Axios Crypto

November 30, 2022

📞 1 big thing: A phone call with SBF

Photo illustration: Gabriella Turrisi/Axios. Photo: Lam Yik/Bloomberg via Getty Images

👨👧👦 2. Charted: Bitcoin diverging from... bitcoin?

Much of the wealth in the crypto market is in bitcoin, Brady writes.

- But the Bitcoin blockchain has little functionality beyond accounting for bitcoin, so if someone wants to use their bitcoin to finance a trade, they often need to copy it to another chain (usually, Ethereum).

Context: Historically, these copies trade basically on par with bitcoin proper, but, in light of all the uncertainty since the FTX implosion, two of them are starting to diverge.

- The REN protocol powers renBTC. The team behind it had been acquihired by Alameda Research. They are now unwinding the original product, and renBTC are becoming more scarce by the day. (We covered this on Nov. 22, too.)

- So, renBTC are trading above bitcoin's spot price right now.

- Meanwhile, wrapped bitcoin (WBTC) is the largest derivative. It's a centralized product created by BitGo. It's trading a little below bitcoin's price now, because the market seems nervous about centralized products post-FTX.

Zoom in: But what was that giant spike last night? I wish I knew for sure.

🙏 3. BlockFi moves to return deposits now, your honor

Illustration: Megan Robinson/Axios

🚕 4. Catch up quick

🙋♂️ 5. The senator has questions (a lot of them)

Sen. Ron Wyden, Feb. 8, 2022, during a Senate Finance Committee hearing. Photo: Drew Angerer/Getty Images

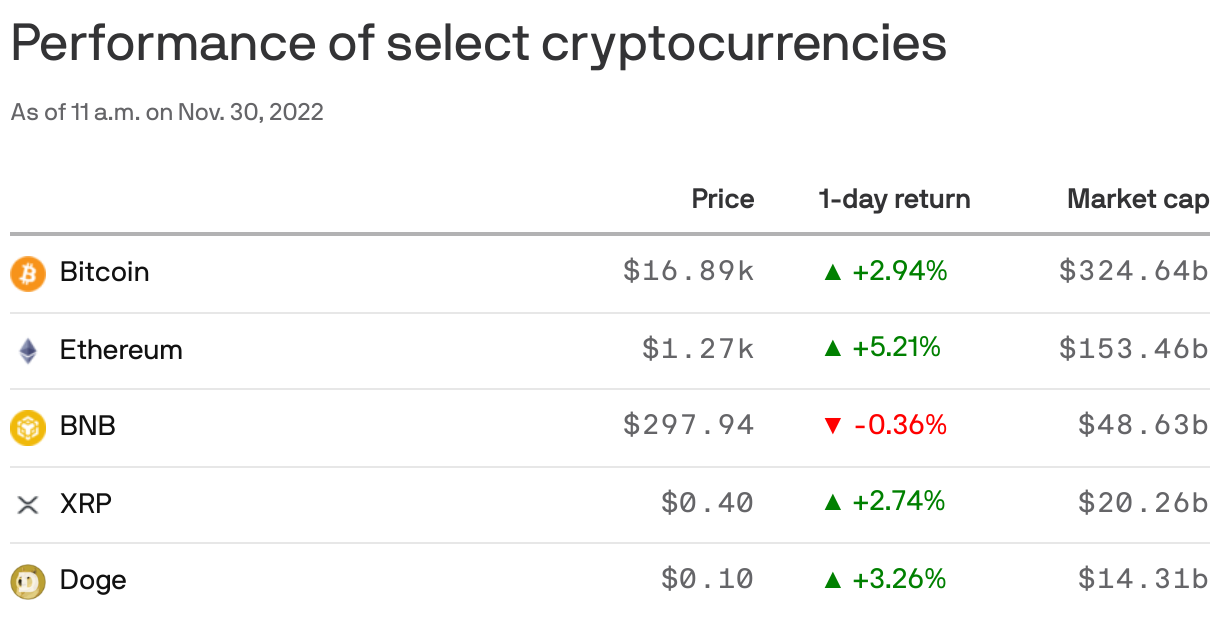

Top coins

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.