Axios Markets

October 26, 2023

🎰 1 big thing: Wall Street's giant Treasury trade is back

Illustration: Shoshana Gordon/Axios

2. What is the basis trade?

Illustration: Aïda Amer/Axios

3. Flashback: March 2020

Traders work on the floor of the New York Stock Exchange on March 18, 2020. Photo by Spencer Platt/Getty Images

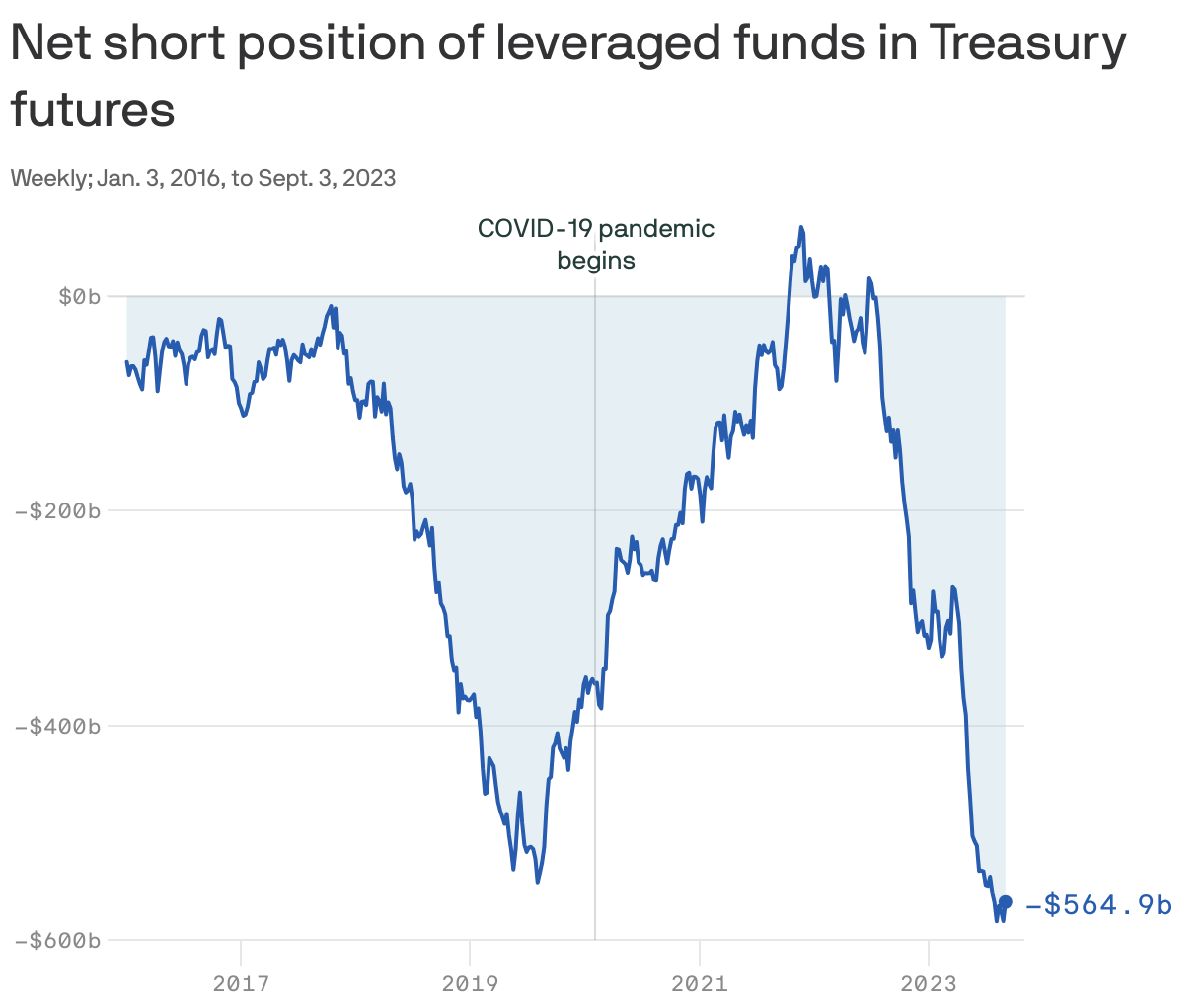

Bonus chart: It's back

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netThere's no central repository of hedge fund trades, but there are several indications that the basis trade is popular once again.

- One is the surge in short positions in the Treasury futures market by hedge funds — that's the line on the chart above that went sharply negative starting last year. (Hedge funds fall under the category of "leveraged funds" in the data collected by the government.)

- Translation: This is the leg of the trade in which the hedge fund promises to deliver the Treasury at some point in the future.

4. 💭 Matt's thought bubble: The regulators' dilemma

5. Catch up quick

Axios Markets

Stay on top of the latest market trends and economic insights