Axios Markets

February 14, 2025

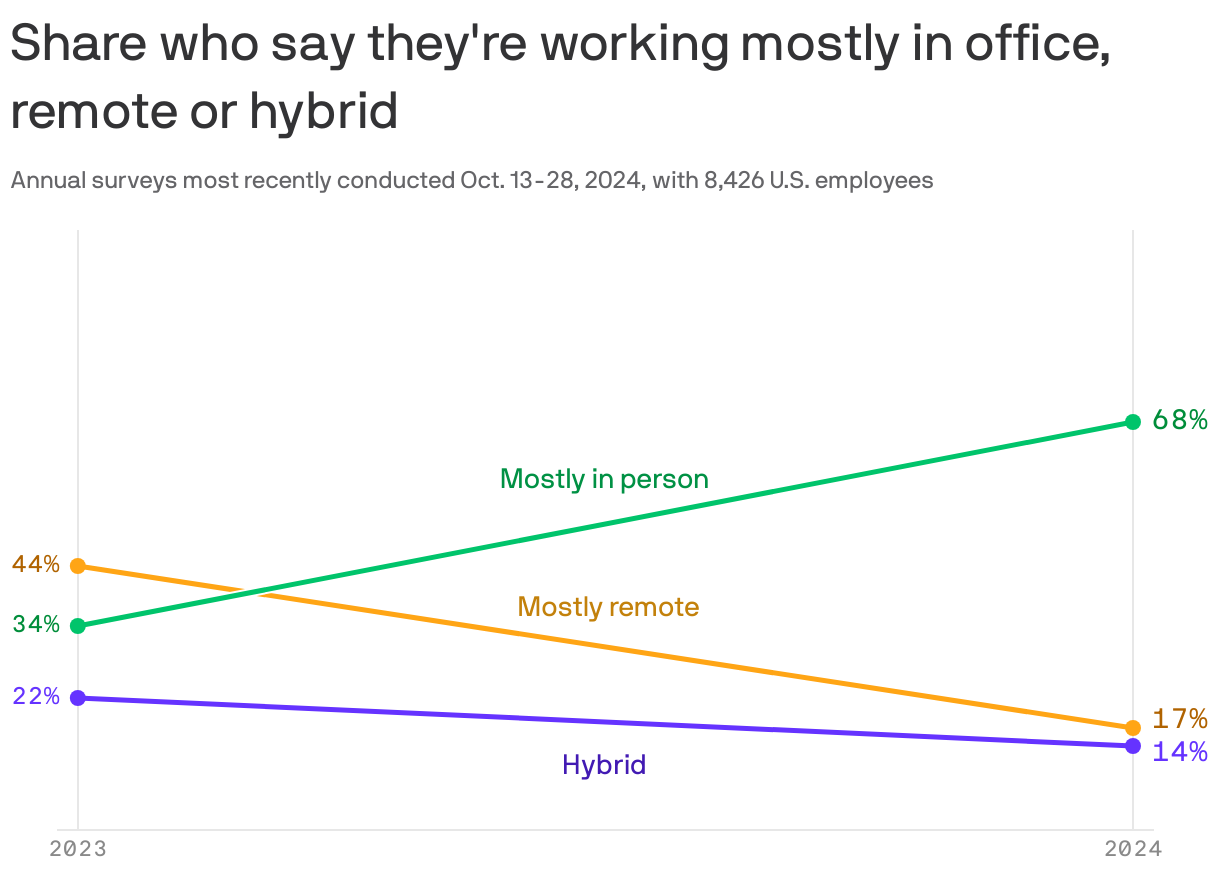

2. Workers are back to their cubicles

The office is back. The share of people who reported working mostly in-person doubled in 2024 from the previous year, according to a McKinsey survey released this morning.

Why it matters: As hiring slows and workers feel stuck, employers are using their newly strengthened upper hand to finally get what they want: butts in seats.

Where it stands: "There is a perception among senior leaders that productivity is better accomplished in office," said Brooke Weddle, a senior partner at McKinsey. (Research paints a more complicated picture.)

- Executives are keen to return to office, Weddle said, noting that in one recent 24-hour period she heard from three different leaders at three companies about it.

The big picture: This survey of 8,426 employees across 15 industries was conducted last October. The RTO push has only intensified since then.

- On Trump's first day in office he ordered federal employees back to the office. Earlier this week, Trump said: "I don't think you can work from home." People who work remotely are "gonna play tennis. They're gonna play golf...They're not working."

- Yesterday, the White House carved out an exception in its in-office policy, allowing federal employees with spouses who work for the military to continue to work remotely.

Flashback: When Amazon called workers back last September, the company opened the RTO floodgates, several observers told Axios. "That turned a wave," Weddle said.

The intrigue: At many workplaces, there's still not enough room for everyone. Amazon is still struggling to fit all its employees into available space, the Wall Street Journal reported yesterday.

Reality check: We aren't all the way back to pre-2020 levels. Even with more RTO mandates there tends to be "wiggle room," Weddle said. "Most policies have some kind of flexibility built-in."

- For that reason, instead of asking if people were in-office or remote, McKinsey asked if people were "mostly" in-person or remote.

- Other recent studies reflect that asterisk. Average office occupancy on Fridays is just 36% of pre-pandemic levels, compared to around 63% on Tuesday, according to recent data from Kastle.

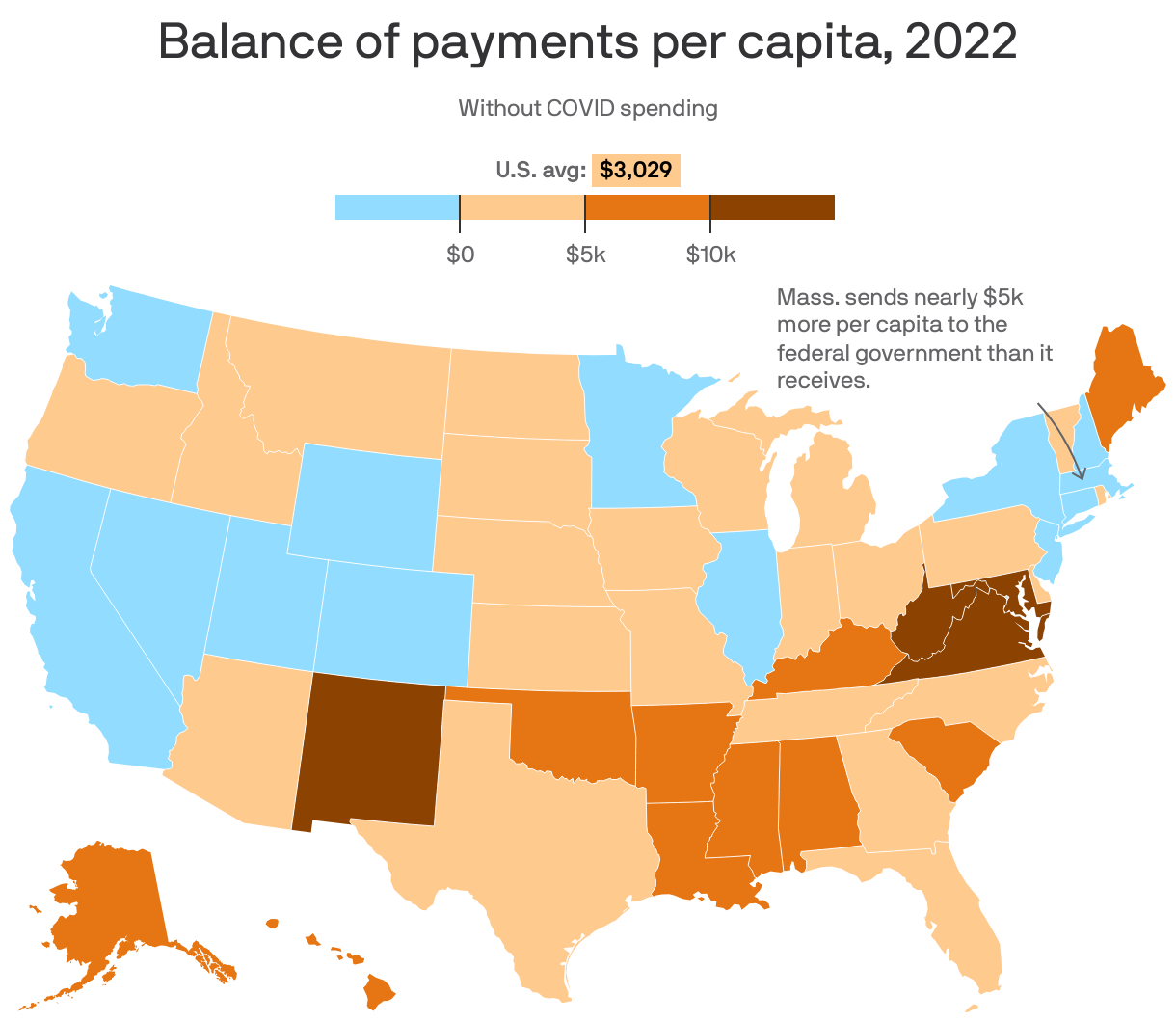

3. Which states net more federal funds

Only 13 U.S. states send more money to federal government coffers than they receive, a recent analysis found.

Why it matters: The Trump administration's push for states to become more financially independent brushes up against the reality that many depend on federal money for everything from disaster relief to food aid.

Driving the news: Massachusetts (-$4,846), New Jersey (-$4,344) and Washington (-$3,494) had the lowest balance of payments per capita as of 2022, discounting coronavirus relief spending, according to a 2024 report from the Rockefeller Institute of Government.

- New Mexico ($14,781), Maryland ($12,265) and Virginia ($11,577) had the highest.

How it works: Each state's balance of payments reflect how much federal money is distributed there (in the form of programs like Medicaid and SNAP, for example) versus how much money residents and businesses send to the federal government (via income or employment taxes, for instance).

- A negative figure means a state sends more to the federal government than it receives, while a positive figure means it gets more than it gives.

Between the lines: "States with large defense-contracting sectors and more military bases receive more federal defense spending, while federal wages are disproportionately concentrated within states with a large federal employee presence," the report noted.

- That at least partially explains the results in states like Virginia and Maryland, which are both relatively high income but have lots of federal workers, contractors and agency offices, thanks to their proximity to D.C.

Axios Markets