DXYZ and the closed-end fund puzzle

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Aïda Amer/Axios

For proof that markets are inefficient, you don't need to look much further than closed-end funds, and other vehicles that behave like them.

Why it matters: When markets are frothy, you'll sometimes see investors paying dollars for dimes. Markets seem to be frothy right now — as evinced particularly in the share price of a new fund called Destiny.

The big picture: From time to time companies get listed on the stock exchange that don't do very much except buy and own various assets. The assets get put into a box, and investors can buy shares in the box, and in principle, the value of the shares should reflect the value of the assets in the box.

- The most common such box is a closed-end fund — a box that contains shares or other securities chosen by a fund manager.

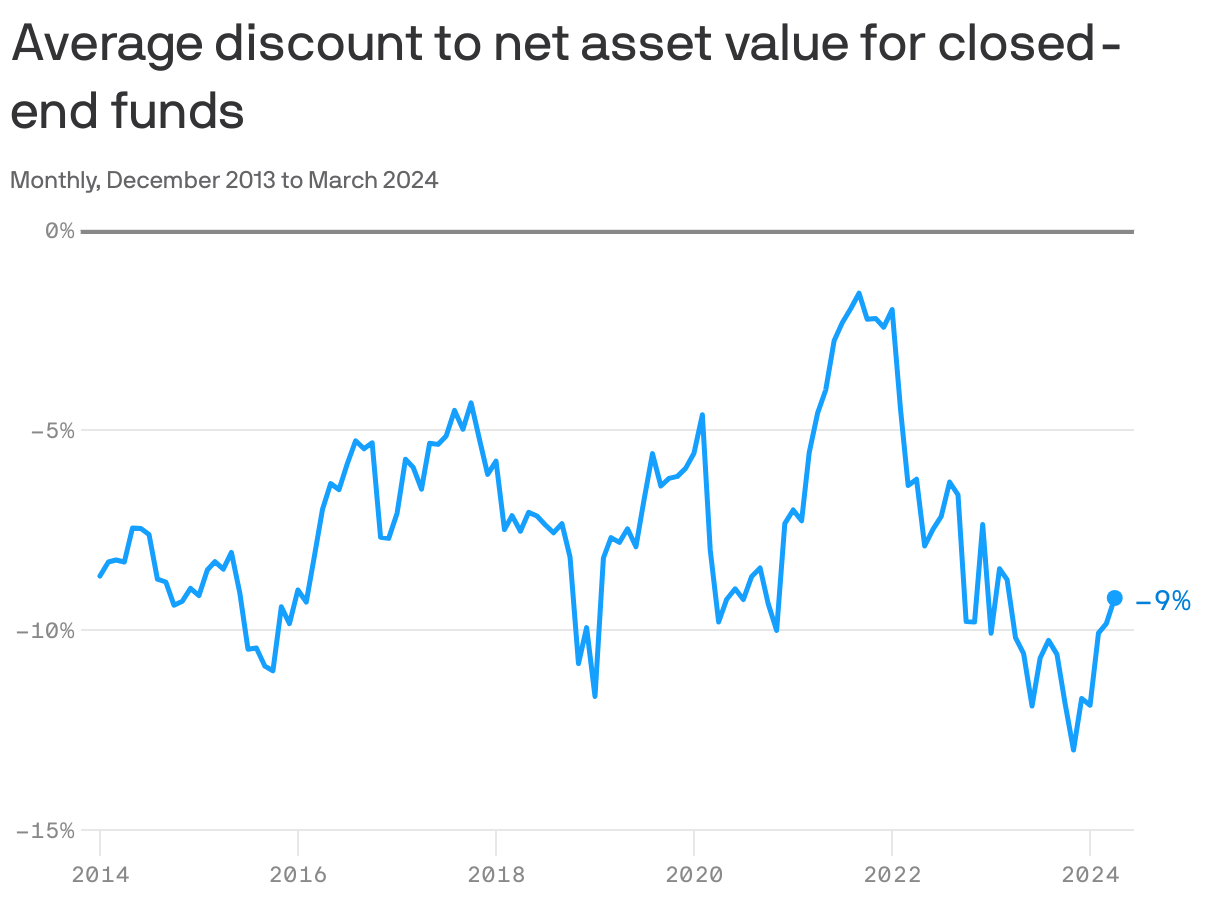

Most of the time, such funds trade at a discount to net asset value, or NAV — which is to say, the market capitalization of the box is lower than the value of the securities in the box.

- Currently, the average discount for closed-end funds is about 9%, per Morningstar Direct, with only 14% of funds trading at a premium to NAV.

- The chart shows why ETFs have effectively replaced closed-end funds as the preferred way to buy funds on the stock market.

Zoom out: It makes sense for closed-end funds to trade below net asset value: The fund managers need to get paid, and most fund managers fail to outperform the market, so the value of the box is essentially the value of the securities minus the deadweight cost of operating the box.

- Sometimes, however, when the managers are seen as having great ability, the box can trade above net asset value.

- The most famous such box is probably Berkshire Hathaway. Warren Buffett's investment vehicle isn't a closed-end fund, but, especially in its early years, it behaved a lot like one. Investors wanting to bet on Buffett's investing genius would buy Berkshire stock for a premium over the value of the shares and companies that Berkshire owned.

Driving the news: Destiny Tech 100, a closed-end fund that went public last week as DXYZ, is a box containing about $53 million in private-company shares.

- Its market cap is volatile but closed on Monday at an eye-popping $1.1 billion.

Where it stands: DXYZ might be the most extreme example, but it's far from the only box trading well above the value of what it holds.

- MicroStrategy, trading as MSTR, is at this point mainly a box holding bitcoin. As the WSJ's Jason Zweig points out, the value of the company is double the value of its bitcoin and its small software business.

- Icahn Enterprises, run by corporate raider Carl Icahn and trading as IEP, claims a net asset value of $4.8 billion — but has a market cap of $7.5 billion. That's one reason it's been in the crosshairs of short-seller Hindenburg Research.

- Many Pimco bond funds trade above NAV. The firm's Corporate and Income Opportunity Fund, for instance, listed as PTY, trades at a 32% premium.

Between the lines: Executives like Icahn or MicroStrategy's Michael Saylor love to take advantage of the premium to net asset value by issuing stock (or convertible debt) and using it to buy more assets for their box. So long as the stock trades above NAV, that deal reliably creates new wealth.

- Hedge fund manager Bill Ackman has announced plans to attempt something very similar.

The bottom line: Closed-end funds don't make a lot of sense, as their systemic discount to NAV shows. But so long as some vehicles trade at a significant premium to NAV and can effectively print money, new ones will always be created.