Axios Markets

September 30, 2022

1 big thing: Ugly, ugly, ugly

Illustration: Sarah Grillo/Axios

2. Catch up quick

3. Charted: IPOs down

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netOne word: Wow.

When stocks are down 24%, it may not be the best time to go public — and IPOs have all but disappeared this year, Axios’ Kate Marino writes.

Worth noting: Not included in the above chart are companies that went public by merging with SPACs.

- Those are down a ton this year, too: Q3 deal value of $13 billion is but a fraction of the $118 billion in SPAC mergers, on average, over the first three quarters of 2021, according to Dealogic.

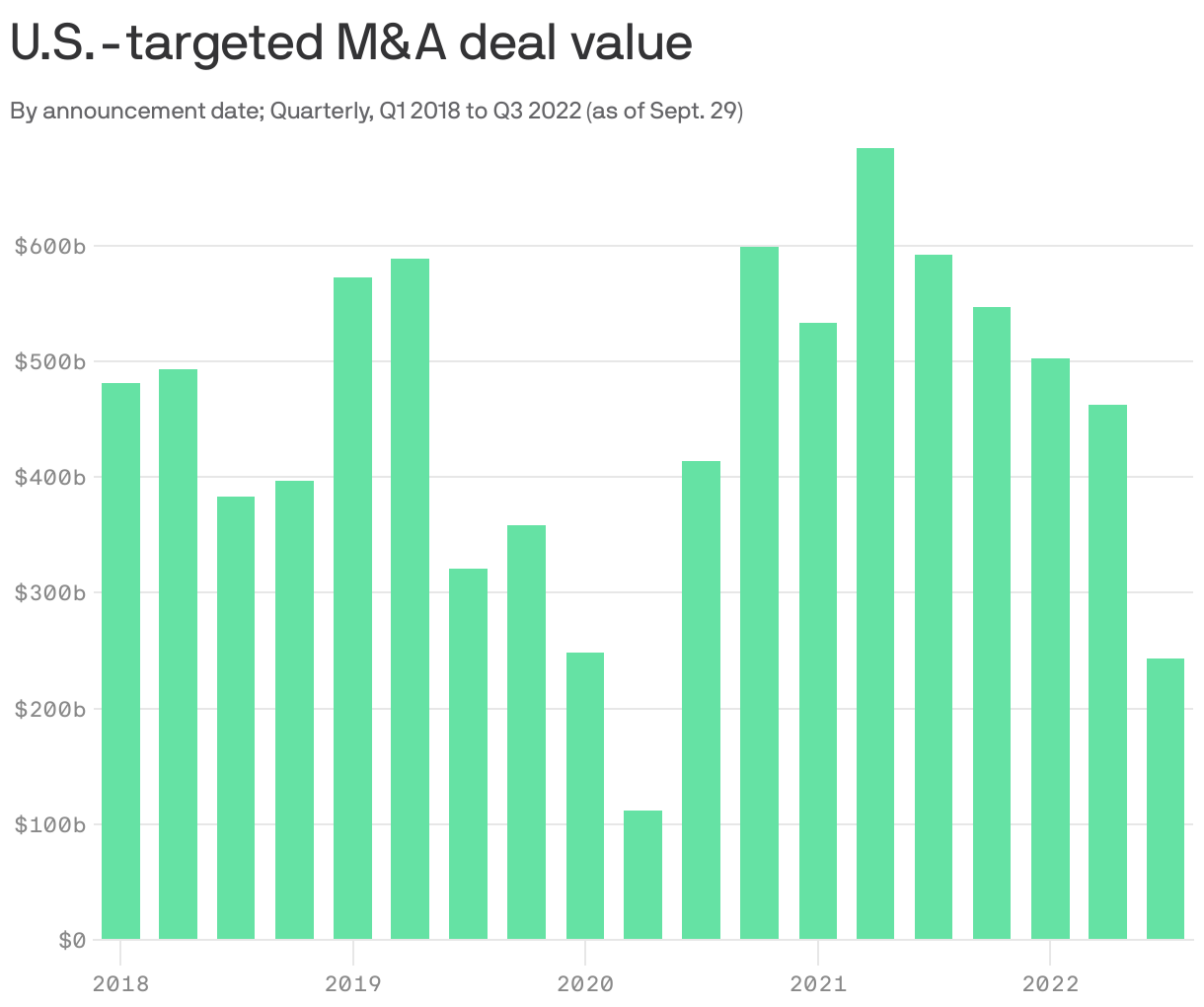

4. Charted: M&A down

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netAs of the second quarter of this year, M&A was down but not out. That changed in Q3, Kate writes.

The big picture: First-half deal volumes were lower than the record-breaking 2021 levels — but still higher than the average in the years before the pandemic.

- But in the last three months, deal-making volumes were basically halved from Q2 levels, sinking below the 2018-2019 quarterly average.

State of play: The higher cost of capital, of course, is one of the big factors. Debt’s been getting more expensive since the beginning of the year, chipping away at the affordability of financing a huge purchase.

- Recession risk is lurking, too. “When companies are anticipating that there's a recession on the horizon, they say to themselves, perhaps it's time to pull our horns in a little bit. And I think that's what we're seeing,” Ken Monaghan, co-head of high yield at Amundi U.S., tells Axios.

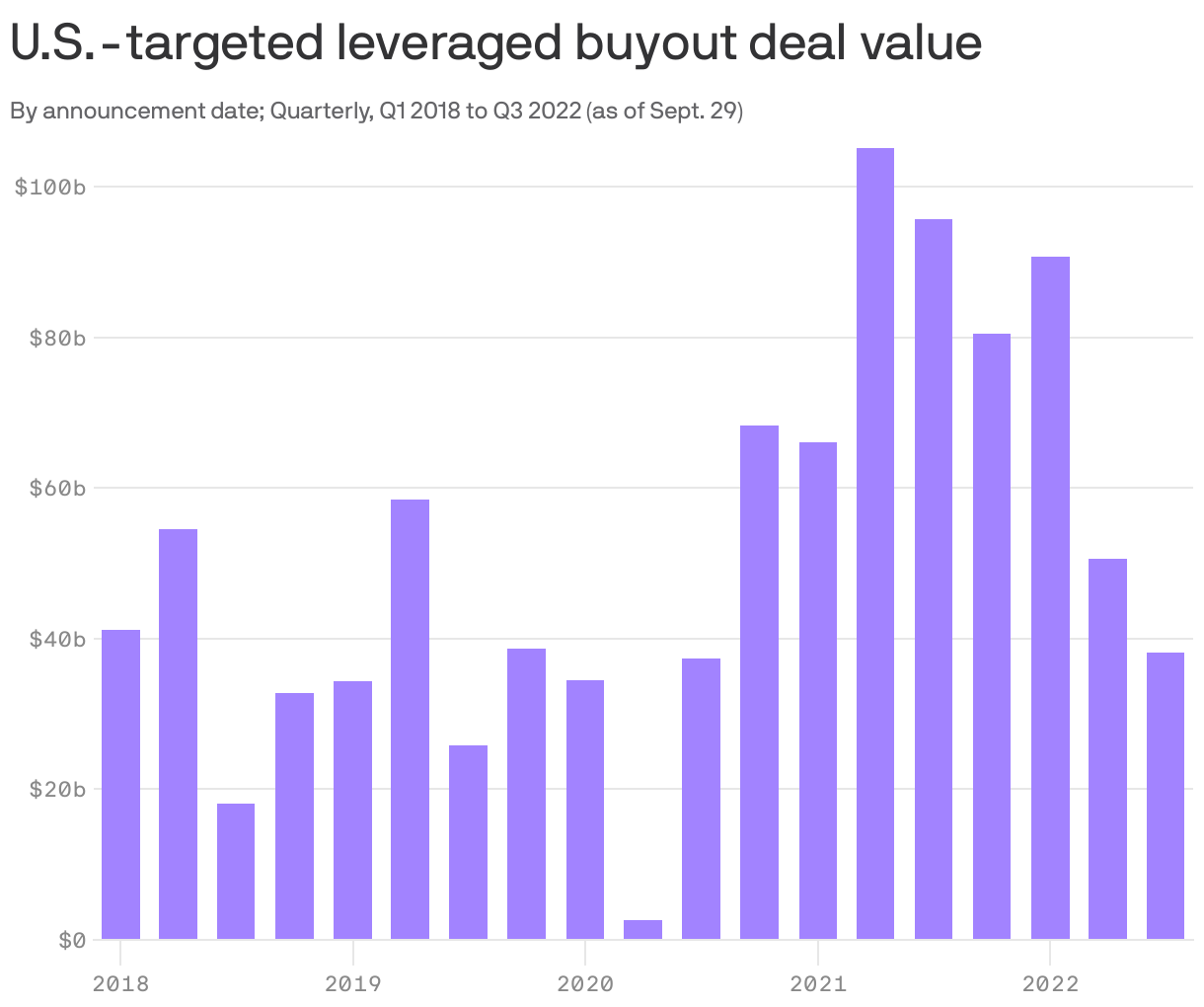

5. Charted: Leveraged buyouts down

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netThe story with leveraged buyouts (LBOs) is a little different. Though deal volumes plummeted this quarter, historically speaking they’ve held up better than corporate M&A — Q3 was neck-and-neck with the pre-pandemic average, Kate writes.

How it works: LBOs are the heavily debt-financed acquisitions by private equity firms.

- Those firms raise money from investors, and in turn, use those funds to buy companies.

The big picture: Right now, PE firms are sitting on record amounts of “dry powder,” or investor money that needs to be deployed.

- That adds up to a little more pressure to do deals than what, say, a corporate CFO might face in an uncertain market.

The bottom line: Still, Q3 LBO activity is a whopping 64% lower than the peak in the second quarter of last year — a signal of the sea change in the markets that Matt described above.

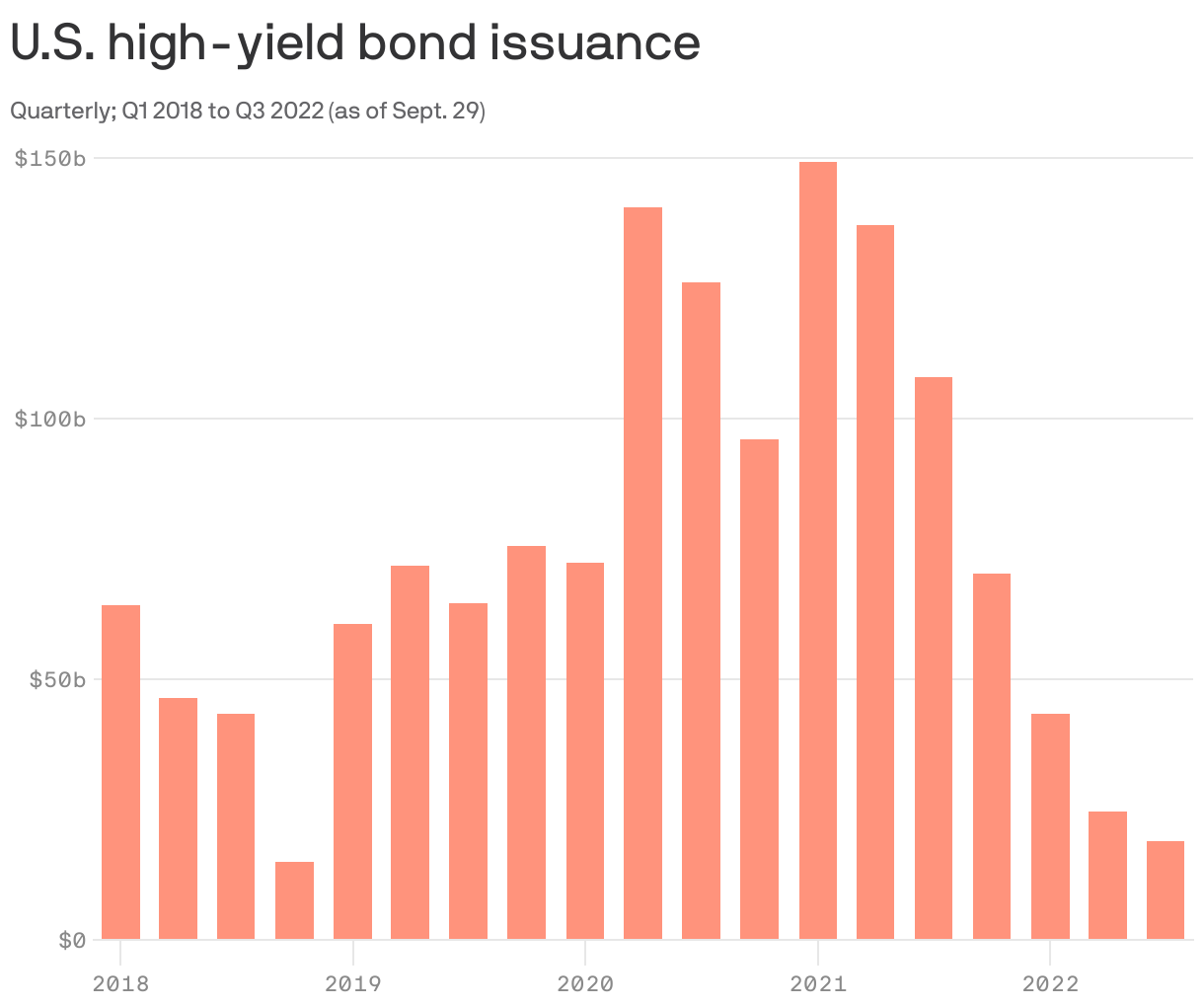

6. Charted: High yield bonds down

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netCorporate borrowing in the high yield bond market slowed to a trickle as money got more expensive, Kate writes.

- Not surprising, right? That’s basically what the Fed wanted to happen when it started raising rates.

But, but, but: The Fed’s actions before this year’s rate hikes are just as important a factor here.

- Call it the pull-forward effect: Thanks to the ultra-low rates of 2020-2021, just about every company with debt has recently refinanced — and pushed maturities to later in the decade.

- "The need to just do the normal refinancing that companies typically do, is just not there right now," says Lindsay Rosner, principal on the multi-sector portfolio management team for PGIM Fixed Income.

Meanwhile: The investment grade (IG) bond market slowed, too, though not as much as high yield.

- IG bond deals in Q3 totaled $270 billion, down from a Q1 2021 peak of $422 billion — but right on top of the 2018-2019 average of $267 billion per quarter, according to Pitchbook LCD.

What to watch: Even the higher-credit quality IG space may slow further in the months ahead.

- Rosner notes that September issuance of around $80 billion was nowhere near the $125 billion-$150 billion expected in the pipeline at the beginning of the month.

- Translation: Some of the expected deals just didn't come to market.

The bottom line: "The volatility in the market and the uncertainty around economic projections is really filtering into the credit market," Rosner says.

Axios Markets

Stay on top of the latest market trends and economic insights