Axios Markets

March 04, 2026

1 big thing: No "oil shock" this time

The U.S. economy tripled in size over the past half century, however, oil consumption barely grew.

Why it matters: We're far less dependent on oil than in 1979, when a crisis in Iran caused widespread disruption in the U.S.

Flashback: There were long lines for gas, and the situation was so dire that it pushed Americans to drive smaller Japanese cars, at least for a time.

Between the lines: There was lots of hand-wringing over U.S. dependence on foreign oil back then, which surely President Trump remembers. He has now taken steps to topple leadership in two oil-producing countries.

- Although gas and oil prices are rising, it's possible that over the long term the administration's attacks on Iran and Venezuela could "neutralize two oil exporters who have regularly been the cause of supply disruptions in recent generations," Greg Ip writes in the Wall Street Journal.

Where it stands: Yet the U.S. is no longer as dependent on foreign oil. Today the U.S. is the largest producer of oil in the world. And Iran's share of world oil production has decreased.

- The situation has arguably given Trump an opportunity to take on Iran.

State of play: The price of oil has increased in recent days, rattling markets and threatening to spike prices at the pump, putting pressure on Trump.

- The White House said yesterday it would step in as an insurer of last resort, and offer military escorts to oil tankers, to get shipments moving across the Middle East, sending oil prices down. But now, Brent Crude is back over $80.

The big picture: Perhaps more crucially, the economy needs less oil now.

- The "oil intensity" of the economy — looking at the ratio of oil consumption to economic growth — has declined more than 70% since 1979, as economist Paul Krugman noted this week.

Zoom in: Gas mileage on cars is much more efficient today, cheap natural gas has replaced oil in areas like home heating, and renewable energy is "starting to make a dent," Krugman explained.

- You can see the U.S. advantage by looking at the trend in natural gas prices around the world. (More on that below.)

Reality check: If the White House effort to keep the Strait of Hormuz running fails, and oil shipments don't move, prices could spike further.

- The worst case is storage tanks could start filling to capacity, as countries are unable to move fuel, which could lead to a shutdown in oil production.

- "That's the risk," Rebecca Patterson, a senior fellow at the Council on Foreign Relations, tells Axios.

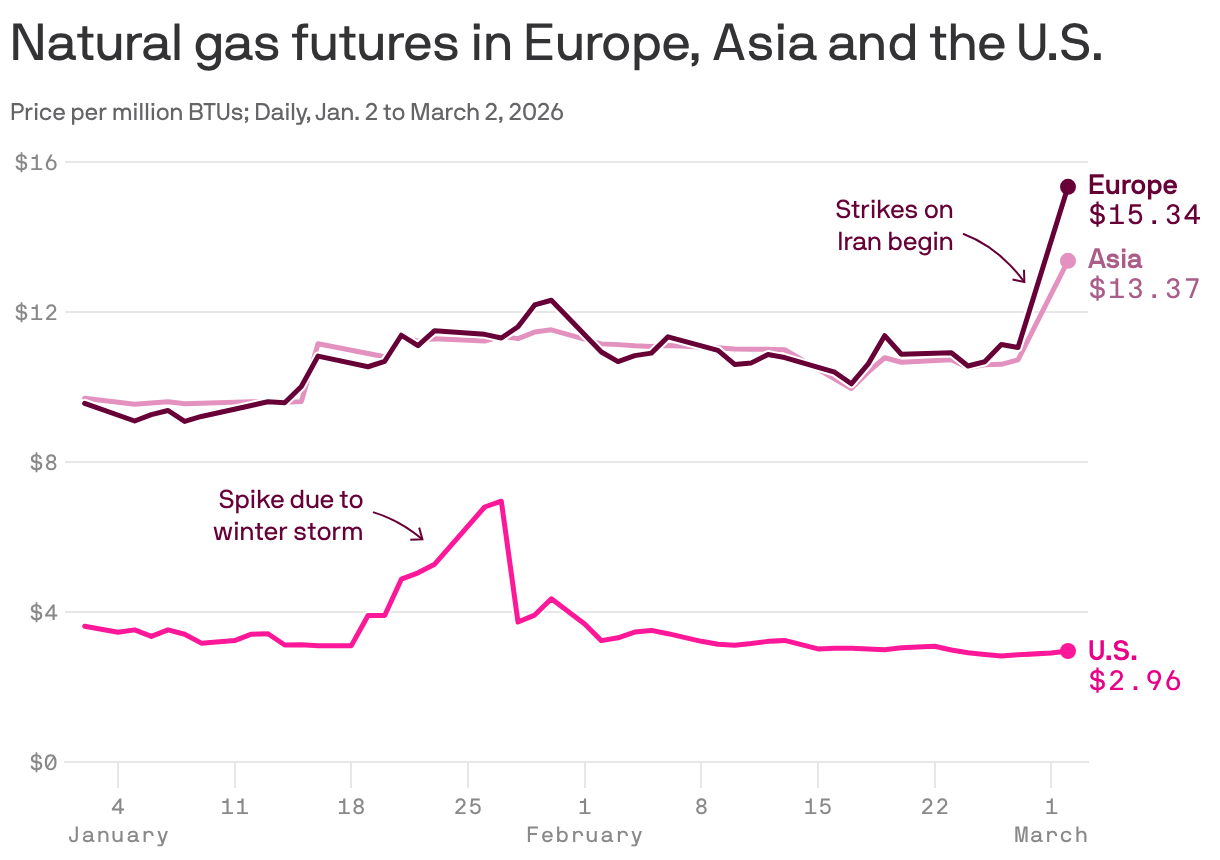

2. U.S. natural gas prices hold steady

America's natural gas bounty is acting like a moat, largely shielding the U.S. from price spikes while much of the world reels from escalating unrest in the Middle East.

Why it matters: Natural gas hasn't historically drawn the same headlines as the more volatile oil markets. But it has become increasingly central to the economy, including powering the AI boom.

State of play: The moat isn't impenetrable. If substantially more American natural gas gets exported, it could raise heating and electricity bills.

The big picture: Fueled by fracking, the U.S. has been the largest natural gas producer in the world since 2011. Since 2023, it's been the largest exporter of liquefied natural gas, the main form in which gas is shipped globally.

- That dominance provides a cushion when overseas supply is disrupted.

Driving the news: Qatar, the second-largest exporter of liquefied natural gas, said earlier this week that it is halting production amid the escalating conflict between the U.S. and Iran.

- That pulled some 20% of global liquefied natural gas exports off the market.

The result: Natural gas prices quickly spiked in Europe and Asia, but the impact in the U.S. has been much more muted, so far, anyway.

How it works: Oil is a global commodity, and prices tend to move in sync. American consumers will likely see at least a short-term spike in gasoline prices. But natural gas is still mostly regional.

Reality check: Domestic natural gas prices are forecast to increase this year due to growing liquefied natural gas exports, the U.S. Energy Information Administration said in a January report before the Middle East escalation.

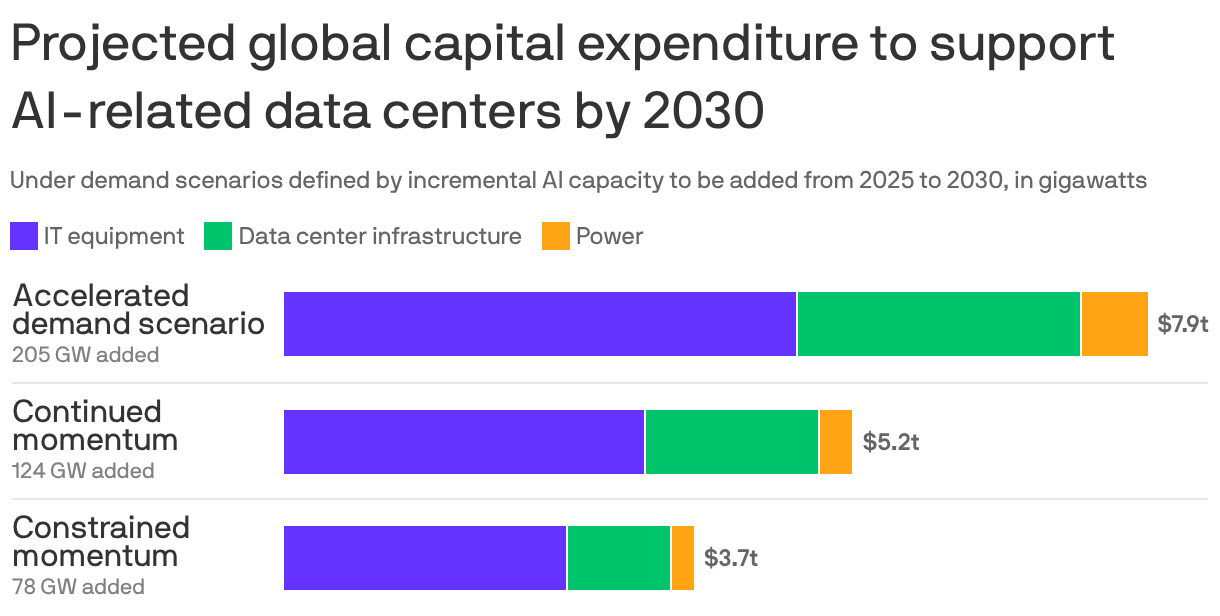

3. 💰 When any price is right

Even with rising costs, power is a small slice of what Big Tech spends on data centers.

Why it matters: Deep-pocketed tech companies are voluntarily offering up pledges to pay for their own power. To them, it's just not that much money.

By the numbers: Power costs account for 7.6% of the overall capital expenditures on data centers, according to McKinsey.

Reality check: Those numbers are from a report published last April, and this is a fast-moving story.

Driving the news: Big Tech is under pressure to pay for their power usage as electricity rates rise across the nation, with many communities blaming data centers.

What to watch: Goldman Sachs estimated last year that power demand from data centers could rise 50% from 2023 by next year and by as much as 165% by the end of the decade.

- Ongoing power constraints could push power prices up so high that they start to bite into a larger share of costs.

Axios Markets