Axios Crypto

March 05, 2024

📈 1 big thing: Bitcoin sets new all-time high

Illustration: Shoshana Gordon/Axios

🕸️ 2. ETHDenver dispatch: Fixing internet creep

Brady at ETHDenver. Photo: Crystal Kim/Axios

🔌 3. Washington halts Bitcoin-specific power inquiry

Illustration: Gabriella Turrisi/Axios

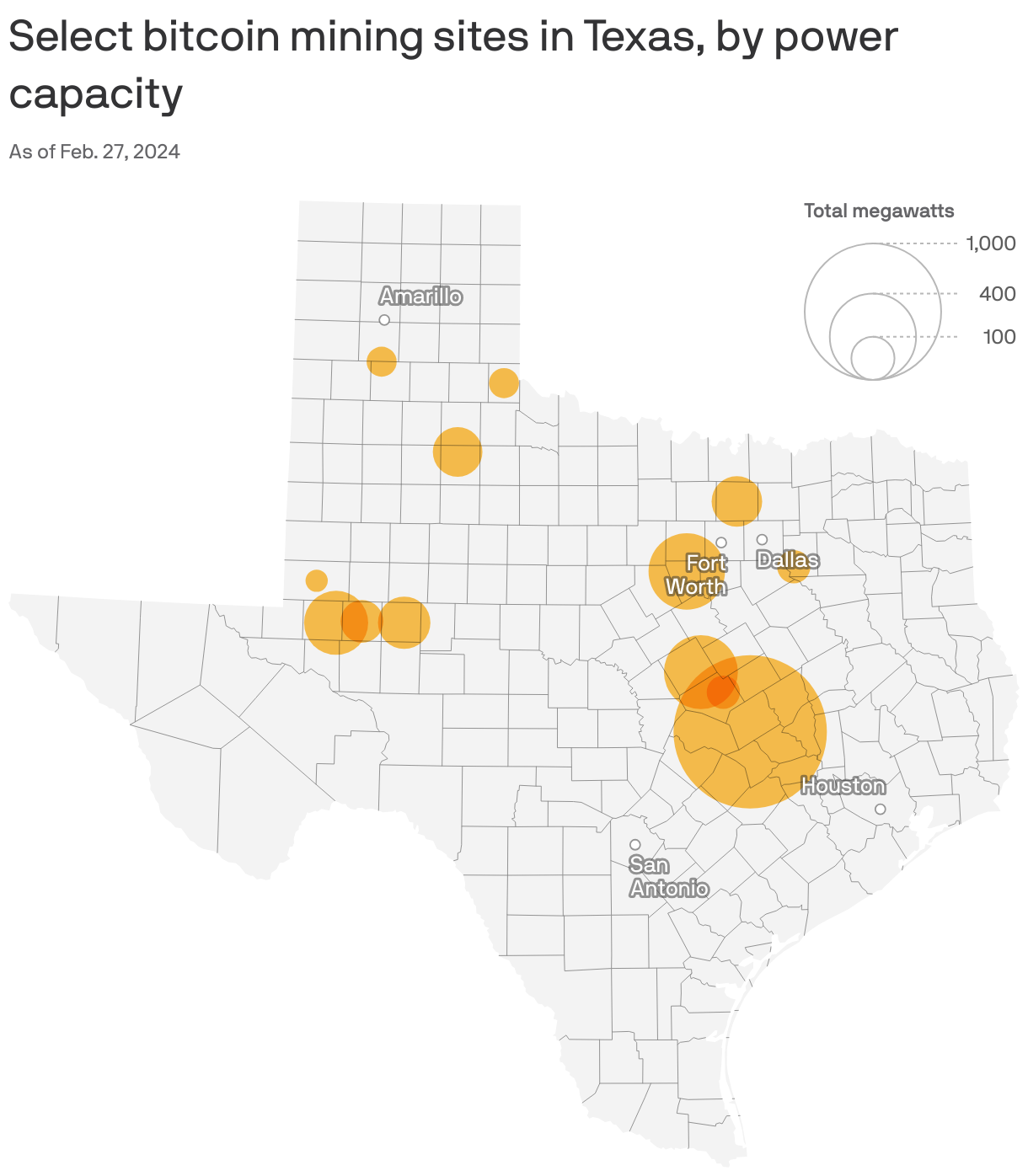

🤠 4. Charted: Power in Texas

The lion's share of conversations we have about bitcoin mining end up taking us to Texas, Brady writes.

- So we asked our friends at the bitcoin-mining publication, The Miner Mag, to peel off the Texas data set from their national map, adding details about how much power each site uses.

Why it matters: Texas is the most popular place for bitcoin mining in the nation, largely, we are told, because of the free-market approach it takes to its energy market.

- It's also a hot spot for building wind and solar capacity. Unfortunately, its grid is not up to the task of making good use of it.

What they found: As this map shows, most of the wattage is near where most people live in Texas, but there's quite a bit out in West Texas, too.

- West Texas is a more thinly populated part of the state. It is also home to lots of wind and solar power.

- The forecast for Texas is more wasted wind and solar power — that is, electricity generated that can't get to end users. (Enter: bitcoin miners.)

In the weeds: Some of the biggest operators in the state are Marathon Digital, Iris Energy, Riot Blockchain and Hut 8.

⏰ 5. Catch up quick

Illustration: Annelise Capossela/Axios

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.