Stocks climb, bond yields recede as Treasury and Fed calm markets

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

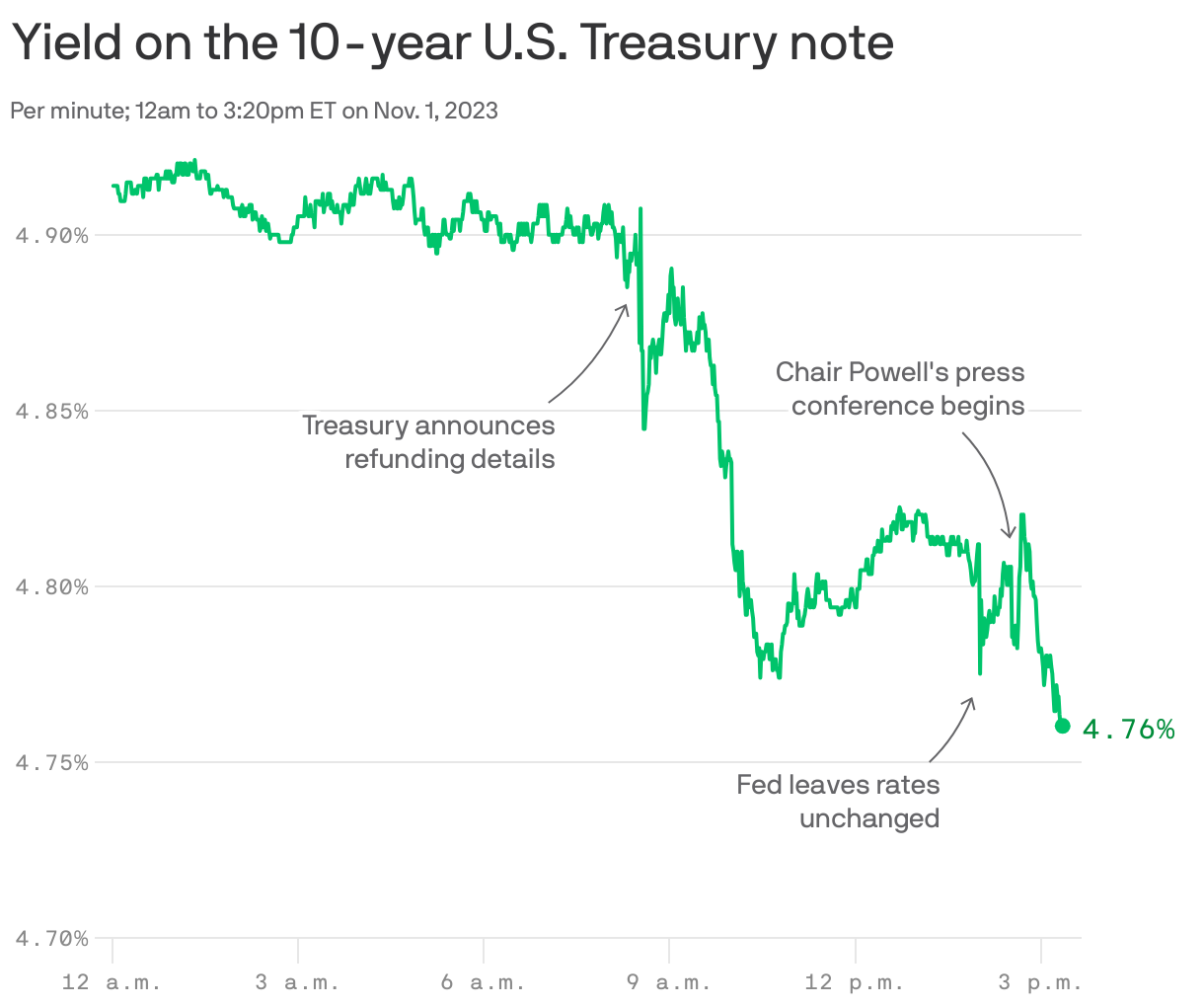

Open embedded content from datawrapper.dwcdn.netA big day in the Treasury market went smoothly, driving yields lower.

Why it matters: The recent rise in yields took the wind out of the stock market's sails over the last couple of months.

- The T-note yield had climbed to 16-year highs just shy of 5% by late October, from less than 4% at the end of June.

Driving the news: The Fed left monetary policy unchanged Wednesday and the Treasury detailed smaller-than-expected sales of long-term securities, setting off a rally in Treasury prices, which pushed yields — which move inversely — lower.

- The lower yield helped push the S&P 500 up 1.1%, in its third straight gain.

Zoom in: Bond yields started to fall at around 8:30am when the Treasury Department issued the latest update on the details of its quarterly process of rolling over maturing debt and financing any new deficits, known as the "quarterly refunding."

- Essentially, the Treasury announced plans to sell a more modest amount of long-term debt than the market seemed to expect (instead, it boosted its plans for shorter-dated notes).

How it works: The basic logic of markets is, if a product is in lower supply, and demand stays more or less the same, prices should rise.

- That's what happened in the Treasury bond market, as the announcement of lower-than-expected supplies of long-term bonds pushed Treasury prices up, and yields lower.

Separately, the Federal Reserve at 2pm announced that it would leave short-term rates alone, instead of hiking again. Half an hour later Fed chair Jerome Powell's news conference reinforced the idea that the already implemented rate hikes are still working their way through the economy, so the central bank is in no rush to hike further.

- In other words, although rate cuts aren't on the table, it doesn't seem like many more hikes will be needed to slow down the economy, either.

What they're saying: "Our read is that the Fed is in the process of transitioning into the next logical stage of the cycle – i.e. leaning on the higher-for-longer messaging to avoid being pressured to cut rates before the Committee deems it prudent," wrote analysts with BMO Capital Markets.

The bottom line: The bond market seems to like that kind of message, and so do stocks.