Steward Health's sale puts scrutiny on real estate deals

Add Axios as your preferred source to

see more of our stories on Google.

It's official: Six of Steward's Massachusetts hospitals will get new operators under a $343 million deal that was given the green light in bankruptcy court this week. Two other Steward-owned hospitals in the state closed last weekend, and Steward announced the sale of its doctors group last month.

Why it matters: This is the end — in Massachusetts — of a months-long ordeal that critics say laid bare the risks of private equity involvement in health care and threatened access to hospital care for patients in the state.

- The dispute illustrates the potential uncertainty of one of private equity's most criticized strategies in the health care space: sale-leasebacks, in which providers' underlying real estate is sold in exchange for cash that can be reinvested in the facility.

Yes, but: Steward runs dozens of other hospitals in other states whose operations are being transferred under a settlement reached with Medical Properties Trust, the real estate investment trust that has owned nearly all of Steward's hospitals' real estate and to which the health system has paid rent.

- MPT is looking for new operators for those facilities and will have to come to a rent agreement with them.

- That may be easier said than done if the last few weeks are any indication. Before they reached the settlement, Steward and MPT had been feuding to the point that Steward last month sued its landlord, arguing that MPT was impeding its effort to sell the hospitals.

The big picture: While it's an open question as to how much of an anomaly the Steward case has been — and whether it says anything beyond the specific mismanagement by Steward's operators — REITS own hundreds more health care facilities around the country.

- The argument for their use is that they free up much-needed cash infusions.

- The argument against seems to be exactly what was described in court: There's nothing stopping the land from being overvalued, and if the current tenants can no longer pay their rent or need to sell for some other reason, the private market won't pay the same rates.

- "Sale leasebacks are agreements that turn healthcare organizations into financial assets to be bought and sold without any regard for human care. They should be outlawed in health care," said Cornell professor Rosemary Batt.

Where it stands: Critics have long argued that Steward's former private equity owner, Cerberus — which owned the hospital chain at the time of the sale-leaseback to MPT — saddled the health system with inflated and burdensome rent responsibilities, in addition to loading it up with other debt.

- In the end, Steward argued the same thing in a court document, describing MPT's lease rates as "above-market, burdensome, and inflated."

- During the bidding process, Steward wrote in the document that it discovered "values and terms contained in the proposals, indications of interest, and bids demonstrated that the economic terms of the master leases (including the rent obligations thereunder) were significantly above-market."

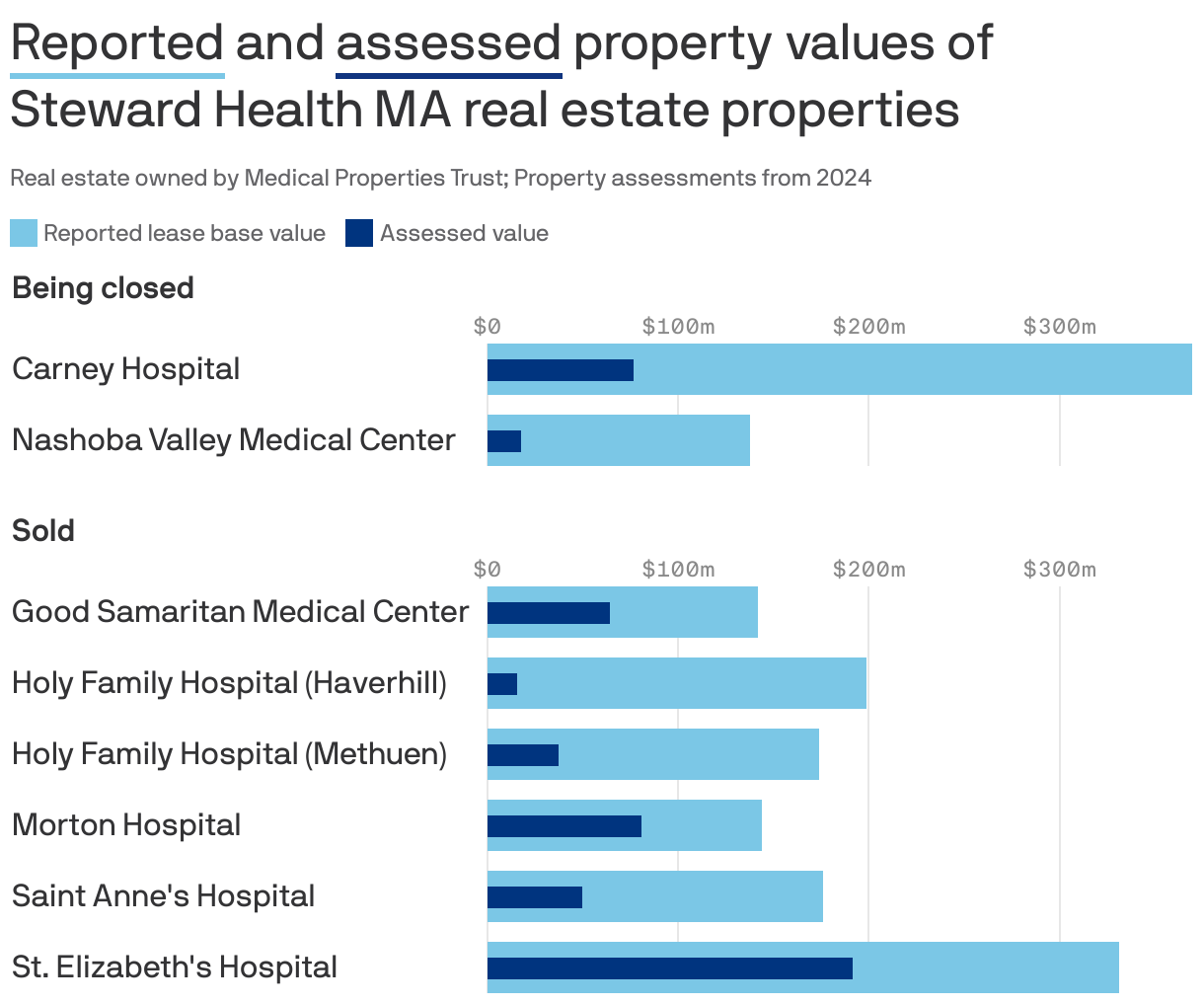

Between the lines: The value of a property is obviously in the eyes of the beholder. In this case, the Massachusetts hospitals were deemed by various entities to have wildly different values.

- First, there's what local governments say they're worth for tax purposes. It's normal for that assessed value to be lower than market rates, but in Steward's case, MPT's lease base for each hospital was often multiple times its assessed value.

- There's also what MPT bought the hospitals for back in 2016. That number, when publicly available, fell in between the assessed value and the lease base.

- And then there's what the market deemed the properties were worth, which is represented by the deal recently announced.

By the numbers: The lease base for the eight Massachusetts hospitals, according to court documents, was $1.67 billion.

- The deal for six of them — remember, two closed — was for $343 million. One of the six is being acquired by the state through eminent domain.

- The total assessed 2024 value for those six hospitals was more than $400 million, meaning in this case the market valued them even less than the government did.

- "When acquiring hospital real estate assets, MPT focuses on identifying characteristics that will appeal to experienced and competent operators. That includes physical asset quality, location, competitive market dynamics, and facility-level operations to determine true community need and, in turn, cash flow potential," an MPT spokesperson told Axios in a statement when asked about the gap between valuations.

The intrigue: MPT argued on its earnings call last month that the eight properties "can be run profitably by other operators, and the recent bidding process validated this belief," and that there had been paths to keeping all eight hospitals open.

- Insight, a Michigan-based health system, made a bid for all eight properties, but it wasn't accepted, the Boston Herald reported last month.

- "The Commonwealth's focus seems to have been on transferring ownership of these hospitals only to in-state, not-for-profit operators and, ultimately, the regulators determine who receives the license to operate these facilities," MPT president and CEO Edward Aldag said. Given this, the company decided to exit the properties.

- The insinuation: Better deals had been available, which means the one that was approved last week may not actually reflect market value.

- For what it's worth, U.S. bankruptcy court Judge Christopher Lopez called the sales approved this week, "the best deal that's on the table," Reuters reports.

On the call, Aldag also defended the use of REITs: "We are deeply concerned that the recent criticism of privately owned healthcare businesses and real estate owned by REITs stems from a misunderstanding that will only damage access to care and employment opportunities for healthcare workers over the long term."

- In a memo posted to its website, MPT argues that Steward's financial problems were unrelated to its rent obligations and that Steward said so itself in its initial bankruptcy filing.

And Steward CEO Ralph de la Torre certainly isn't avoiding controversy.

- He said this week that he won't be testifying before a Senate health committee hearing next week, even after the committee voted to subpoena him.

- In response, committee chair Sen. Bernie Sanders called de la Torre the "poster child for the type of outrageous corporate greed that is permeating through our for-profit health care system," but had plenty of blame to spread around.

- "Working with private equity vultures, he became obscenely wealthy by loading up hospitals across the country with billions in debt and selling the land underneath these hospitals to real estate executives who charge unsustainably high rent," Sanders said.

What we're watching: In its Q2 filing, MPT disclosed how much money is still at stake:

- "We have approximately $2.3 billion in real estate that is expected to be re-leased or sold as part of the ongoing bankruptcy process. We believe these investments are fully recoverable at this time."