Axios Markets

October 24, 2023

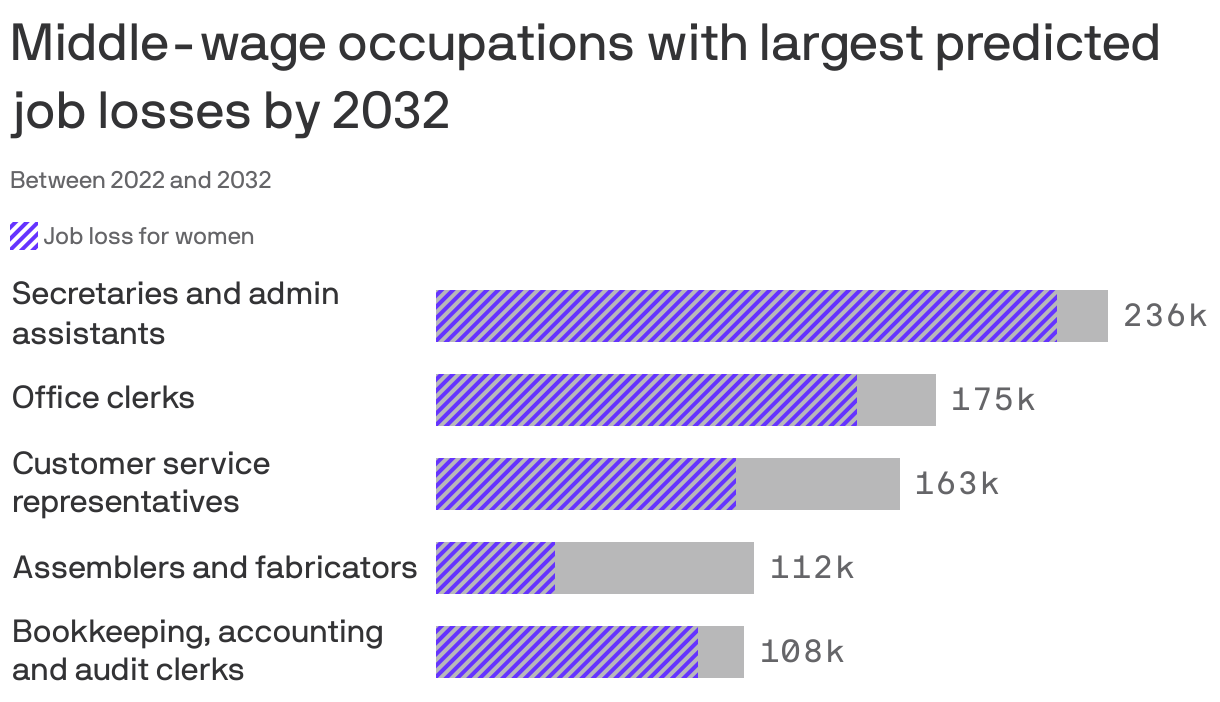

1 big thing: Tech-driven job losses will hit women hardest

Technology will eliminate scores of jobs over the next decade — and two-thirds of those losses will hit jobs currently held by women without college degrees, finds a new report shared first with Axios, Emily writes.

Why it matters: The analysis from left-of-center think tank Third Way paints what it calls a "bleak" future for women without college degrees, i.e., the majority of women in the U.S.

- Just 39% of women age 25 and up have a bachelor's degree, per the Census.

- "Opportunity is really shrinking for women without a degree," said Curran McSwigan, a senior economic policy adviser at Third Way who conducted the analysis.

By the numbers: The Bureau of Labor Statistics projects which industries are set to shed the most jobs over the next decade — 97% of those jobs are roles that don't require a bachelor's degree.

- Two-thirds of those jobs are held by women, according to Third Way's analysis, which overlaid the BLS projections with the department's data on gender and occupation.

Zoom in: Third Way calls the jobs going away "middle-wage" occupations — roles that pay between two-thirds and three times the median wage, and allow women to "provide for themselves and their families." Think office clerks, bookkeepers, and administrative assistants.

- Meanwhile: The occupations that are likely to grow for non-college workers are low-wage positions that pay less than $37,000 a year, like home health aids.

- Those who have college degrees will capture much of the growth in high-wage work.

Zoom out: For years, a lot of the conversation about the decline in middle-class jobs had to do with men and manufacturing work. The potential women-dominated job losses are an area that's gotten less attention.

- These are just projections, however. McSwigan pointed to two policy solutions to make the future a bit brighter: Improve the quality of the lower-wage jobs that women might take, and create more paths into male-dominated sectors of the economy that are doing well.

The big picture: The U.S. economy is projected to see overall job growth in the coming decade, per the BLS. But that growth will be slower than in the previous one — because of the aging of the American workforce.

- Technology will drive much of the job growth — and job loss.

- For example, the shift to online shopping could lead to a loss of 348,000 cashier jobs, according to the BLS — more than any other occupation in the country.

- However, computer and math occupations are projected to see 15% growth in the coming decade — women currently hold 27% of the jobs in that space.

- The information security analyst occupation, where women make up only 18% of current roles, is projected to grow 32%.

2. Catch up quick

3. LBOs, minus the “L”

Leveraged buyouts, or LBOs, aren't looking so leveraged anymore, Axios' Kate Marino writes.

- This year, private equity funds are ponying up more of their own cash than ever before to fund their deals — and using less debt.

Why it matters: It shows how the high interest rate environment is reshaping the economy and the way big investors deploy capital.

How it works: When private equity funds buy companies, they finance the purchases similarly to how individuals buy homes. They make a down payment — known as the equity contribution, which comes from the cash they raise from investors — and borrow the rest from banks or other lenders.

- PE funds tend to use as much debt as possible — this preserves cash for other deals and juices the funds' returns.

State of play: Debt's gotten pretty expensive this year, so the companies being acquired by PE firms can't afford as much of it.

- Loans to companies purchased by PE firms have yielded 11% on average at issuance during Q3, a record high, according to PitchBook LCD.

The impact: PE firms have been forced to use more of their funds' own money.

- Equity contributions are collectively around 51% this year, PitchBook LCD says — the first time that metric crossed the 50% threshold since the firm began tracking the data back in 1997.

- For comparison, the average equity contribution in the 10 years through 2021 was 41%.

The flip side: Leverage, or a company's ratio of debt-to-earnings, is now at a 13-year low for syndicated loans backing PE acquisitions.

- But, but, but: Even though debt is lower, interest payments are eating up a larger share of the earnings at LBO'd companies than they have since 2007, PitchBook data shows.

💭 Kate's thought bubble: Rates will (probably) come back down someday. And when they do, watch for PE firms to pounce, and take debt-financed dividends from these companies to recoup some of their cash.

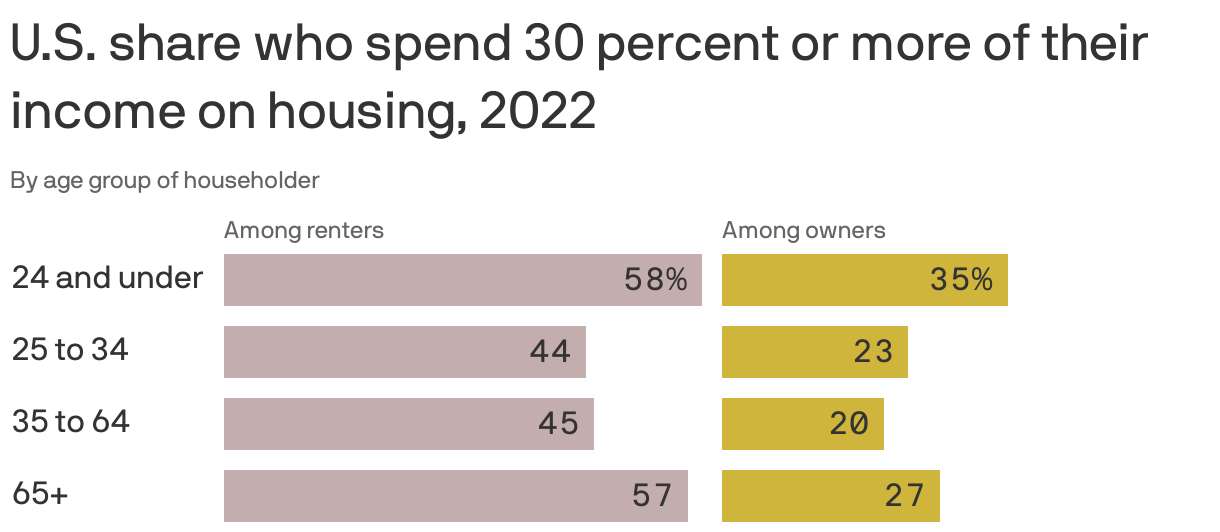

4. Charted: The weight of renting

Renters in the U.S. spent a bigger chunk of their income on housing last year than those who own their home, according to data from the Census Bureau, Emily and Axios' Sami Sparber report.

Why it matters: It's a terrible time to buy a house, but a great time to already own one.

- The price of everything has shot up over the past two years — but if you're a mortgage holder, the one thing that hasn't budged is your monthly payment.

- And about 90% of all mortgage holders are locked into rates that are well below the current near-8% interest rate on a 30-year loan.

- Meanwhile, rents have soared.

On the flip side: If you're currently debating whether to rent or buy a home — the equation is radically different. For many, renting is now the cheaper option.

- The average new mortgage payment is 52% higher than the average apartment rent, according to CBRE data cited in the WSJ.

5. 💬 Quoted: Back to the '90s

Axios Markets

Stay on top of the latest market trends and economic insights