Axios Pro Rata

May 04, 2024

Good morning, readers! Today we're taking a closer look at continuation funds in the venture world.

- ☎️ Reminder: Feel free to send me tips or comments by replying to this email or on X: @imkialikethecar. (Or ask me for my Telegram or Signal number.)

Today's Smart Brevity™ count is 738 words — a 3-minute read.

1 big thing: Riding the continuation fund trend

Illustration: Aïda Amer/Axios

Continuation funds are taking hold in venture capital: Lightspeed Venture Partners has a term sheet from a lead investor and is hoping to wrap things up by July, while NEA is quietly working on its own vehicle, Axios has learned.

Why it matters: Historically rare in venture capital, they've been getting more attention recently as firms look for new ways to navigate the market downturn and ongoing lack of liquidity.

The big picture: Continuation funds have been a staple of the private equity world, typically used to manage one or a few assets.

- And they perform well. They earn a median of 1.4x multiple on invested capital, on par with secondaries funds and higher than the median 1.2x from buyout funds, according to Morgan Stanley data that looked at 71 continuation funds formed from 2018 to 2023.

Zoom in: In the past year, a small number of venture firms have concluded or begun working on such funds, taking a variety of approaches. For example:

- RockPort Capital moved its holdings in two companies into a new vehicle.

- Lightspeed has selected 10 assets, about 70% of which are in enterprise tech. The group is a mix of companies still several years away from an IPO, some in which it only own a tiny stake, and others the firm just wants to move out of otherwise top-performing funds, according to a source familiar with the transaction.

- Shasta Ventures, meanwhile, wanted to move nearly all its holdings from its last fund into a continuation fund.

- Insight Partners last year closed its second continuation fund, comprising select investments across six of its funds.

Between the lines: One reason for the dearth of continuation funds in VC is the regulatory environment, Joe Binder, a partner at law firm Debevoise & Plimpton who specializes in fund formation, tells Axios.

- The SEC's recent focus on continuation fund transactions and the conflict they can create has led some firms to approach them with caution.

- However, both PE and VC firms are getting more comfortable navigating the regulations.

Another reason: Traditional venture funds can really live for a long time — much longer than the initial 10 to 12 years given at formation.

- For active firms that continue to raise new funds, dealing with aging investments is at worst a hassle.

Yes, but: The devil is always in the details — that is, in the terms.

- Shasta Ventures' recent attempt to move its last fund into a continuation fund was priced at 65% of its 2023 Q3 value, plus 1% in fees and carry based on performance. Limited partners ultimately rejected the vehicle.

- Meanwhile, Lightspeed's own fund is set up to have no additional fees or carry, likely a welcome setup for limited partners. But it'll also have to offer an attractive price.

- "During the tech downturn, there was more pressure on the valuation of venture capital portfolios compared to what you might see in a single-asset continuation fund led by a private equity firm," explains Binder. So buyers have been applying steeper discounts to venture assets.

What we're watching: How enduring this trend remains in the venture world — especially once IPOs and M&A return in full force, and provide long-awaited exits.

2. Zoom in: Both sides

Illustration: Brendan Lynch/Axios

Of course, continuation funds have pluses and minuses. As mentioned above, much of it comes down to the details.

The good:

- They provide liquidity for limited partners who value cashing out now over waiting it out.

- They tend to be known quantities for limited partners — investors know exactly what's in the portfolio and have a sense of how the companies are performing and their trajectories, unlike when they invest in a brand-new fund.

- They can be fantastic deals for the buyers.

- Portfolio companies don't have to deal with newcomers on their cap table.

The (potentially) bad:

- General partners need to make a convincing case for not having a conflict of interest, since they're on both sides of the transaction.

- Can come with fees and carry that some limited partners don't agree are fair.

- Can be significantly underpriced, leaving limited partners with less than ideal options.

📚 Due Diligence

- Tech funds adopt private equity strategies in race to return cash to investors (Financial Times)

- HV Capital launches Germany's first continuation fund of €430m (Sifted)

- Stars align for continuation funds to thrive (Pensions & Investments)

🧩 Trivia

In lieu of trivia this week, if you've dealt with a continuation fund (especially as an LP), send me your thoughts on what happened!

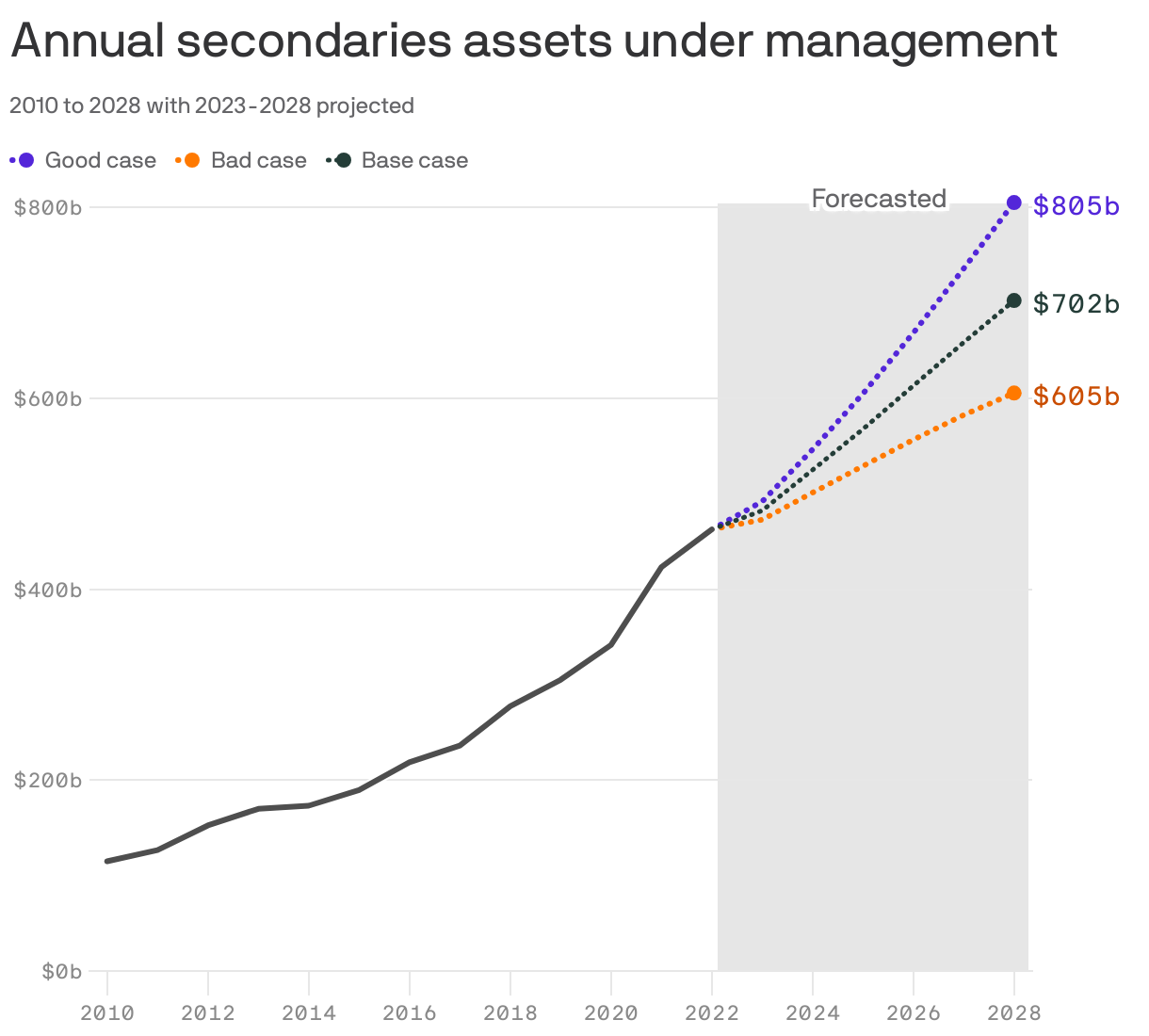

🧮 Final Numbers

🙏 Thanks for reading! And to Javier David and Brad Bonhall for editing. See you Monday for Pro Rata's weekday programming, and please ask your friends, colleagues and secondaries buyers to sign up.

Sign up for Axios Pro Rata

Dan Primack’s briefing on VC, PE & M&A for dealmakers.