Axios Markets

August 03, 2026

1 big thing: SpaceX is testing market gravity

Elon Musk's galactic AI rocket-social media company faces two big tests this week: reporting its first financials as a public company and potentially coping with a flood of unlocked stock.

Why it matters: Investors aren't exactly eager to scoop up shares. Judging by the SpaceX stock price, Musk's power to drive investor excitement is already fading.

- The company's stock market debut is increasingly looking like a cautionary tale for the two other mega-cap IPOs coming down the pipeline, Anthropic and OpenAI.

By the numbers: Since SpaceX's IPO on June 12 at $135 a share, its shares have fallen nearly 20% — closing at $108.37 on Friday.

Zoom out: A supply and demand situation is playing out here. SpaceX made a very small percentage of its stock available to investors when it went public, less than 5%. That means there was high demand for only a wee bit of stock. And even then, the pop faded.

Where it stands: Now, more supply is on tap. On Thursday, two days after the earnings report, SpaceX employees and some early investors will be able to sell 911.5 million shares — 12% of the total, and more than the 640 million currently on the market.

Follow the money: A lot of those folks need to sell, says venture capitalist Paul Kedrosky. They've pledged their stock to buy homes, "private islands, cars, whatever," he says.

- That puts downward pressure on the price.

- In anticipation of this, short sellers are piling in — betting the share price will go down, Bloomberg reported Friday

What they're saying: "When lockups expire, that does put downward pressure on stock prices," says Jay Ritter, the University of Florida economist known as "Mr. IPO."

- And the SpaceX unlock is unusually large because of the initial tiny float. "It's quite possible there will be a little bit of a further dip in the share prices."

Yes, but: Not all the unlocked shares will wind up on the market, Ritter says.

- And, perhaps counterintuitively, all those short sellers will be effectively supporting the share price when the lockups do expire later this week.

- Eventually they do have to buy back stock to cover their positions, and some of them might do so in the wake of the unlock.

The intrigue: The SpaceX IPO may well have been the moment the market began to turn on the AI trade, Kedrosky and others have said.

- Investors looking to buy SpaceX at share prices that analysts are increasingly seeing as overvalued also sold other assets — particularly those that had seen the most gains this year, like chip stocks.

- Since the IPO in June, those stocks saw sharp drops in value. (So steep in fact that they contributed to the near blow-up of hedge fund Situational Awareness.)

Between the lines: "You can expect the exact same phenomenon happening two more times," Kedrosky says, if and when Anthropic and OpenAI go public with similarly small floats.

Flashback: Remember the dot-com bubble and how it burst at the turn of the last century? Widely cited research from that era attributed some of that collapse to the expiration of lockup agreements putting more stock onto the market.

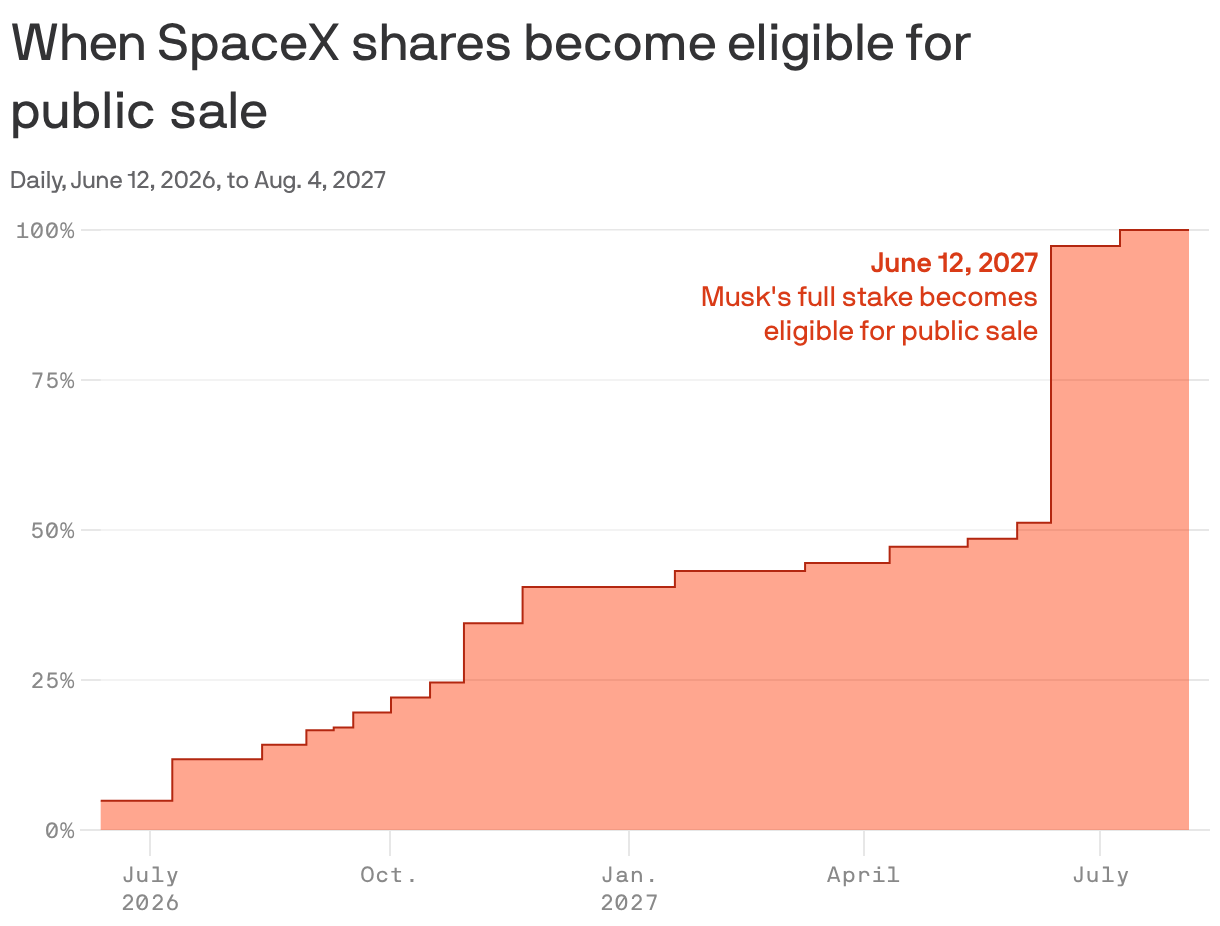

What to watch: More shares unlock through the year. By next June nearly 50% of SpaceX's shares will float on the public markets, and the rest will be in Musk's hands.

Bonus chart: More mega caps, more mega losses

SpaceX lost $773 billion in market cap from June to July — the most for any company dating back to 1970, per an Axios analysis.

Why it matters: This isn't simply about Musk. The market is in its mega-cap era, and dealing with a lot of volatility this year — that's going to make drops and gains in stock prices look big.

- Seven of the 10 biggest monthly market cap losses have happened in June and July.

The big picture: There are 13 U.S. listed public companies with a market cap of $1 trillion or more, per a tally from AlphaSense. They're mostly in the tech sector: Apple, Amazon, Nvidia, etc.

- When the numbers are that big — so are the losses and gains.

Zoom in: The eye-popping losses are a new phenomenon. Even after Axios analyzed numbers going back to 1970 and adjusted for inflation, SpaceX's gargantuan monthly loss remained on top. And only one large loss happened before 2025 — a $330 billion dip in Apple's market cap in December 2022.

Reality check: Despite its big drop, SpaceX's market cap is still above the line at $1.4 trillion.

- And Microsoft, which had two of the biggest declines in market cap this year, also notched a record one-day gain just last week.

2. Gen X is losing confidence

Generation X is not OK. The oft-forgotten cohort once identified with slacking has the lowest consumer confidence of any generation, per The Conference Board's latest numbers.

Why it matters: Xers might say nothing matters, but many in this generation are near or at their peak earning years, and if they're growing more morose it could drag down spending and the economy, to boot.

Zoom in: The business think tank's survey is meant to measure people's assessment of business conditions, jobs, incomes and outlooks — but it doesn't get into why generations differ.

Conference Board chief economist Dana Peterson — herself an Xer — offered some "probable causes."

- These include the financial and emotional pressures of being in the so-called sandwich generation, caring for both aging parents and their own children.

- Feeling unprepared for retirement.

- Plus, regrets, various.

Reality check: Gen X's elders aren't feeling so great either — confidence among boomers and the Silent Generation is only slightly better, per the data.

Between the lines: Gen X is actually being true to the generational pattern. Often cited research finds that happiness follows a U-shaped curve over a lifetime.

- Meaning: You start out happy in youth, then things begin to fall apart. Happiness bottoms out in midlife in the mid- to late-40s.

- Gen X is 45 to 61 — either in the pit of despair or just climbing out (and not the fun mosh pit kind of their youth).

Yes, but: Researchers note that more young adults are facing a crisis in wellbeing. And, slumping confidence across all generations so far hasn't put much of crimp in Americans' appetite to spend.

The bottom line: There's a reason the term midlife crisis exists.

Axios Markets

Stay on top of the latest market trends and economic insights