Axios Crypto

December 19, 2022

Brace yourself, frens! After Wednesday, CK and BD won't be back in your inboxes again until Jan. 4! 🥺

Today's newsletter is 1,483 words, a 5-minute read.

😤 1 big thing: Tensions mount

Illustration: Sarah Grillo/Axios

The FTX bankruptcy proceeding is starting to resemble divorce court, where the adults are angry, but no one can tell what about. And the kids are starting to cry, Crystal writes.

The big picture: The underlying tension between FTX's new chief John J. Ray III and the Bahamian government and regulators has to do with which authority— the U.S. or the Bahamas — will carry out the exchange's liquidation.

Catch up fast: The Bahamas is a sovereign nation, and regulating FTX Digital Markets — the crypto exchange registered there— was under its mandate.

- At least it was until crisis struck.

- FTX, as indicated by its new chief, wants its liquidation to be done under U.S. Chapter 11. And since starting those bankruptcy proceedings, FTX has had a strained relationship with the Securities Commission of the Bahamas.

The relationship has been tense from the start due to their overlapping roles in identifying and securing the exchange's assets, before distributing them to creditors.

The intrigue: Muddying the turf battle are allegations playing out in court around mistrust.

- Put simply, the new FTX under Ray believes that founder and former CEO Sam Bankman-Fried (SBF) was working with Bahamian regulators amid the exchange's collapse, allegedly moving money that FTX — and the bankruptcy estate — now can't account for.

Yes, but: The Securities Commission of the Bahamas, however, sees that transfer very differently.

- It says it transferred all digital assets of FTX Digital Markets (FDM) — under authority from the Bahamian Supreme Court — to a digital wallet controlled by the commission, "for safekeeping."

- "Urgent interim regulatory action was necessary to protect the interests of clients and creditors of FDM," it said.

Details: That transfer seems to have occurred on Nov. 11, the same day FTX filed for Chapter 11 bankruptcy and Ray was appointed as chief.

Zoom in: Two days earlier, on Nov. 9, securities commission director Christina Rolle alerted the commissioner of the Royal Bahamas Police Force to investigate FTX after being informed by former FTX executive Ryan Salame of potentially fraudulent activities by members of management.

- The commission a day later said it froze FTX assets, suspended its registration and applied to the Supreme Court of the Bahamas to appoint Brian Simms as a joint provisional liquidator (JPL).

State of play: The Bahamian government and its securities commission have asserted multiple times since Nov. 10 that the commision is the lead authority in investigating FTX's collapse.

Between the lines: On Dec. 7, the JPLs sent a letter to FTX's counsel saying they "urgently require immediate access" to certain FTX records, filing a motion two days later in the U.S., seeking to compel FTX to resume their access to FTX systems.

- Slack, Gmail and FTX trading systems per Amazon Web Services and Google Cloud Platform, are among the systems they are requesting resumption of access.

- FTX's counsel objected to the motion on Dec. 12, arguing that granting the Bahamas "live, dynamic access" would put that access in the hands of SBF and FTX's Gary Wang.

- Later that night, the Royal Bahamas Police Force arrested SBF.

The following day, the Bahamas securities commission admonished Ray for "misstatements" related to the November withdrawals, also accusing Ray of obstructing the commission's investigation.

The other side: Ray said in his testimony before Congress last week, "We think that the Chapter 11 process is the only open, transparent process that gives visibility to customers of what happened and when they're gonna get the money and how."

The bottom line: What strides the commission has made thus far in their coordinated effort with the JPLs to make FTX customers whole is dubious, in part, because the liquidators haven't had access to the data they said they need to do their jobs.

What we're watching: A hearing in early January where customers and the issue of privacy will come to the fore.

😓 2. Binance's stress test (not that stressful)

Much has been made recently of withdrawals from Binance, the world's largest exchange, but once you look at the numbers, it's just not that bad, Brady writes.

- Binance has a little more bitcoin than it had as FTX went bankrupt.

- Stablecoin deposits are down quite a bit, but it still has $22 billion worth.

Of note: It's interesting to see the slightly different behaviors of different kinds of users.

- The initial massive run up in bitcoin holdings might have been more retail types, perhaps exiting FTX for a safer custodian, before thinking better of that and shifting to self-custody.

- Binance, it should be noted, is by far the leader in spot bitcoin trading, according to CryptoQuant.

- The biggest holders of stablecoins are the big funds, market makers and traders. They appear to have been aggressively derisking from counterparties.

🧾 3. The unlooked books

Illustration: Sarah Grillo/Axios

There is at least one very clear reason right now for why crypto firms aren't doing audits: No one will take the job, Brady writes.

Why it matters: Following the crash of FTX, many investors and clients of crypto's big exchanges and other financial service providers would like the reassurance of knowing that these companies' numbers add up.

- Just in time: The bookkeeping biz is backing away.

Driving the news: Mazars, which had run a recent report on the world's largest exchange, Binance, pulled the report on Friday as part of a larger retreat from work in the crypto space.

- A spokesperson told the WSJ that the move was due to "concerns regarding the way these reports are understood by the public.”

- The same day, BDO, which has done the last several quarterly attestations for Tether, also said it was reevaluating whether or not it wants to serve crypto clients.

State of play: How to account for crypto assets remains an open question. The Financial Accounting Standards Board has begun a process to update the current treatment (as intangible assets, which can only lose value), but that work is incomplete.

- In a recent announcement, it warned firms that hold a significant amount of crypto assets that they will be expected to disclose them separately from other assets in that category.

In the weeds: One firm whose accounting standards have been very scrutinized is Tether. The nature of its quarterly attestations only speaks to its holdings on a single day for each quarterly report.

Yes, but: There are other ways to check. After all, all crypto assets sit in public wallets. For the key blockchains like bitcoin and ethereum, these wallets all exist on the public ledger.

- So if an exchange simply publishes which wallets belong to it, that goes a long way.

- One more level down, cryptographic technology enables them to provide proofs of their holdings, incorporating both assets and liabilities. That said, this is a new weird approach, and (understandably) not everyone is comfortable with the assurances of this novel method yet.

Of note: Binance published such proofs in late November, but some experts noted that it lacked liabilities.

- Binance claims it doesn't have any.

- Mysten Labs, which built its own blockchain, offered some critiques of Binance's approach, but they are quite technical ones.

What we're watching: The Big Four accounting firms (Deloitte, KPMG, PricewaterhouseCoopers and Ernst & Young) have done limited amounts of crypto work so far. Were they to level up the practice, smaller firms would likely be less skittish.

- None of the Big Four responded to a request for comment from Axios by press time.

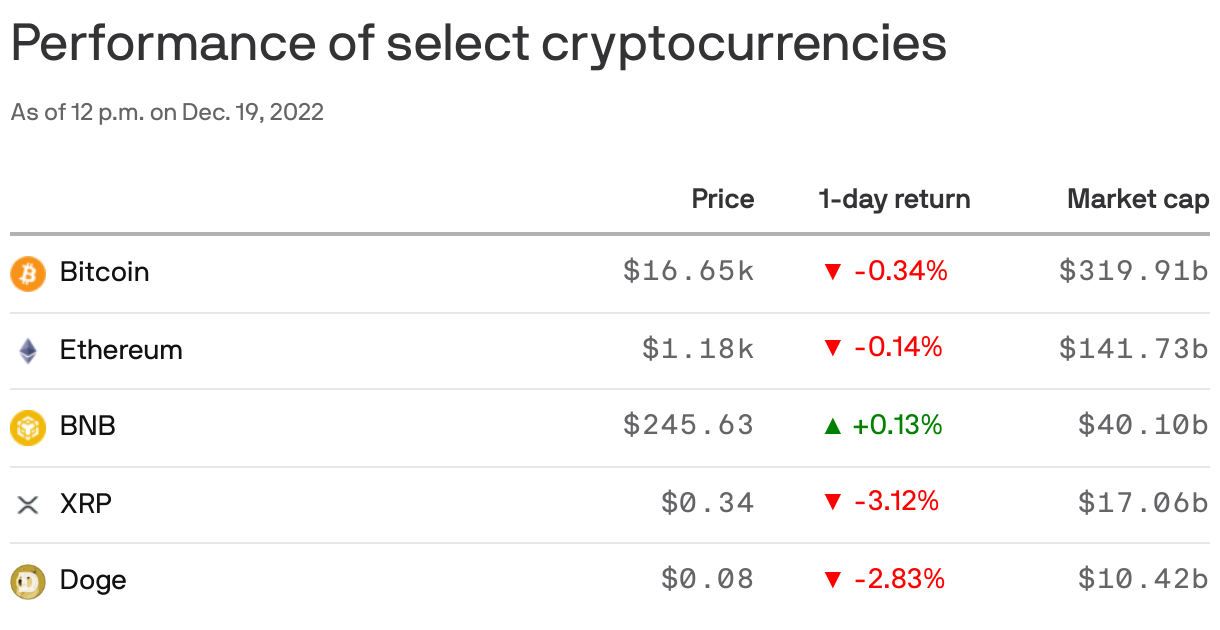

Top coins

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.net🚤 4. Catch up quick

😨 The conditions at the Fox Hill prison in the Bahamas, where Sam Bankman-Fried is being held awaiting another bail hearing, sound truly terrible, though notably he's held in the least bad part: the sick bay. (Washington Post)

🥺 Voyager, left without a buyer in the FTX bankruptcy, looks like it will be picked up by Binance.US (Axios)

👻 Grayscale, the world's largest bitcoin trust and one piece of the stumbling Digital Currency Group, is looking at options if it can't shift to an ETF. (WSJ)

🔒 $15 million in bitcoin may get locked up forever once the Ren protocol, owned now by Alameda, gets shut down for good. (The Block)

🍊 5. Culture hash: Investigating 45's NFTs

Screenshot: @Valuemancer (Twitter)

Rumors have been swirling on Twitter that the artwork for the recent Donald Trump NFT collection was repurposed from prior projects.

- The NFTs sold out in a day last week, earning about $5 million.

- Lumi, a bit of web3 gadfly, just dropped a long Twitter thread breaking down his investigation of the NFTrumps, linking it to a prior unfinished effort using the likeness of Sylvester Stallone.

Zoom out: The former president is running again.

- Just because some initiative doesn't mention a campaign specifically, doesn't mean election officials won't see it as electioneering (see the FEC guidance on coordinated communications).

- However, one of the prongs in the three-part test is payment. Who paid for the communication?

- In the case of the NFTs, the Trump organization's licensing partner paid a little, but recipients paid them even more. So it might make for a very weird case, should anyone choose to take issue with it.

This newsletter was edited by Pete Gannon and copy edited by Carolyn DiPaolo.

Tomorrow and Wednesday we've got some fun lists for you. —C & B

Sign up for Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.