Small bank struggles could hit the real estate market hard

Add Axios as your preferred source to

see more of our stories on Google.

A pullback in lending among small banks in the U.S. was already underway before the collapse of Silicon Valley Bank and Signature Bank. Now economists expect to see more tightening.

Why it matters: Stricter lending standards among smaller banks is likely to slow economic growth overall. But the commercial real estate sector, already battered by rising interest rates and half-empty office buildings, is particularly at risk.

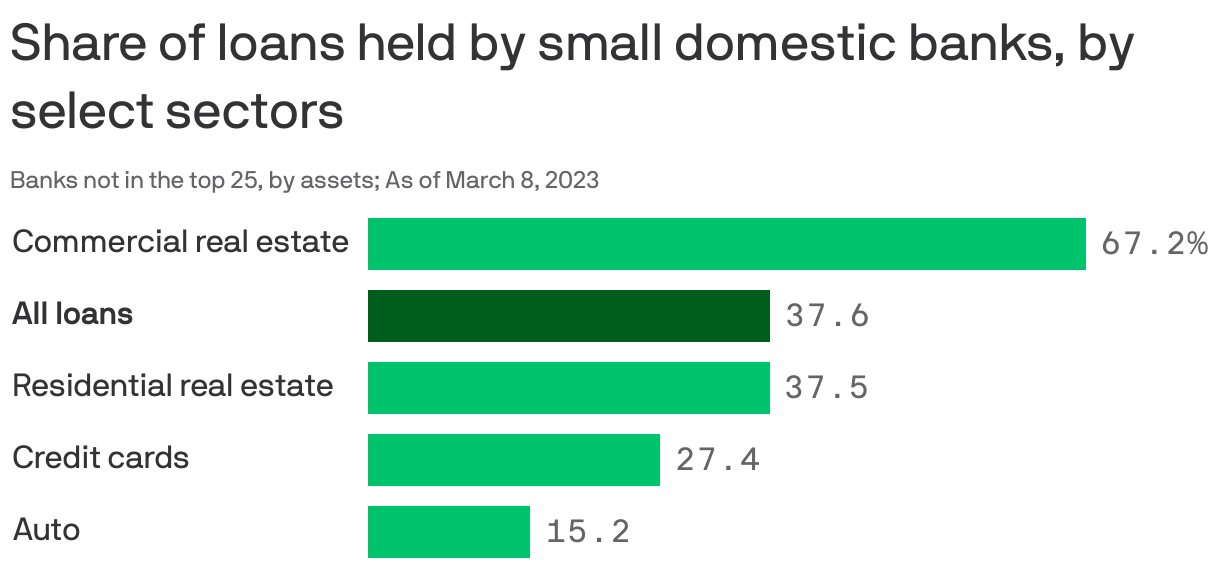

The big picture: Big banks get a lot of attention, but there are about 4,800 banks in the U.S. — and the small ones play a large role in the economy, as a recent Goldman Sachs report notes.

- Small and midsized banks, defined as domestically chartered banks not among the 25 largest, currently hold 67.2% of all outstanding commercial real estate loans, and 37.6% of loans overall. (h/t: Wall Street Journal for chart inspiration.)

- These small players grease the wheels of the economy in all kinds of ways, particularly in specialized areas and regions. Think, Signature Bank's lending to Broadway or SVB's lending to startups.

Zoom out: By the end of last year, banks were already pulling back on lending, as they saw more deposits head out the door, said Chad Littell, CoStar Group's national director of U.S. capital markets analytics.

- Regular consumers had burned through excess savings, and needed money to pay the bills. And some companies — like the tech startups who banked at SVB — were seeing a greater need to access their cash, too.

- About 40% of loan officers said they had tightened lending standards in the commercial real estate space during the last quarter of 2022, per an analysis of the Fed's most recent quarterly survey of loan officers by CoStar. Only about 5% said they were tightening at the end of the previous year.

Meanwhile: Another huge area of office building financing — the market for commercial mortgage-backed securities (CMBS), where banks bundle the loans and resell them to investors — is seizing up. Sales of these deals were down 85% in February, compared with last year, per Bloomberg.

Between the lines: The failures of SVB and Signature are likely to accelerate the pullback. "The banking sector, which was already limiting its exposure to real estate, may look to restrict lending even further after the recent collapse, especially among regional and community banks," Littell wrote in a recent report.

- Yes, but: Since lending standards were already tight, it's possible the impact of these recent bank failures "might be more limited," write the Goldman authors.

Where this surfaces first: Probably in the most distressed part of the real estate sector, offices — particularly Class B.

- Those most at risk: Companies with floating-rate loans whose interest burdens have become increasingly unaffordable, or those with loans scheduled to mature soon. "That's probably the biggest area of concern," Littell said.

What to watch: How this pullback trickles out to regular folks and the economy — and whether it makes it harder to get car loans or other kinds of consumer loans.