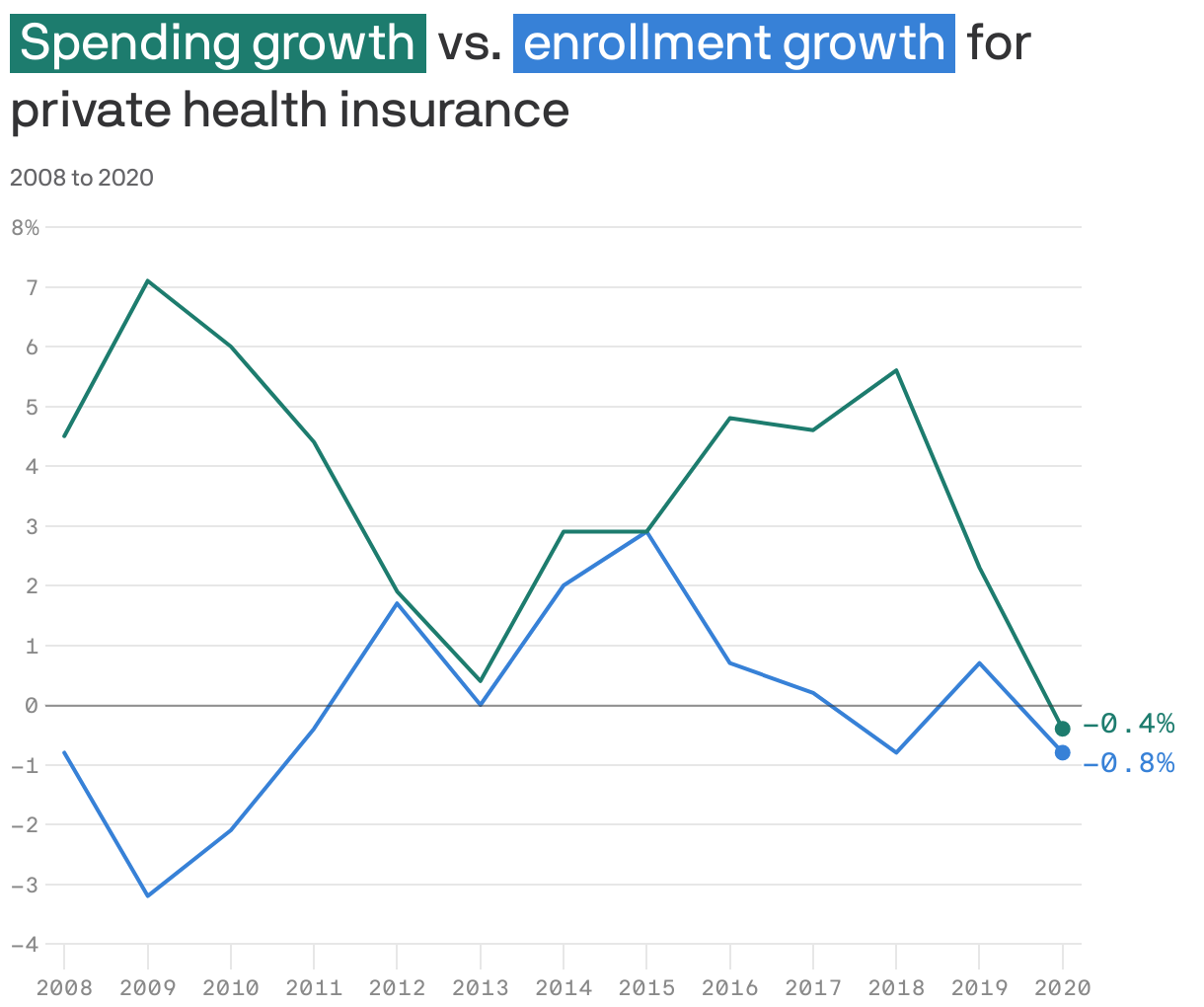

The pandemic disrupted nearly every facet of health care. But it hasn't changed the way hospitals, doctors, drug companies and other health care firms continue to charge employer health plans — and workers — whatever they want.

What they're saying: "The big honking problem is the prices that are being paid in the commercial sector," said Mark Miller, the former head of the Medicare Payment Advisory Commission who is now at Arnold Ventures.

As employers struggle to tame health care's market power, they have used the tools of less generous coverage — higher deductibles, copays and coinsurance — to offset some of the rising premiums.

Why it matters: Workers are increasingly finding their health insurance doesn't feel like insurance.

Employers support reforming how workplace health care is paid for and covered, but various coalitions don't agree on the details or how significant changes would actually be.

What they're saying: "None of us are going to say that this is a perfect system. There's a lot of frustration," said Jim Klein, CEO of the American Benefits Council, a lobbying group that advocates for corporate health benefits. "But compared to any alternatives, this system has earned a lot of trust."

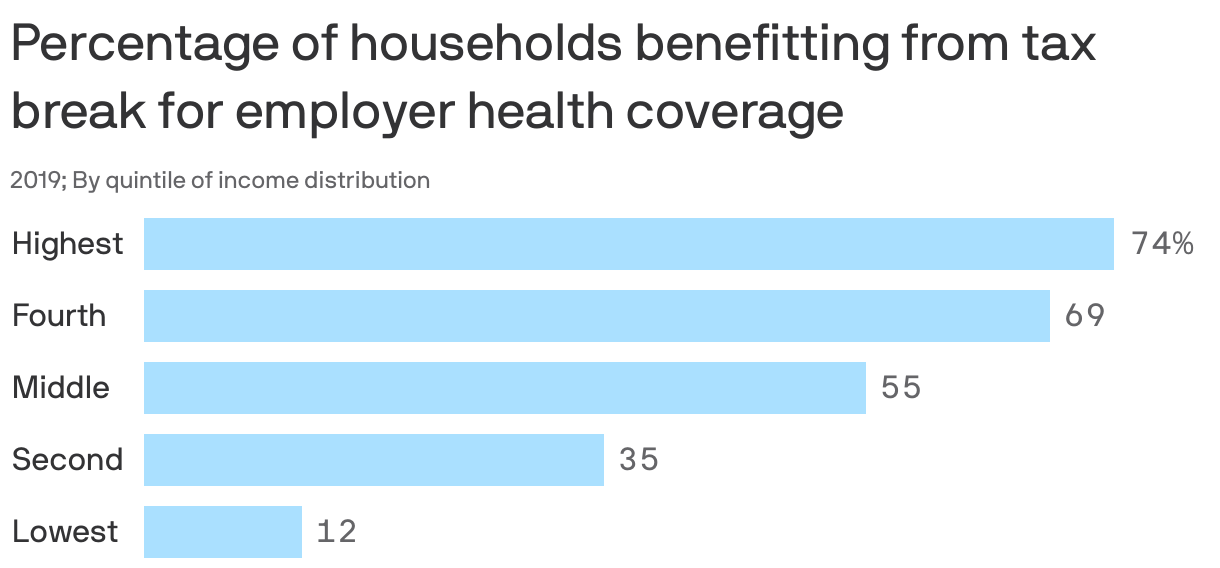

Employer coverage is the country's largest tax break, and the idea of taxing that benefit to help expand coverage is usually met with widespread outrage from both corporations and organized labor.

By the numbers: Employer-paid health insurance premiums, which are exempt from income and payroll taxes, cost the federal government $329 billion in lost tax revenue in 2021, according to the Treasury Department.

The failure of Haven — the joint venture among Amazon, Berkshire Hathaway and JPMorgan Chase — is the most recent example of how employers lack the clout to push back against the market power of increasingly consolidated systems of hospitals, doctors and other medical providers.

What they're saying: "Even big employers aren't big enough within a market to really be able to negotiate down prices, especially with the must-have providers," said Emily Gee, a health economist at the Center for American Progress and former federal official.

Even after decades of being health care purchasers, companies ranging from small shops to Fortune 500 companies may not fully understand the health coverage they're buying and often pay more as a result.

The big picture: "Employers have been forced to look around and assemble this hodgepodge of vendors," said François de Brantes, a senior vice president at Signify Health. "The vast majority don't have sophisticated benefit teams."

Health care is a major benefit in attracting employees, but the rising costs serve as a barrier for small employers that already have a more difficult time competing for workers.

The big picture: Only 58% of companies with fewer than 200 workers and 31% of companies with fewer than 50 workers offer health insurance, and that insurance comes with much higher deductibles on average, surveys show.