Axios Markets

March 10, 2023

1 big thing: Behind the crash of Silicon Valley Bank

Illustration: Annelise Capossela/Axios

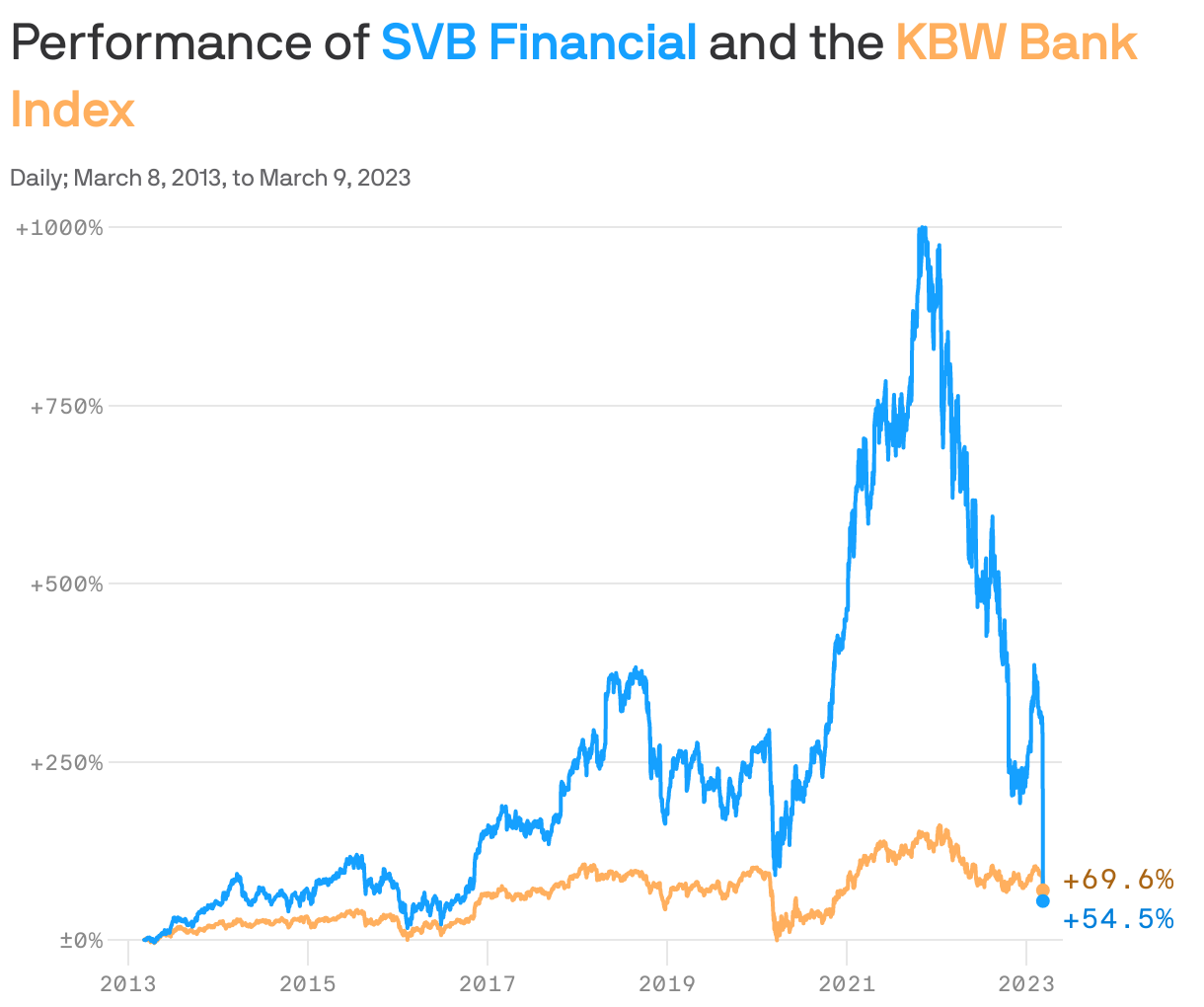

2. Charted: When it was good, it was really good

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.net2. Catch up quick

3. The U.S. default trade returns

The U.S. has hit its debt limit, which means — given congressional dysfunction — that the chances of a sovereign debt default are real, if small. One consequence has been a spike in the price of credit default swaps (CDS) that pay out if the U.S. defaults, Axios' Felix Salmon writes.

Why it matters: The price action in U.S. sovereign CDS is important, but it can't be used in the same way that other CDS prices can, to infer a probability of default.

How it works: Think of CDS as insurance against a bond defaulting. The seller of a CDS contract is effectively taking on the risk that a certain borrower — like the U.S. government — might default. Buyers of CDS are seeking to hedge that risk.

By the numbers: U.S. CDS hit an all-time high of 83 basis points on Wednesday — meaning it costs $83 to insure $10,000 of Treasury bonds against the risk of default.

- That's higher than the previous record high of 82 basis points set on July 28, 2011, during that debt-ceiling crisis.

Between the lines: If the U.S. Treasury finds itself unable to pay all its bills as they come due, all manner of horrible things would probably happen, both in markets and in the economy as a whole.

- Traders are trying to hedge that risk — that’s what the rise in the price of U.S. CDS indicates.

- If questions surrounding the full faith and credit of the United States cause markets to plunge, the price of U.S. CDS is almost certain to rise dramatically.

- Buying cheap CDS that soar in value when a crisis hits is a well-worn playbook: Hedge fund manager Bill Ackman famously made billions doing exactly that in March 2020.

Be smart: The bet here is not, really, that a U.S. default will cause the CDS to be triggered and that there is a potentially large profit to be made when that happens.

- People selling the CDS are making the reasonable bet that, ultimately, the recovery value of Treasury securities will be very close to 100 cents on the dollar — even if there is an event of default. Until then, they pocket the income the buyers pay them.

The bottom line: U.S. Treasury securities are considered risk-free assets in the financial world. The U.S. can always print the money it needs to repay its debts.

- If for some short period it fails to do so, however, the resulting tremors could be large, and the price of insurance against that earthquake would spike.

5. 💭 Quoted: Literally speaking

Axios Markets

Stay on top of the latest market trends and economic insights