Axios Crypto

April 11, 2023

GM! Bitcoin is in a good mood today, so we are going to talk about where new bitcoins come from.

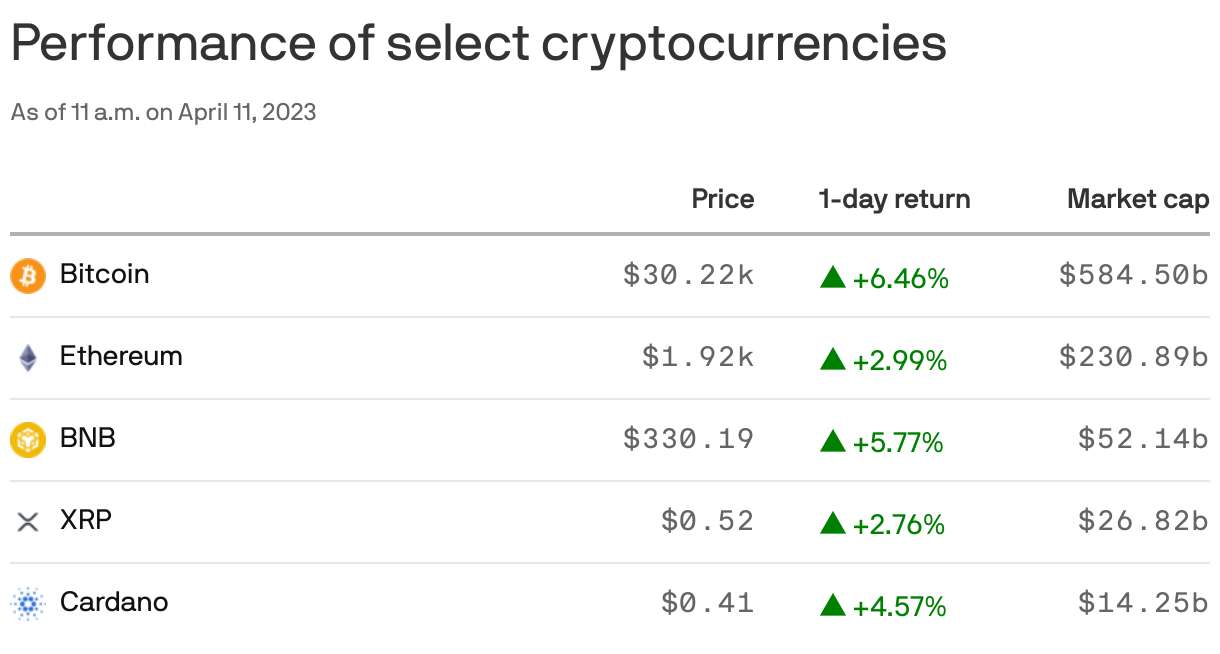

🚨 Situational awareness: Bitcoin's price broke through the psychological threshold of $30,000 for the first time since June.

📧 Is this a new level or a fluke? [email protected]

Today's newsletter is 1,461 words, a 6-minute read.

💅 1 big thing: Bitcoin mining has leveled up

Fred Thiel. Photo Illustration: Natalie Peeples/Axios. Photo: courtesy of Graham Partners

Which bitcoin miners can survive vs. which will give out comes down to this: Who planned for bitcoin price to drop or go sideways for a long time?

- That's the argument of Fred Thiel, CEO of Marathon Digital, a publicly traded company (NASDAQ: MARA) and one of the largest bitcoin mining operators, Brady writes.

Why it matters: With bitcoin price down massively from its all-time high and basically the worst year in the history of the industry in the rear-view mirror, the big question is: Where does the industry go from here?

The upshot: Thiel forecasts a lot of hardware going offline and likely a lot of mining operations giving up.

- The looming challenge is the Bitcoin halving next year (April 6?). Then, each block will be worth half as much to miners, in fresh bitcoin, than it is now.

Be smart: Most of the money miners make comes from winning the bitcoin that gets produced with new blocks.

- "There's going to be a lot of miners that — unless bitcoin is substantially closer to $48,000 — won't be able to continue to keep mining bitcoin," Thiel said. (If they have been barely holding on as it hovered around $24,000 or so, it will need to be twice as dear for them to survive post-halving.)

- Marathon has been there. It suffered losses when one of its mining partners, Compute North, went belly up last year.

The intrigue: This might surprise regular readers because we've noted that Bitcoin difficulty keeps rising.

- That's not necessarily because so many more machines are joining the network, Thiel says. It's because the latest upgraded machines are so much better.

- The difference has been massive so that the same amount of power can often generate wildly more attempts at solving the bitcoin puzzle.

What they're saying: "Right now, our belief is we're going to see likely stability in this range between 25 and 30 [thousand dollars], and it's going to take a shift in the macro environment to break through 30," Thiel said. (It's basically at 30 now.)

Marathon rarely sells bitcoin and has one of the largest piles in the world.

- In the meantime, it's investing now to move away from its approach of paying others to mine on its behalf. It's aiming to operate 50% with self-hosted supply in the near term.

- For example, it owns 20% of a 250-megawatt UAE-based bitcoin mining operation, announced in January.

- "We think there's still a lot of machines in the market at a low cost," Thiel said.

Meanwhile, diversification has been a theme for Marathon this year.

- "We've diversified our banking relationships. We now have a lot more banks on board," Thiel said, after cutting ties with the ill-fated crypto banks.

By the numbers: It now has more than five and under 10, mostly regional banks. Thiel said, "We're not mentioning the names of the banks for all sorts of reasons."

🙋♂️ 2. CleanSpark orders $145M worth of bitcoin miners

Illustration: Natalie Peeples/Axios

The Bitcoin halving is less than a year away, when each block of bitcoin mined will yield 3.125 BTC, down from the 6.25 it yields now, Brady writes.

Driving the news: And yet, CleanSpark announced today that it is spending $145 million on Antminer S19 XP units, targeting a September delivery, to be ready to win as much of the forthcoming supply as possible.

What they're saying: “The Antminer S19 XP is the most power-efficient bitcoin mining machine available in the market today, and a key component in our continuing work to build some of the most efficient bitcoin mining facilities in the country,” said Zach Bradford, CEO of CleanSpark, in a statement.

- The purchase will bring it to a 15.9 exahash, just shy of its 16 exahash goal for the end of 2023.

- In February it announced a $43.6 million deal for an additional 2.44 exahashes.

Zoom out: There are fewer than 2 million bitcoins left to mine.

Flashback: We visited two of CleanSpark's facilities in Georgia, looking at both immersion facilities and air-c0oled.

- According to CleanSpark, 90% of its energy comes from low-carbon sources.

Zoom in: A common thread between Marathon and CleanSpark: They are both buying their miners from Bitmain, the supplier that is, by far, the leader in the market.

Yes, but: Crypto is supposed to be all about decentralization and resilience.

- Thiel said there's a lot of room for these products to develop. Bitcoin mining operations are getting built as if the original cryptocurrency was still mined primarily in garages.

- "There's an architecture change that's happening," Thiel said. "We're just now starting to see the shift in the mining industry."

The bottom line: Both Marathon and CleanSpark are developing fleet-level control systems. It's just a matter of time until the machines are built to reflect that sort of operation.

🏃 3. Catch up quick

🇨🇳 Reports out of China suggest that mining equipment giant Bitmain was fined for failure to pay taxes. (Cointelegraph)

🧑🔧 Understanding the importance of this week's Shanghai upgrade on Ethereum. (Bloomberg)

🛟 The Winklevoss brothers lend Gemini, the company they founded, $100 million. (Bloomberg)

🤷 4. FTX's new leadership throws shade on founders

Illustration: Sarah Grillo/Axios

FTX debtors yesterday released a damning initial report on the crypto firm’s management practices and financial controls — or lack thereof — before its collapse, Axios Pro's Ryan Lawler writes.

Why it matters: The lack of records attendant to these failures creates a serious challenge to debtors as they seek to identify and recover assets and customer funds.

What they did: The group interviewed 19 employees who worked in policy and regulatory strategy, IT, administration, legal, compliance, and data science and engineering.

What they found: The report notes that the company lacked dedicated financial risk, audit, or treasury departments.

- FTX maintained over a thousand accounts on external digital asset trading platforms in jurisdictions around the world but “had no comprehensive, centralized source of information reflecting the purpose of these accounts, or the credentials to access them.”

- FTX and its affiliates used QuickBooks and “relied on a hodgepodge of Google documents, Slack communications, shared drives, and Excel spreadsheets” to manage their assets and liabilities.

Go deeper to see more on the firm's chaotic business practices.

What also jumped out about the new management's report, though, was FTX's cybersecurity practice, Brady writes.

TL;dr: When it comes to stewarding crypto assets, FTX was doing basically everything wrong, according to this report.

- Obviously, the new management has shown it wants to paint its predecessor in the worst light possible, but the case it makes is damning.

For example, FTX kept its private keys on cloud servers. There's no evidence that it kept any of its assets on air-gapped devices. Most of its funds were in hot wallets. It did not use any of the basic security measures to make sure no one person could pilfer its crypto assets.

- Worse, it misrepresented the quality of its security to stakeholders.

- "Despite the well-understood risks, private keys and seed phrases used by FTX.com, FTX.US, and Alameda were stored in various locations throughout the FTX Group’s computing environment in a disorganized fashion, using a variety of insecure methods and without any uniform or documented procedure," the report says.

The bottom line: It's hard to summarize all the things done wrong in this latest report other than to say: If you can think of a shortcut FTX might have taken, it probably did.

Top coins

🤝 5. Not all decentralized software rides blockchains

Illustration: Sarah Grillo/Axios

A quick note on an alternative kind of decentralization: peer-to-peer web development, Brady writes.

- Socket Supply announced today that it has a stable version of its platform, Socket Runtime, for building web development apps that primarily function in a peer-to-peer manner.

Why it matters: Socket Supply's architecture could make it much more affordable to run popular web apps that have a lot of users but not tons of revenue, by vastly minimizing the need to rely on cloud services from the likes of Amazon and Microsoft.

- It's not unusual for small and medium-sized businesses to spend more than a million dollars per year on cloud expenses.

How it works: When you scroll around in a web app (think Instagram), you're caching data that could also be used by the person next to you. Web apps that let you share public data your device has already cached take the load off centralized services.

- The more people who use that kind of network, the better it gets, Socket Supply founder Paolo Fragomeni explained to Axios.

What they're saying: "The value proposition is your cloud bill is probably the largest bill your business has," Fragomeni said.

- Socket Runtime proposes to turn users into a cloud in a way they won't even notice.

The secret sauce: "The problem with a lot of the networks as we surveyed the peer-to-peer space ... most of the networks that were designed were designed in 2002," Fragomeni said.

- Socket Runtime was built with mobile devices in mind, which could be a difference maker.

This newsletter was edited by Pete Gannon and copy edited by Carolyn DiPaolo.

From Brady: It's crazy to think that next April will be the third halving I've paid attention to.

- Do you think the halving is priced in? 😝 —C & B

Sign up for Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.