Axios Markets

June 27, 2024

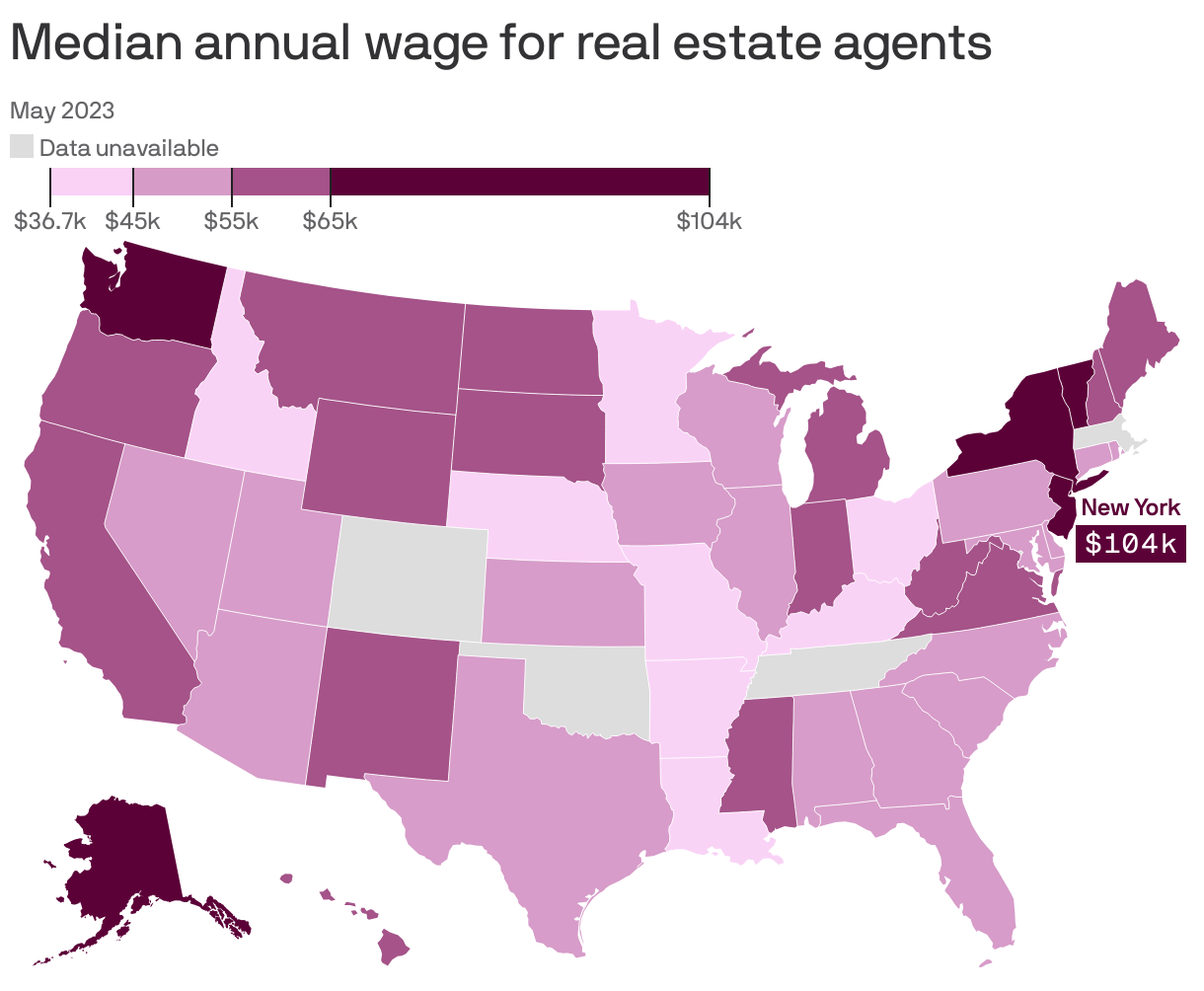

2. Charted: Broker pay around the U.S.

The future of commissions may be murky, but as Faron King, a vice president with the national association, tells Axios' Brianna Crane and Sami Sparber: Buyers' agents aren't going to work for free.

3. The stock market's concentration, in one chart

The stock market has never been as concentrated as it is now — even after the recent decline in Nvidia stock.

Why it matters: A large amount of the value of the stock market is concentrated in a handful of companies — which is to say, the performance of the stock market as a whole is increasingly a function of how just a few megacap tech stocks are faring.

How it works: One generally accepted way of measuring concentration is to look at the Herfindahl-Hirschman Index, or HHI, more familiar from its use in antitrust enforcement.

- HHI takes a sum-of-the-squares approach: It squares the market share of each S&P 500 component, and then adds all those numbers together.

- If every S&P 500 component was exactly 1/500 (0.2%) of the index, then the sum of the squares — the HHI — would come to 20, the lowest possible score.

- Conversely, if 5 stocks each comprised 10% of the index, accounting for half the total capitalization, while the other 495 were 0.1% each, then the HHI would be 505.

By the numbers: The old high point, set in March 2000 at the height of the Wintel duopoly, was 123. That record was shattered in June 2020, as a handful of high-fliers started to dominate the stock market.

- By August 2020, the S&P 500's HHI reached what was then an all-time high of 159. More recently, with the AI boom, it's risen even higher. By the end of May 2024, it reached 184.

Of note: The most recent spike, in May, is in part an Nvidia story — because the AI chipmaker's valuation rose so fast.

- Still, at the end of May, Nvidia's market capitalization was $2.7 trillion, well below the $3.1 trillion at which it closed yesterday. As a result, even after the recent sharp decline in Nvidia shares, the S&P 500 HHI could still set yet another new high this month.

The bottom line: What's far from clear is whether this spike in concentration is bullish or bearish. Concentration will probably retreat from its current highs at some point — but while bears fear devastation in megacaps, bulls look forward to seeing more strength in the rest of the market.

4. 1 fun thing: We're still calling it Twitter

Axios Markets