Coinbase Global's second quarter reflects crypto slowdown

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Aïda Amer/Axios

Coinbase Global stepped into the spotlight for its earnings show-and-tell and delivered the stinker of a performance everyone expected.

Why it matters: Coinbase is the crypto industry's main character at the moment. As the highest-profile publicly traded crypto company in the U.S., its results are watched by many as a proxy for the health of an entire industry. And lately, it has become the venue for a public battle between it and securities regulators over what is not allowed.

Catch up fast: The crypto exchange reported a $1.1 billion net loss for the second quarter (roughly half of which was due to crypto price drag) and revenue of $803 million, down 31% compared to the previous quarter.

- Its stock fell 11% and extended losses in post-market trading Tuesday.

Of note: If anyone was hoping for something illuminating on the Great Securities Debate, the company's earnings call was a big disappointment.

- "In May, the SEC sent us a voluntary request for information, including about our listings and listing process. We do not yet know if this inquiry will become a formal investigation," CEO Brian Armstrong said in reference to the seven assets listed on Coinbase's platform that have been deemed securities.

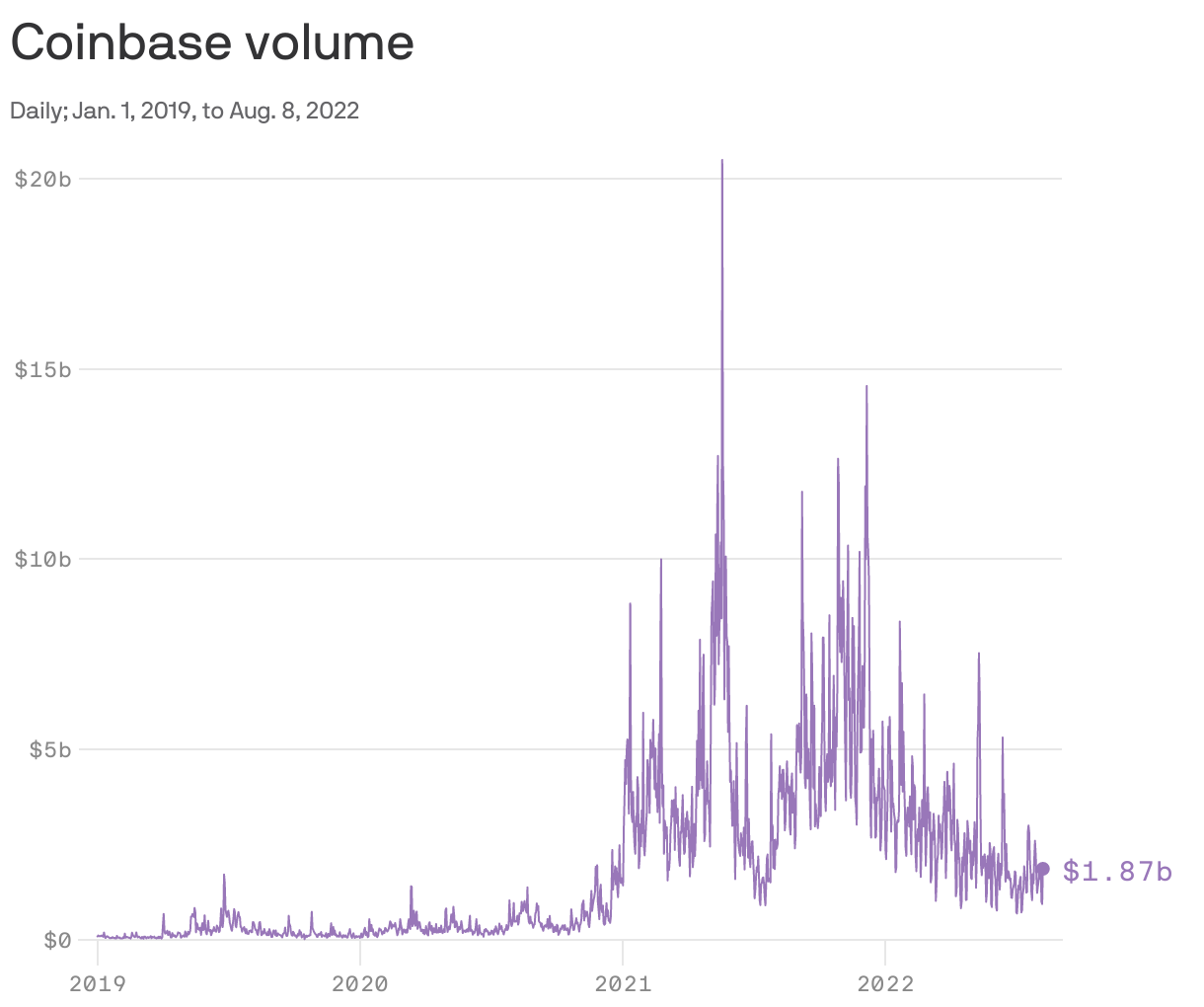

State of play: Coinbase's business model relies heavily on regular people, with retail customers' transaction fees accounting for the lion's share of its revenue. Now those people are trading less.

- Monthly transacting users fell to 9 million from 9.2 million in the previous quarter.

- Of its net revenue of $803 million, $655 million was in transaction revenue and the rest from subscription and services.

- Of that transaction revenue, its retail customers accounted for $616 million, down 36% form the first quarter.

- By comparison, institutional transaction revenue (from the likes of hedge funds, mutual funds and ETFs) was $39 million, down 17% over the same period.

Between the lines: Coinbase took a $42.5 million restructuring expense as a result of reducing its headcount by 18%.

- Non-cash impairment charges relating to crypto investments and venture investments were $446 million. That ate into profits due to an accounting quirk.

What others are saying: "What is baked in [to the stock] — significant pessimism," BTIG analyst Mark Palmer said. He has a buy rating on shares, but his price target of $290 suggests the stock can climb 230% from Tuesday's closing price of $87.68.

- The big picture: "Coinbase’s institutional platform has largely been overlooked. That's a big part of our bullish thesis," he said.

- "BlackRock is a big step in the right direction" Chris Brendler, analyst at D.A. Davidson tells Axios. "But we're not sure how big of a business that's going to be without details." Brendler has a buy rating on Coinbase and a 12-month price target of $90.

What's next: More of the same.

- Coinbase expects second-quarter trends to persist through the rest of the year.