Axios Markets

February 03, 2024

1 big thing: The newspaper savior complex

Illustration: Shoshana Gordon/Axios

2. Auction pricing is about to become a lot more transparent

Illustration: Annelise Capossela/Axios

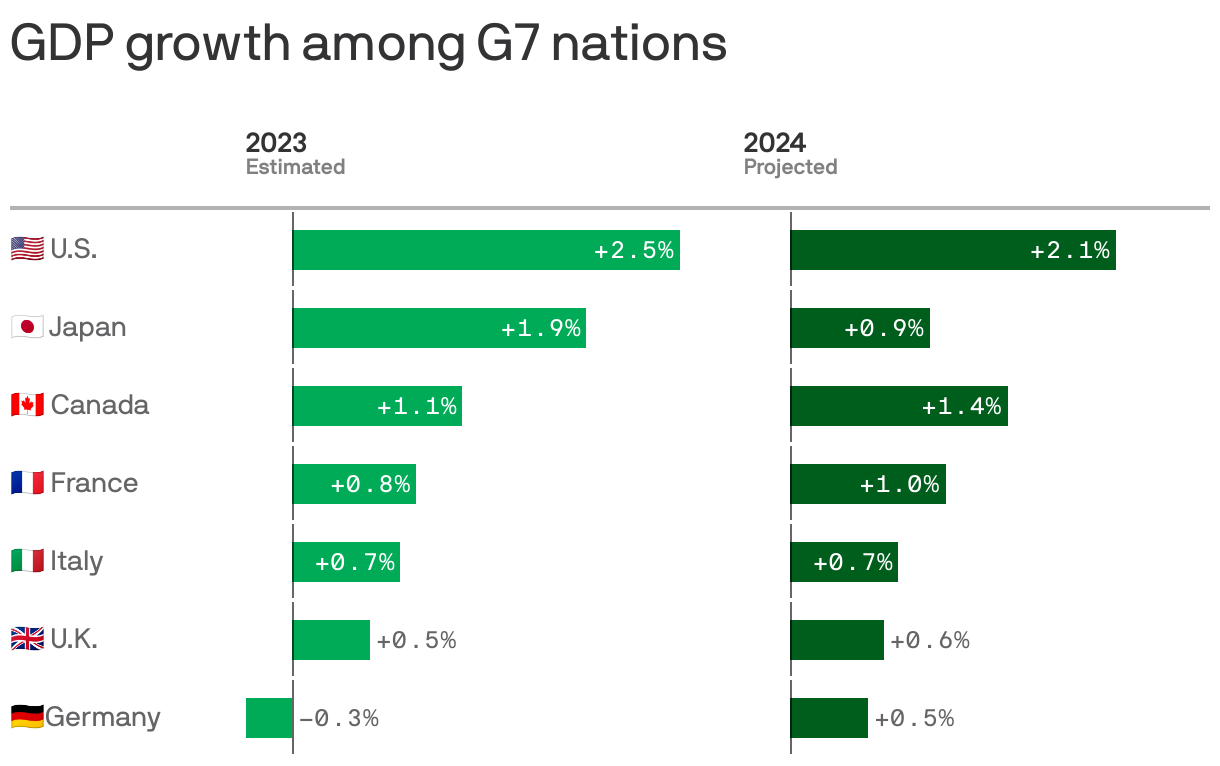

3. The Phoenix Economy

This chart, from Axios' Neil Irwin, understates the degree to which U.S. economic growth has dwarfed that of its international peers. If you measure 2023's growth as the amount by which U.S. fourth-quarter GDP grew from a year previously, the country's growth rate last year was actually 3.3%.

Why it matters: The high growth and boom in productivity — not to mention January's astonishing rate of job growth — are a function of what I called in my book "shaking the Etch-a-Sketch."

- The huge spike in U.S. unemployment in March and April of 2020 — something not mirrored in most other developed countries — presaged an even bigger "great resignation" in which Americans quit jobs they didn't like for more appealing alternatives.

Be smart: We're now reaping the benefit of that great shake-up.

- "The enormous labor market churn of COVID in 2020-21 had the unintended benefit of moving millions of lower income workers to better jobs, more income security, and/or running their own businesses," Adam Posen, president of the Peterson Institute for International Economics, tells Neil.

- "We are reaping the benefits of it now in labor force participation, wage growth, and improved productivity."

The bottom line: In burning down much of the old economy, we created the preconditions for a phoenix to rise from its ashes.

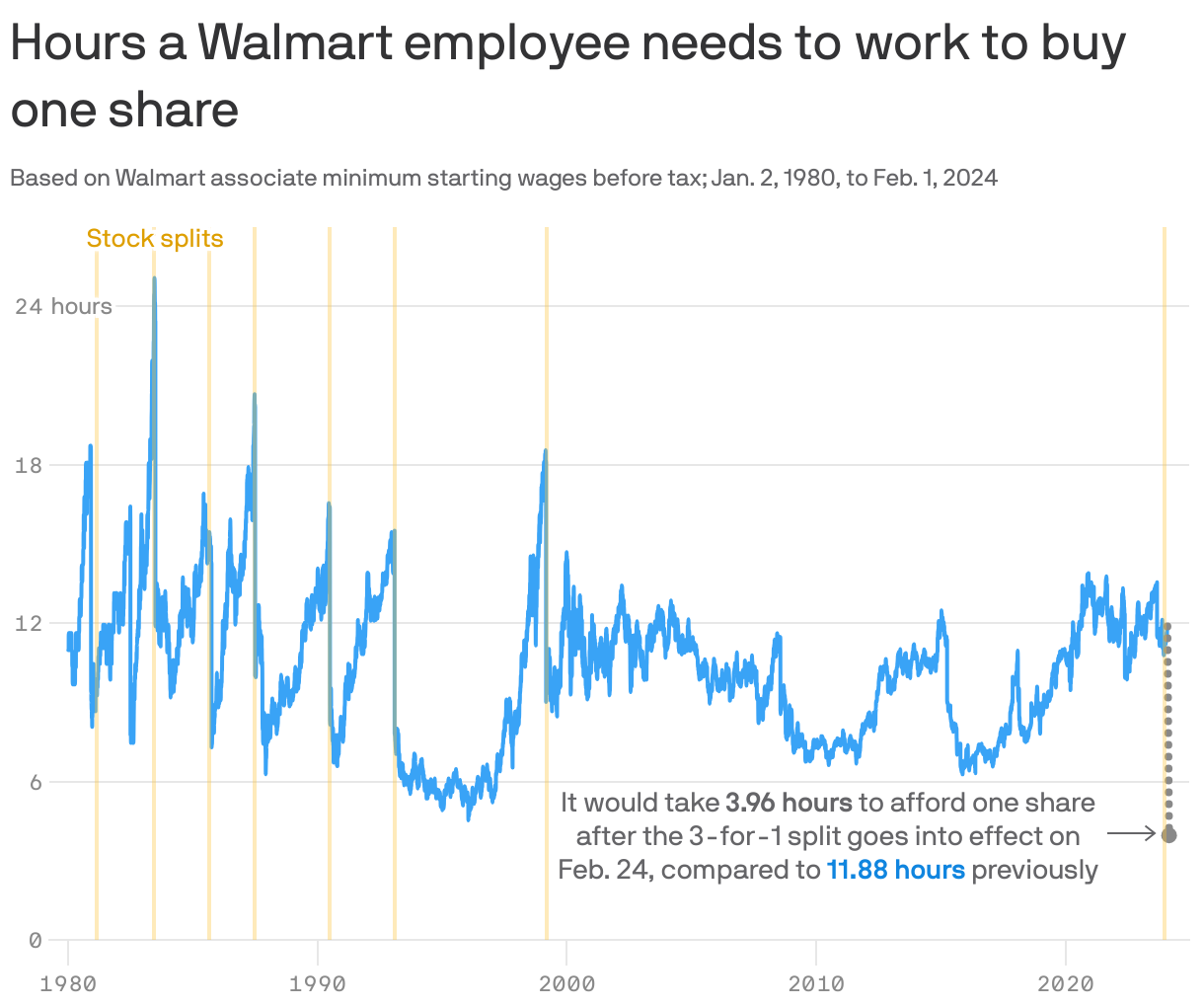

4. Why Walmart split its stock

Walmart stock splits used to be a regular event — there were six of them just between November 1980 and June 1990. But it's now almost 25 years since the last one, in March 1999.

Why it matters: Nowadays, almost every brokerage, including Walmart's own Associate Stock Purchase Plan, allows the purchase of fractional shares, making a company's nominal share price less important than ever.

The other side: Walmart's own press release this week announcing a new stock split quotes CEO Doug McMillon as saying that "Sam Walton believed it was important to keep our share price in a range where purchasing whole shares, rather than fractions, was accessible to all of our associates."

- Walton stepped down as CEO in February 1988, when an entry-level Walmart associate would have had to work more than 8 hours to amass enough pre-tax income to buy a single share.

- After this month's stock split, that ratio is going to plunge to an all-time low of less than 4.

The bottom line: The stated reason for splitting the stock doesn't seem to make a lot of sense — especially given that the split is going to significantly dilute Walmart's contribution to the Dow.

5. Evergrande, in context

Chinese property developer Evergrande, which has now been ordered to liquidate, has an astonishing $300 billion in liabilities.

Why it matters: That places it near the very top of the all-time list of corporate bankruptcies.

Between the lines: A lot of Evergrande's liabilities are down payments that Chinese homebuyers made on apartments that remain unbuilt. But even just looking at the bonds and loans outstanding, the amount is greater than $80 billion.

My thought bubble: In 2020, there was a lot of talk of a "tidal wave" of bankruptcies coming as a result of the pandemic. Turns out, that never really happened. Evergrande's implosion can't primarily be attributed to COVID.

By the numbers: China is no stranger to mega-bankruptcies, as can be seen by the presence of CEFC China Energy and Peking University Financial Group on this list. But Evergrande dwarfs them all.

- What's more, creditors' expected recovery on most of that debt is effectively zero. Insofar as there's still value in Evergrande, expect that to go to the homebuyers rather than foreign bondholders.

- That places Evergrande in stark contrast to Lehman Brothers, which was the largest corporate bankruptcy of all time. While the investment bank had much greater total liabilities, creditors ultimately got paid back in full.

6. The rise and rise of money market funds

More than $6 trillion is now held in U.S. money market funds, up $1 trillion just since mid-March, when the banking crisis hit.

- That's just under $46,000 per U.S. household.

Axios Markets

Stay on top of the latest market trends and economic insights