Axios Markets

July 20, 2023

1 big thing: New banking reality

Illustration: Sarah Grillo/Axios

2. Catch up quick

3. 🪛 Charted: Consumer credit tightens

Lenders have gotten much stricter over the last year, Matt writes.

The big picture: The Fed's quarterly survey of bank senior loan officers — charted above — shows bankers have toughened requirements for credit cards, auto loans, mortgages and various other consumer debt in recent months.

- Consumer lending standards haven't been this stringent since banks slammed the brakes on lending when COVID hit.

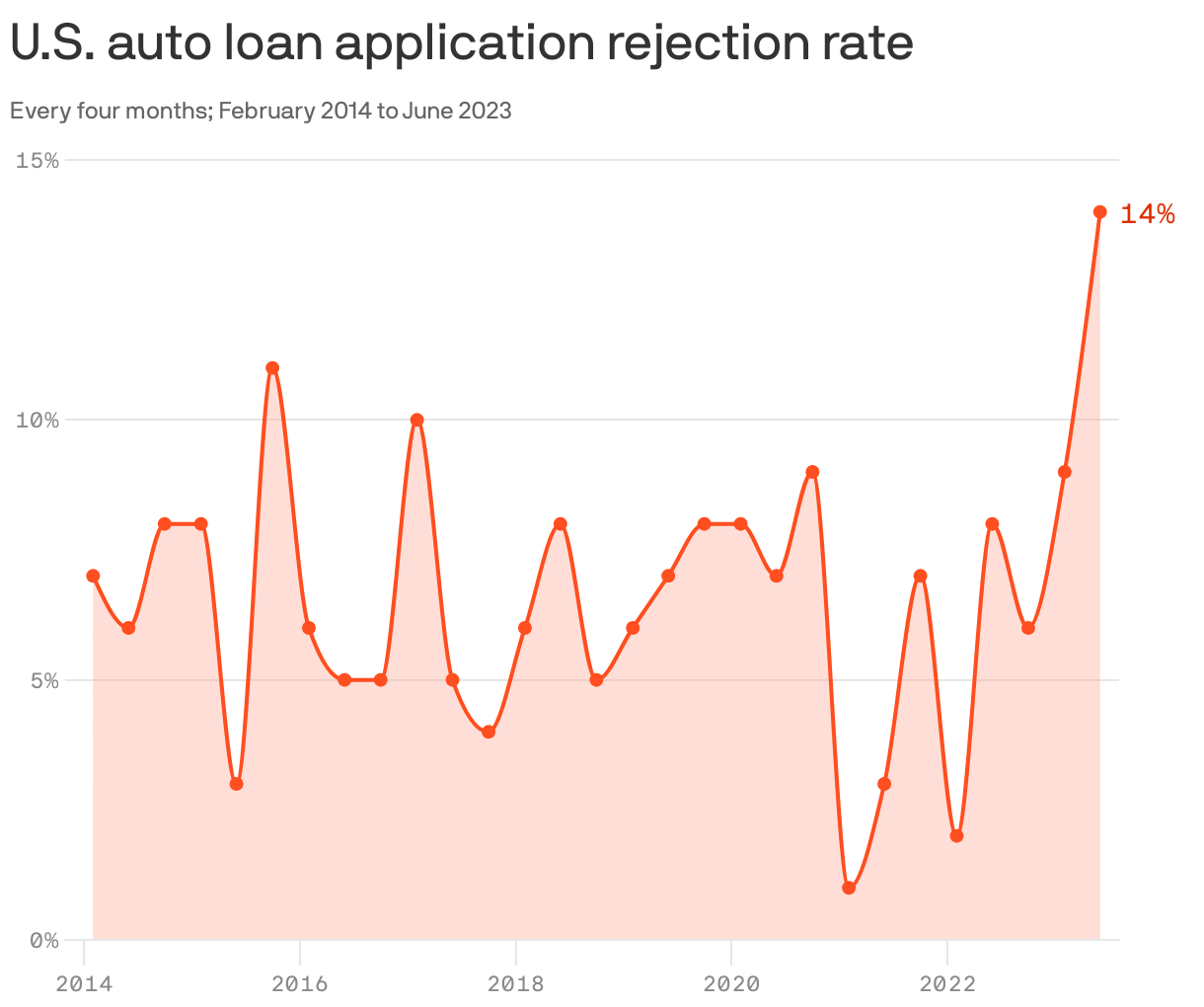

4. Zoom in: auto lending

The rejection rate for auto loans hit a new high in June, per a New York Fed survey out this week, Emily writes.

- That shouldn’t be surprising in the context of the overall tightening of underwriting standards rippling through the banking system.

Meanwhile, with both car prices and interest rates still so high, affordability is falling and delinquencies are rising.

5. Regional bank stocks show signs of life

Stock prices for smaller banks have perked up in recent months, Matt writes.

- The latest: Regional bank stocks rallied hard yesterday, after one of the largest regional players, M&T Bank, posted much better second-quarter profit and revenue numbers than expected.

Worth noting: PacWest Bancorp — which was one of the banks that seemed to be wobbling after Silicon Valley Bank collapsed last March — led yesterday's rally, rising 11%.

The bottom line: As Emily explained above, banks are limping through the aftermath of this year's bank runs.

- After the bout of social media-driven stock losses and bank runs, some investors are now betting there's a recovery to ride in the battered share prices.

Axios Markets

Stay on top of the latest market trends and economic insights